I spend a lot of time writing…and talking…about the credit inflation that has taken place in the United States over the past fifty years. In my mind, this period of credit inflation set the stage for the Great Recession of December 2007 through July 2009. It also set the stage for the debt overhang that burdens the United States economy to this very day. It also will account for the mediocre economic growth that the United States will experience for the next four or five years.

Essentially this credit inflation laid the foundation for all the private sector credit expansion that took place during this fifty-year period and for the financial innovation that dominated the country in the latter part of the last century.

Over the past fifty years, the Gross Public Debt of the United States increased at a compound rate of growth of approximately 8.0 percent. Private debt rose somewhere between a compound rate of 10.0 percent and 15.0 percent.

All of these figures exceed the growth rate of the economy, which averaged a compound rate slightly in excess of 3.0 percent.

When credit growth exceeds the rate at which the economy can grow, that is called “credit inflation.” A good portion of this credit inflation has gone into consumer prices, but even more has gone into asset prices, or, has gone offshore.

The Gross Public Debt stands around $15.0 trillion as of this last October. In just the past three years this figure has grown by about $4.0 trillion.

If this pace is continued, the Gross Public Debt will rise by more than $13.00 trillion over the next ten years, slightly below the forecast I have been putting out for the last year or more, which is $15.0 trillion or more. I have argued that, given current attitudes, the government’s debt outstanding will double in the next ten years.

I feel much more comfortable, at this time, arguing that the debt will double in the next ten years than I do that the debt will increase by only 50.0 percent or 75.0 percent.

I have very little faith, at the present time, that much will be done to divert us from the path that we are on. And, just ten years ago we were experiencing a surplus in the government’s budget.

It comes as no surprise, therefore, that I am not surprised in the breakdown in the deficit talks of the Congressional supercommittee. There is no leadership in Washington to bring about a change in direction. The President’s ability to lead the situation is almost non-existent given the evidence of the recent polling data on support. And, Congress is even less able to lead given that polls on the public’s confidence in it are substantially below that of the President.

The problem, as I see it, is that the leadership style of the President is to state, in general, what he would like…a health care bill, a financial reform act, an increase in the debt ceiling, and a deficit reduction plan…and then turns it over to Congress to come up with a plan.

The Republicans in Congress knows that they will not be punished if they stand up and take a very intransigent position. They have become very direct in this in the last two skirmishes, because they knew that there was no way they would be called out. They learned this from the first events surrounding the development of the health care bill and the financial reform act. The Democrats in Congress have just been left out to “hang”. You really don’t hear anything from them anymore. They know they have the weak hand.

So, I continue to predict that the federal debt outstanding will grow…and grow…and grow.

And, as the debt continues to grow, the value of the dollar will continue to trend downward. Over this time period the debt of the United States government has trended upwards.

Since 1971, when the dollar was taken off the gold standard, the dollar has declined in value by about 33.0 percent. Since 1971, the debt of the government has increased by 39 times. The reason that the dollar has not declined by more is that other countries have followed policies that are similar to those of the United States and the U. S. dollar is still the reserve currency of the world.

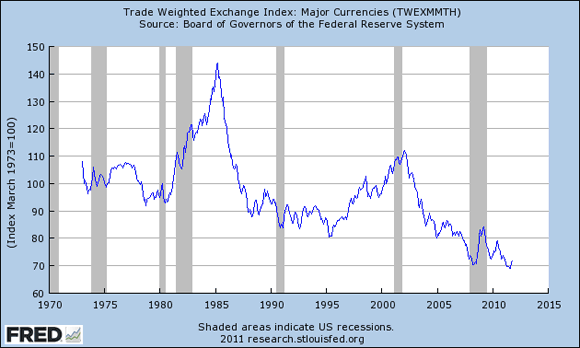

As the debt continues to grow, the value of the dollar continues to decline. Here is the chart of the value of the U. S. dollar against other major currencies over the last ten years.

The chart begins near the start of the Bush (43) administration. The two years previous to the beginning of the Bush (43) administration, the federal budget was in surplus. As can be seen, the value of the dollar was about 10.0 percent above the level it was at the time the dollar was removed from the gold standard. As federal deficits rose through the last decade, the value of the dollar continued to decline, reaching historic lows earlier this year.

Thus, I continue to be a pessimist about the ability of the United States government to get its budget under control and I continue to be a pessimist about the future value of the dollar. We cannot expect to see the value of the dollar really get stronger until we achieve some control over our fiscal affairs.

Given this view about the future, I continue to be a pessimist about the ability of the United States to maintain its economic lead on the rest of the world going forward. (link) Right now, that is the environment I believe businesses and investors should prepare for.

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply