I think a lot of Chris Whalen over at Institutional Risk Analytics, so I tuned in CNBC to listen to him this morning. At one point the discussion turned to Europe and Chris made it clear:

There are growing funding issues at some European banks

David Faber jumped out of his chair and challenged Whalen. He implied that Chris was making things up and spreading rumors. I was a bit surprised. It was if Faber was defending the Euro banks.

Faber is an ass. He doesn’t read newspapers either. Two recent headlines:

My understanding from talking to Europe again the morning is that there is a constant drain of dollar funding from highly rated core European banks. I’m absolutely confirming what Whalen has separately heard.

Behind the problems are US money market funds. They have been reducing their exposure to the big “safe” Euro banks. This process has been ongoing for some time. It’s not news at all.

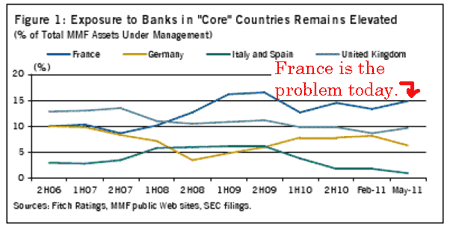

This chart from Fitch shows where the exposures were at the end of June. Note that there is not much outstanding for Spain and Italy, but you can be sure that even those numbers are much lower today. Germany is relatively small; the reason is they don’t pay much for deposit money. But look who is a total of 15% of all US money funds. France.

A US money fund that is either facing redemptions (they are) or who just wanted to reduce Euro bank exposure there is only one place to go; France. And that is what is happening. I have no idea of the volume of this unwind; my instincts tell me it is pretty large. It accelerated today.

It’s only Wednesday. There is a lot of time to worry about this before Friday. Normally big developments in Europe have happened over a weekend. That may not be case this time around. The markets may force the global finance leaders to move more quickly to (try to) stabilize things.

The mechanism is already in place. The US dollar swap agreements can be used at any time. A trillion of liquidity could be provided very quickly. It would require that the central banks of Europe on-lend the liquidity to the commercial banks. That would solve the solvency issue. It would be the equivalent of a Euro TARP. A semi-nationalization of the banks.

I wrote yesterday that I was dumfounded by Bernanke’s decision to extend ZIRP for two years. This unprecedented step has huge risks attached to it. Bernanke is well aware of that. Why did he risk it all? He must have known that there was soon to be a very big sucking noise from Europe. One that would require the USA to lend Europe some very big bucks.

I have some sense of what is going on in the background. Chris Whalen has a much better idea than I. But the big shots at the major banks know exactly what is going on the funding markets. After all, they ARE the funding markets. I can assure you that central bankers and treasury officials are all talking as well.

So if your wondering why stocks are tanking and bonds are soaring it’s because the news on this is already out. It’s just not in print. A thanks to Chris Whalen for putting this so squarely on the table.

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply