Can the wild swings in the price of oil over the last few weeks have anything to do with supply and demand?

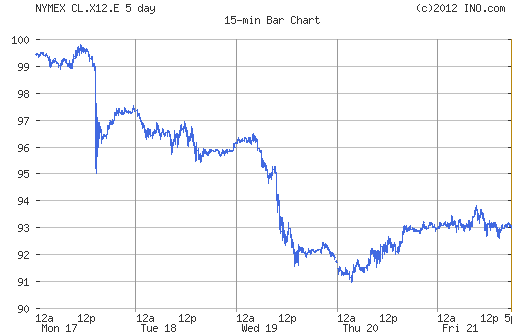

NYMEX November crude oil. Source: ino.com.

The Wall Street Journal carried this account last week:

Oil prices dropped more than $3 in less than a minute late in the trading day on Monday, just as trading volume spiked. The move also dragged down prices of gold, copper and even the euro.

“Traders were looking like deer in the headlights,” said Peter Donovan, a floor trader at Vantage Trading on the New York Mercantile Exchange. “I called four different desks, and they all said, ‘we don’t know.’ ”

The move came at about 1:54 p.m. EDT. West Texas Intermediate crude for October delivery plummeted to $94.83 a barrel on the Nymex, from more than $98. Some 12,500 contracts changed hands in a minute, compared with less than 500 a minute previously.

The move sparked talk of an erroneous trade—called a “fat-finger” error in industry parlance—or a computer algorithm gone awry.

Fat finger or no, there was an even bigger drop on Wednesday, leaving the price of West Texas Intermediate well below where it had been prior to Fed Chair Ben Bernanke’s Jackson Hole speech on August 31 and the Fed’s announcement of QE3 on September 13.

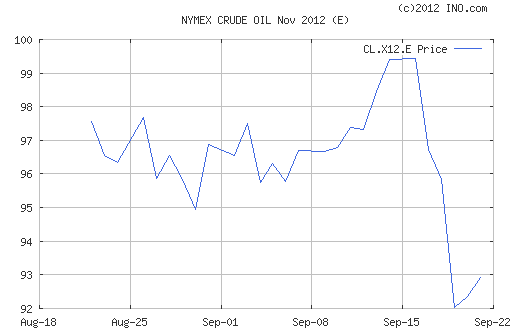

NYMEX November crude oil. Source: ino.com.

Those who doubt that oil prices are determined solely by fundamentals would naturally ask, what aspect of the supply or demand for oil could have possibly changed in the course of less than a minute last Monday? The obvious and correct answer is, there was no change in either the supply or the demand for physical oil over the course of that minute. The minute-by-minute price of a NYMEX contract is determined by how many people are wanting to buy that financial contract and at what price, not by how much gasoline motorists burned in their cars that minute. But since changes in the price of crude oil are the key determinant of the price consumers pay for gasoline, doesn’t that establish pretty clearly that the whims or fat fingers of financial traders are ultimately determining the price we all pay at the pump?

In one sense, the answer to that question is yes– last week’s decline in the price of crude oil will soon show up as a lower price Americans pay for gasoline. But here’s the problem you run into if you try to carry that theory too far. There are at the end of this chain real people who burn real gasoline when they drive real cars. And how much gasoline they burn depends in part on the price they pay– with a higher price, some people use a little bit less. Not a lot less– the price of gasoline could change quite a lot and it would take some time before you could be sure you see a response in the data. That small (and often sluggish) response is why the price of oil can and does move quite a bit on a minute-by-minute basis, seemingly driven by forces having nothing to do with the final users of the product.

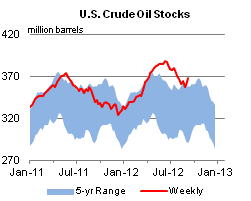

But if the price of oil that emerges from that process turns out to be one at which the quantity of the physical product that is consumed is a different amount from the physical quantity produced, something has to give. Indeed, the bigger price drops we saw on Wednesday followed news that U.S. inventories of crude were significantly higher than expected:

Oil dropped to a one-month low after U.S. crude inventories surged the most since March as production and imports rebounded from Hurricane Isaac.

Futures decreased as much as 3.3 percent after the Energy Department said supplies rose 8.53 million barrels last week, more than eight times what was projected in a Bloomberg survey. Imports arrived at the highest rate since January and output rose. Crude fell before the report on speculation Saudi Arabia is moving to reduce prices.

U.S. crude oil inventories (millions of barrels). Source: This Week in Petroleum.

There are several channels by which QE3 may end up influencing the quantity of oil physically produced and consumed. A lower value for the U.S. dollar would mean a greater quantity demanded worldwide at a given dollar price of oil. A higher level of economic activity (the ultimate goal of QE3) would also boost demand for the physical product. And lower real interest rates may make it profitable to store more oil physically, leaving less available for the ultimate users of the product. So I would have expected QE3 overall to be one factor that could contribute to a higher dollar price for oil.

But any investors who have been assuming that QE3 will boost the price of oil for no reason other than the fact that other traders expect it to raise the price of oil may find themselves tripping painfully over the fat finger of reality.

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply