The stock market has looked scary. But economic indicators suggest U.S. growth is continuing.

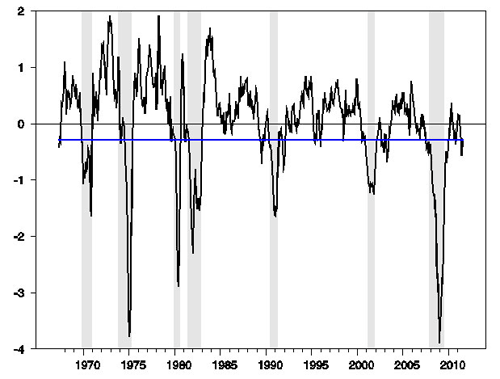

Last week the Federal Reserve Bank of Chicago released its National Activity Index, which summarizes the common tendency of a large number of indicators previously reported for August. The 3-month average of this index now stands at -0.28. We’ve seen this number that bad in 26% of the months since 1967. 59% of the time when the CFNAI was this bad or worse, the economy was already in a recession.

3-month average of the Chicago Fed National Activity Index. Shaded regions indicate NBER dates for U.S. recessions, with blue line drawn at -0.28, the latest value.

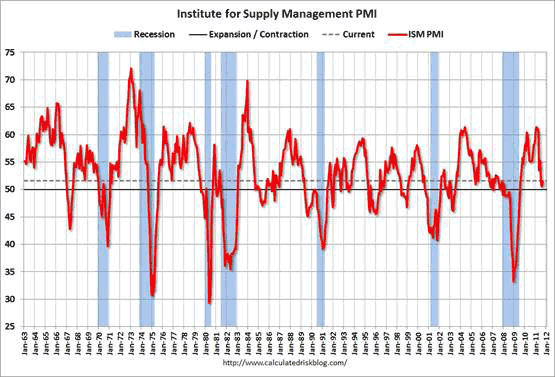

But the indicators coming in so far suggest that September was a little better than August. The ISM survey of managers of manufacturing facilities resulted in a value for their PMI index of 51.6 for September, up from 50.6 in August. A value above 50 indicates that more responders reported improvements than reported deteriorations. Still, we should see a majority reporting improvements if the economy were growing, and the average historical value for this index is 52.7. The September PMI is thus consistent with the conclusion that growth picked up a bit from the very disappointing August, but remains below average. The ISM non-manufacturing index for September was reported today to be 53.

Manufacturing PMI. Source: Calculated Risk

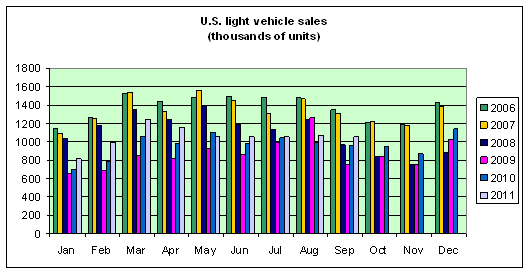

U.S. auto sales also suggest some improvement. The number of light vehicles sold in September was up 9.8% from September 2010, and down only slightly from August, significantly improving on the usual seasonal drop-off.

Data source: Wardsauto.com

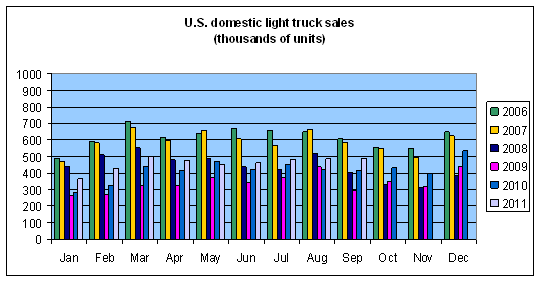

Sales of domestically manufactured light trucks were up 16.9% over September 2010 and even up slightly over August 2011. In part because of where we started out the year, the domestic auto sector has so far avoided a big hit to demand. This is one of the features that led me to conclude that the oil price increases earlier this year would not be enough by themselves to bring about a recession.

Data source: Wardsauto.com

The most important indicator for September will be the employment report due Friday. ADP estimated today on the basis of the 23 million employees whose payrolls it maintains that nonfarm private business sector employment increased by 91,000 workers on a seasonally adjusted basis between August and September. If true, that would be disappointing, since we should get about 45,000 jobs added back in from settlement of the Verizon strike alone. In addition, public sector cutbacks will likely continue to put a drag on total employment.

My biggest worry continues to be developments in Europe. The fiscal cutbacks and uncertainty will be enough to reduce growth significantly on the continent. And the possibility of disruption of interbank and private lending remains quite serious. I’m having a hard time seeing how the sovereign debt story will have a happy ending.

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply