How did we get a housing bubble? This column describes how well households predict the market values of their homes. Most homeowners overestimate the value of their properties by 5% to 10%, primarily due to the large expected capital gains implicit in the self-reported home values. Overly optimistic expectations about the evolution of house prices may have planted the seed of the current mortgage crisis in the US.

Housing wealth is one of the pillars of the well-being of Americans families, especially because it represents more than 60% of the average net wealth of US households, according to the Federal Reserve’s 2004 Survey of Consumer Finances (SCF). However, we know relatively little about the ability of households to predict the market value of their homes in the context of household-level representative surveys and using data on sales prices of those properties. Understanding the accuracy of self-reported housing wealth is of great importance in a variety of contexts, since it is a pervasive explanatory variable (either by itself or as a component of net individual or household worth) in just about any empirical analysis or behavioural model of individuals’ and households’ decision making. For example, it is a key variable in decisions such as retirement, consumption, savings, and the debt composition of the household.

In a recent paper (Benítez-Silva et al. 2008), we take a closer look at the accuracy of self-reported housing wealth, using the Health and Retirement Study (HRS). A rarely used section of the HRS provides very detailed information about real estate transactions by households, which allow us to repeatedly observe self-reported house values, as well as the selling prices of properties sold in the 1994 to 2002 period. We compare these self-reported housing values with self-reported sale prices. This enables us to estimate a sales-price equation as a function of self-reported housing wealth in the previous interview of the panel study.

Our estimates suggest that homeowners on average overestimate the value of their properties by 5% to 10%. We also show that the overestimation is primarily due to the large expected capital gains implicit in the self-reported home values, especially since the mid-1980s. The measure of the expected capital gains is obtained by subtracting the self-reported original purchase price from the self-reported value of the home. The difference shows us the amount that the homeowner believes his or her house has appreciated.

We re-estimate the equation discussed above, substituting the original price and the (unrealised) expected capital gains for the self-reported house value. For individuals who accurately assess the market value of their properties, we would expect that both coefficients equal to one. On theoretical grounds, we expect the capital gains effect to be less than one due to the fact that individuals are unlikely to set their reservation selling price below the original nominal price they paid on the property, implying a coefficient associated with the original price variable of no less than one. This means that individuals use the original price as a reference point when determining what offers to accept.

The estimates suggest that homeowners are, on average, much less accurate with respect to their assessment of the role of capital gains for the value of the house compared to the role of the purchase price. Specifically, the marginal effect of the capital gains variable is estimated to be around 0.91, indicating that homeowners may significantly overestimate the contribution of the capital gains on the sale price. On the contrary, the original purchase price is reflected almost one to one in the selling price. This result is consistent with the idea that homeowners are unlikely to accept offers below the original priced paid on the properties.

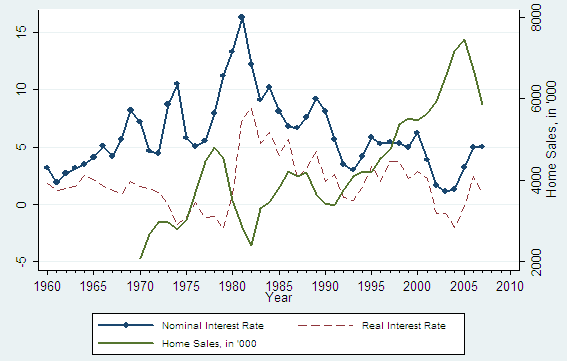

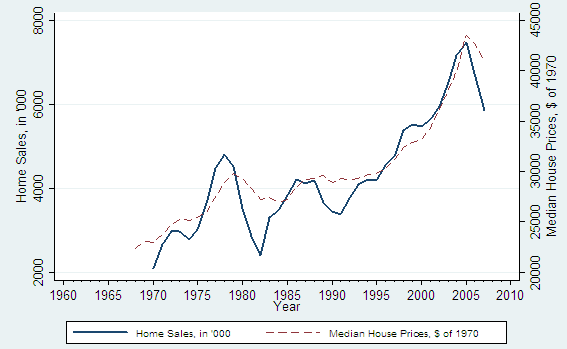

The latter result suggests a possible role for business cycle effects on the accuracy of the estimates through the characteristics of the period in which the household bought the property they eventually sell. In fact, we find considerable variation in how accurately homeowners predict the value of their properties depending on when individuals bought their homes. Given the characteristics of our data on house purchases and house sales, we observe properties purchased as early as 1955 until 2000. This information enables us to explore whether the timing of the purchase and the market conditions at that time could have lasting effects on the accuracy of the individual in reporting the value of their homes. We document a strong correlation between the evolution of our accuracy estimates over time and the business cycle. In periods of high interest rates and declining incomes, the buyers are likely to have lower appreciation expectations due to the declining housing prices (see Figures 1 and 2), and end up assessing, on average, more accurately the value of their homes, and even in some cases underestimating it.

Figure 1. Interest rates and home sales in the US, 1960-2007

Figure 2. Home sales and home prices in the US, 1968-2007

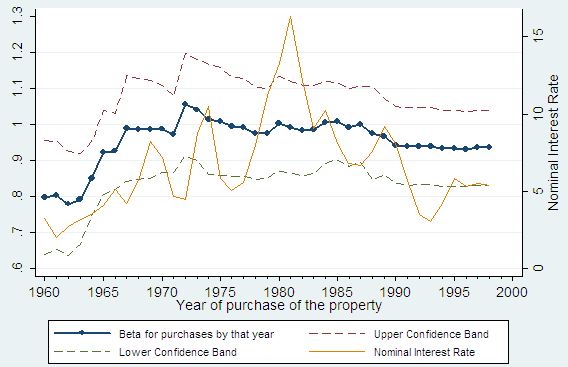

We find (see Figure 3) a strong positive correlation between the evolution of our estimates and the interest rate; the correlation coefficient between the series of our estimates and the interest rate is 0.566. In fact, a regression of our estimated coefficients on the series of interest rates and a constant, delivers an R-square of 0.32, and a very significant positive coefficient on the interest rate measure. The increasing trend of the interest rates up to the early 1980s translates in a trend towards an eventual decrease in overestimation of the properties and in some periods towards a slight eventual underestimation of the house values. The 1990s, a time of mostly falling interest rates is correlated with a trend towards overestimation of housing values.

Figure 3. Estimated β coefficient with confidence bands and interest rates

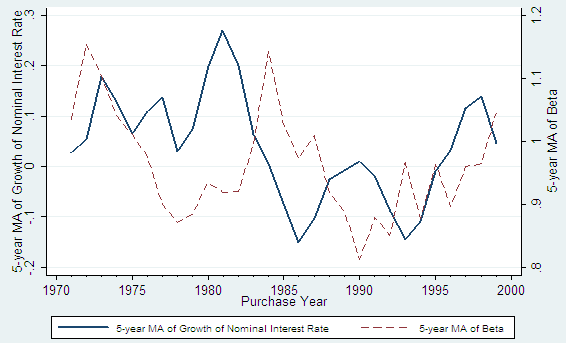

Figure 4. 5-year moving average of estimated β coefficients and of the growth of nominal interest rates

Comparison of our coefficients with other market variables further supports the evidence of the counter-cyclicality of the accuracy estimates (or cyclicality of the presence of overestimation). Periods of declining median household income (measured by the 5-year moving average of the growth of household income) and active expanding monetary policy (measured from the 5-year moving average of the growth in nominal interest rates) are associated with more accuracy in the estimation (and even underestimation) of the value of the properties (see Figure 4). One likely explanation for this evidence comes from the trends in the growth of housing prices over recent decades. While most individuals overestimate the value of their homes (some by as much as 20%), those who acquire their properties during economic downturns (and a slowing housing market) tend to be more accurate, and in some cases even underestimate the value of their houses.

These results establish a surprisingly strong, likely permanent, and in many cases long-lived effect of the initial conditions surrounding the purchases of properties on how individuals value them. Our interpretation is consistent with the link between nominal interest rates and the formation of housing prices appreciation expectations emphasised by Harris (1989), and more recently by Mishkin (2007). Moreover, it is in broad agreement with the relationship between states of the economy, the housing market, and housing price appreciation expectations discussed in Case and Shiller (1988), where good economic times (housing booms) are associated with very optimistic expectations of buyers regarding the evolution of housing prices.

In addition to a possible lasting effect of the housing cycle on the expected pace of home appreciation, the cyclical nature of the accuracy may also reflect changes in the composition of buyers during the business cycle, with richer, more educated buyers entering (or re-entering) the market in rougher economic times. We find that those who bought during more difficult economic times, especially the early 1980s, tend to be more educated, with an 80% of them having a college degree or more, compared with less than 60% during other periods. Given the correlation of education with income and wealth, this is in line with the discussions in Harris (1989).

All this suggests that in good economic times there is a larger number of buyers who are (eventually) overly optimistic regarding how much their properties are worth. This is precisely what is believed to have happened since the beginning of this decade and until 2005-2006, when a wave of buyers (many of them first-time owners, which pushed the homeownership rates to historic highs in the 2003-2006 period), responding to easy credit conditions and with possibly overly optimistic expectations about the evolution of house prices, planted the seed of the current mortgage crisis in the US by accepting mortgage terms that were set to explode in the short to medium run, and making them more dependent on price appreciation to build equity in order to accommodate adverse events such as an increase in the interest rates.

References

•Benítez-Silva, Hugo, Selcuk Eren, Frank Heiland, and Sergi Jiménez-Martín (2008): “How Well do Individuals Predict the Selling Prices of their Homes?” Working Papers 2008-10, FEDEA.

•Case, K.E., and R.J. Shiller (1988): “The Behavior of Home Buyers in Boom and Post-Boom Markets,” New England Economic Review, November-December, 29—46.

•Harris, J.C. (1989): “The effect of real rates of interest on housing prices,” Journal of Real Estate Finance and Economics, Vol. 2-1, 47—60.

•Mishkin, F.S. (2007): “Housing and the Monetary Transmission Mechanism,” NBER Working Paper Series No. 13518.

![]()

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

I would dare insert that most homeowners are over estimating the value of their property much closer to the 10% level in this current economy. Home values are falling much faster than homeowner expectations.