The earnings season is upon us and each company’s earnings announcement is eagerly awaited, traded upon and talked about. For widely followed companies like Apple, the obsession with what the next earnings report will deliver overwhelms any sensible assessment of what it means for the company. But is this obsession merited? Do earnings announcements have significant effects on value? If so, why? More importantly, can you make money off earnings announcements?

The “Announcement” Process

To understand how and why earnings reports matter, we should start by looking at the process. Publicly traded companies are required to report on their performance at “regular” intervals. In the US, the reports have to come every quarter, with full financial statements filed with the SEC. The degree of disclosure varies across markets, both on timing (quarterly, semi-annual and annual) and on information (partial reports of performance in some regimes).

The reporting ritual is highly scripted, at least in the US, in terms of timing (companies report earnings on about the same date every year, give or take weekends, and in the same format to allow for year to year comparisons). The initial report provides the bare bone details (revenue growth, earnings per share and a breakdown of a few extraordinary items) and is followed a few weeks later by the full filing of the quarterly report (10Q) with the SEC.

Since earnings reports contain information that can affect prices, the SEC does regulate trading and disclosure around the reports. Insiders are restricted from trading before earnings announcements and Regulation FD bars firms from providing information about upcoming earnings reports to subsets of investors (analysts). In theory, at least, the information in an earnings report should be “news” to markets.

Companies may be restricted from providing information selectively to analysts following them, but this does not prevent analysts from forming and propagating their expectations about what the earnings report will contain to their clients and, by extension, the public. In fact, a substantial portion of a typical equity research analyst’s time is spent on the “earnings forecasting” exercise, and there are services that assess analyst quality by looking at how close the forecast comes to actual numbers. In the US, services such as Zacks and I/B/E/S that track and report analyst forecasts of earnings and you can find them in the public domain (Yahoo! Finance or similar sites)

The Expectation Game

When a company does report its earnings, markets will react to the “news” in the report but the way we measure the news has to be relative to expectations. Thus, a company that reports that its earnings went up by 30% may be seen as delivering bad news, if investors were expecting an increase of 40%, and a firm that announces an earnings decline of 30% may be providing positive information, if the expectation was that earnings would decline by 40%. Thus, it is not the magnitude of the earnings change that matter but the “surprise” in the earnings, measured as the earnings change relative to expectations.

But how do you measure expectations? One obvious answer is to use the analyst estimates of the earnings and news reports like this one generally compare the earnings change to the “consensus” estimate of earnings change to frame the report. A second is to use the “past” earnings growth for the company as a measure of expected earnings growth. With either measure, then, a positive (negative) earnings surprise then becomes an earnings report where the actual earnings per share exceeds (falls below) the expected value (using consensus earnings estimates or historical earnings growth).

While you can use analysts or history as the basis for estimating expected earnings, the market expectations process is a more nuanced one and more difficult to model. In the last two decades, firms have become more attuned to playing the earnings game, and have become increasingly adept at beating earnings expectations by playing both sides of the game. First, they work on analyst expectations, using selective leaks to bring expectations down, prior to earnings reports. Second, they work to mold the actual earnings, using both accounting choices (earnings management) and operating discretion (timing of R&D expenses, for instance) to deliver results that beat expectations. The problem with this game is that markets catch on and adjust expectations accordingly.

The Announcement Effect

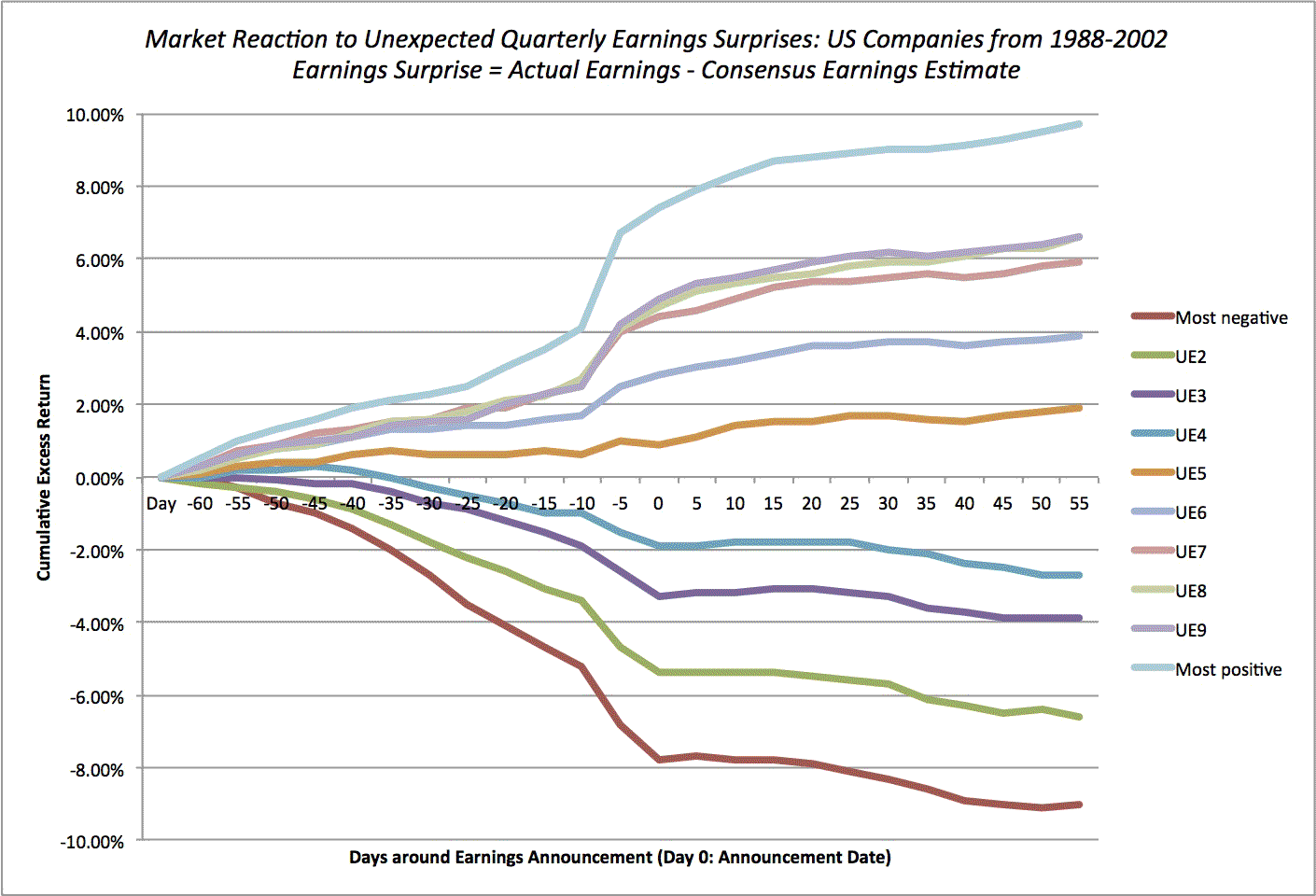

If you can measure earnings expectations, an earnings surprise should have an effect on stock prices, with positive (negative) surprises evoking positive (negative) responses. The earliest studies of earnings surprises used historical earnings to estimate expected earnings and found backing for this hypothesis. In more recent studies, consensus estimates of earnings have been used to measure expected earnings. The following graph captures the announcement effect of earnings surprises, categorized from most positive to most negative, with expectations measured as consensus estimate from analysts:

(click to enlarge)

There are three interesting findings embedded in this graph.

- Pre-announcement drift: There is a mild drift in stock prices before earnings reports that is consistent with the eventual surprise: prices move up before positive surprises and down before negative surprises. I will let you make the judgment on whether this is evidence of insider trading, investor prescience or some combination of the two.

- Announcement effect: The announcement still contains news. On the announcement, the price effect reflects the magnitude and the direction of the surprise, with stock prices going up about 3%, on average, in reaction to the most positive surprises.

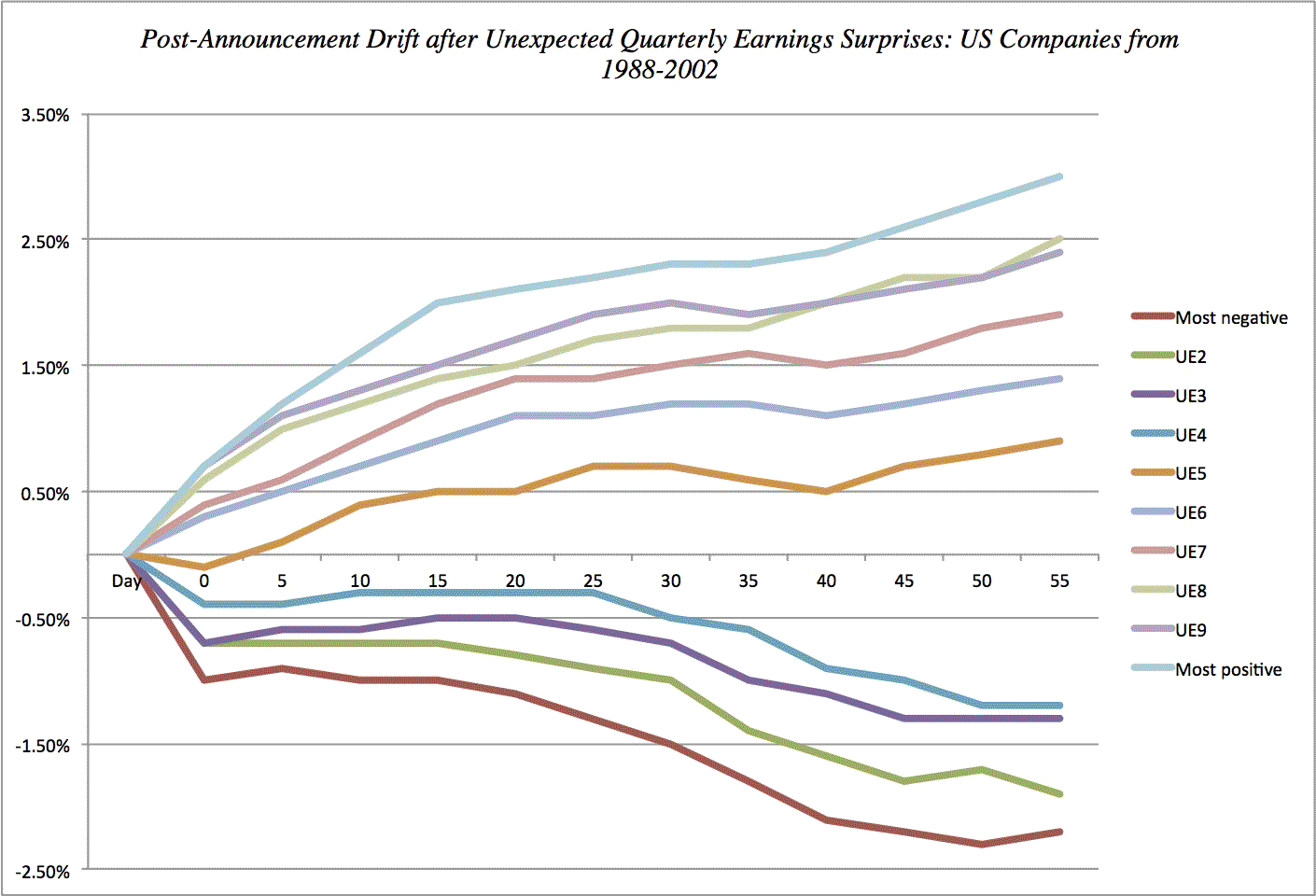

- Post-announcement drift: The most surprising finding is that stock prices continue to drift after the announcement in response to the surprise. The graph below looks at the price drift in the 30 days after the announcement:

(click to enlarge)

Differences across firms

There are studies that indicate that the returns associated with earnings surprises are more pronounced with some types of stocks than with others. For instance,

- A study of value and growth stocks found, instance, that the returns in the three days around earnings announcements were much more positive for value stocks (defined as low PE and PBV stocks) than for growth stocks across all earnings announcements – positive as well as negative. This suggests that you are much more likely to get a positive surprise with a value stock than with a growth stock, indicating perhaps that markets tend to be overly optimistic in their expectations for growth companies.

- Earnings announcements made by smaller firms seem to have a larger impact on stock prices on the announcement date and prices are more likely to drift after the announcement.

- As with analyst reports, there seems to be evidence that the market reaction to earnings reports is a function not only of the earnings number reported but also the accompanying management commentary.

- There is some evidence that the market reaction to earnings reports is greater at firms with high institutional ownership, with one rationale being offered that institutional investors tend to be more short term in their focus and thus more likely to respond to quarterly earnings reports.

There is one final aspect of the earnings game that may be affecting stock market reactions. As firms become adept at playing the game, managing expectations and tweaking earnings to beat expectations, investors have adapted. Firms that consistently beat consensus estimates now have to beat them by a “margin” (based upon their past history) to register a positive surprise. This is of course the phenomenon of “whispered earnings”. With the Apple announcement due later today (July 24, 2012), the consensus earnings estimate is for earnings per share of $10.35 and the whispered earnings estimate is 67 cents higher at $11.02. The only problem is that Apple has beaten whispered earnings 42 out of the last 56 quarters. It is only a matter of time, I guess, before you have whispers on top of whispered earnings. My head hurts just thinking about the possibilities.

Playing the Earnings Game

So, how can investors play the earnings game? Using the earnings surprise graph as the basis for the discussion, here are some of the possible paths.

a. Predict the surprise: You can try to devise ways of forecasting positive or negative surprises before they occur. I know it is easier said than done, but to the extent that you can stay on the right side of the insider trading law and find advance indicators of upcoming surprises (trading volume changes, price patterns etc.) you can profit.

b. Trade on the news: To take advantage of the drift after the news, you could buy stocks after exceptionally positive earnings announcements and sell short on stocks after terrible earnings reports. Given that the drift is about 2-3%, don’t expect this to do much more than augment returns at the margin. You could of course load up and use options to leverage the profits, but…

c. Play the earnings momentum game: While the first two strategies are short term, there is a longer term strategy that can be built around earnings reports. Studies indicate that companies that have consistently beat earnings reports over the last few quarters deliver higher returns in subsequent periods. Thus, in addition to screening for high quality growth and low risk, you can also screen for earnings momentum.

d. Intrinsic value assessment: As a believer in intrinsic valuation, I look for ways to tie the information in earnings reports to intrinsic value. To do that, though, you need to look past the top line news (earnings per share) and at the underlying details (revenue growth, operating margins and return on capital). If you do so, you may very well find a report that looks positive on the surface (because the actual earnings exceed expectations) but contains enough negative news (lower revenue growth, declining margins and return on capitals) to cause intrinsic value to decrease. If the market misreads the report as “good” news and the stock price jumps up, you have the makings for a contrarian play.

So, here is the challenge. By the time you read this post, the Apple earnings report will have been made public. Evaluate it and make your judgment on how (if at all) you will incorporate it into your investment strategy for Apple. I have attached my intrinsic valuation of Apple (made before the earnings report came out) with suggestions on how to incorporate the information in the earnings report into value. Take your best shot!

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply