I must admit that I surprised by the tepid response to the advance release of the 4q2010 GDP data. Mark Thoma catalogues the most common critiques – the negative contribution from government spending and the minimal reduction in the output gap. My review of the data differs. In my opinion, this is the first GDP report since the recession “ended” that offers a certain optimism, a glimmer of hope that perhaps that light at the end of the tunnel is not simply an oncoming train. If it is an oncoming train, it not the train of sagging government spending, but instead a train of imports blasting forward.

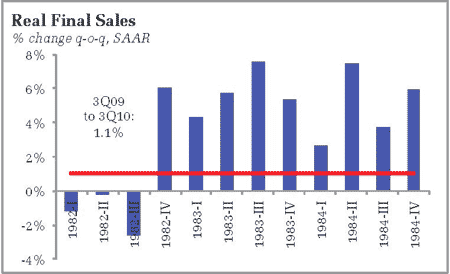

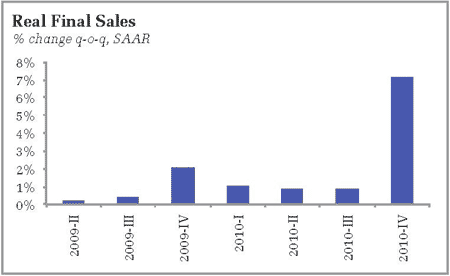

It is no secret that this recovery, to date, has been anything but vigorous. Certainly nothing like the “Morning in America” of the mid-80’s. Real final sales – GDP excluding inventory effects – outperformed for quarter after quarter during that period as demand clearly outstrip the pace of capacity growth. In comparison, real final sales during the most recent recovery has been almost laughable:

But real final sales surged in the final quarter of 2010:

A 7.1 percent gain is nothing to sneeze at – and, realistically, in the scope of that kind of surge in final demand, the 0.11 percentage point reduction from the government sector is little more than a rounding error (I would be more worried about the loss of services than the contractionary impact in the context of 7.1 percent final demand growth). This is exactly the kind of final demand growth needed to lift us out of this morass.

But is it sustainable? What is apparent from this report is the potential for external support to generate real improvement in the US economy. The sharp drop in imports meant that firms were forced to sharply reduce the pace of inventory growth. Will those inventories be replenished with domestic or foreign production? James Hamilton is not optimistic:

But the fact that a huge negative contribution of inventories coincided with a huge positive contribution of imports does not seem to be a coincidence. There’s a clear pattern in the recent data that when one of these makes a positive contribution to GDP growth, the other makes an offsetting negative contribution. Although we often think of inventories as a substitute for production (you could either produce a good or sell it out of inventories), in the current environment inventories seem to act more as a substitute for imports (you could either import the good, or sell it out of inventories). So although inventories shouldn’t be the same drag on GDP in 2011, I expect imports to go back up and exert a drag of their own.

Sadly, the story of this recovery continues to circle around the external accounts. Absent a resolution of the global rebalancing story, faith in fiscal stimulus is somewhat misplaced – much government spending will simply leak abroad as evident in previous GDP reports. Of course, the alternative, fiscal policy that ignores the recession, is not exactly an endearing policy course. If rebalancing continues to be delayed in the months ahead, US policymakers simply must accept the trade deficit will reduce the effectiveness of their efforts.

Moreover, the resistance to rebalancing is nothing less than sadly ironic, as rebalancing produces the only possible win-win scenario in the global economy. Consider that concerns of emerging market inflation suggest that demand is surging ahead of capacity, while deflation in the US suggests the opposite, excess capacity. It seems that these problems are two sides of the same coin, with an obvious optimal solution – greater currency flexibility. Emerging markets could satisfy higher rates of domestic demand growth via declining net exports, while rising net exports allows for higher capacity utilization in the US. In effect, global consumption power would be redirected toward relatively poor economies and away from a relatively rich economy. It seems quite reasonable.

Alas, instead we are faced with the challenges of rising inflation in some nations, and increasingly disturbing hoarding behavior in others. While stories of a massive stock of empty housing in China have long circulated, the Wall Street Journal reports that the hoarding has reached a new level:

The amount of cotton held in hamlets throughout China is unknown, but, with 25 million cotton farmers, a Chinese cotton agency estimates it could amount to about 9% of the world’s cotton supply. And the situation is occurring throughout the supply chain. Many ginners and merchants in China are keeping warehouses full, according to the agency, in an attempt to obtain higher prices.

Expectations that prices will rise are driving the apparent stockpiling, which causes short-term shortages and leads prices to rise further. The situation is complicating an already volatile picture for cotton, which has jumped to 140-year highs in the U.S. and has become a symbol of brewing commodity inflation around the globe.

Included in the story is a picture of a farmer storing 7,700 pounds of cotton in his home (I suspect my wife would object should I start taking a long position in hog bellies via physical possession in the living room). To be sure, such behavior, like stockpiling empty houses, makes sense in an inflationary environment in which agents are desperate to find adequate stores of value.

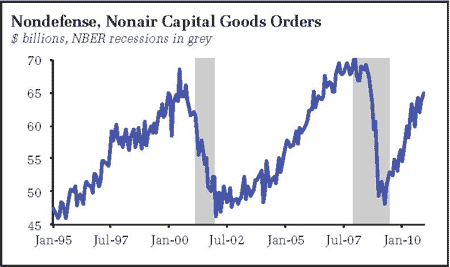

Regarding other data, last week we also saw the December durable goods report. While there was some concern over the headline numbers, it is generally safer to go straight to the core figures, capital goods excluding defense and air:

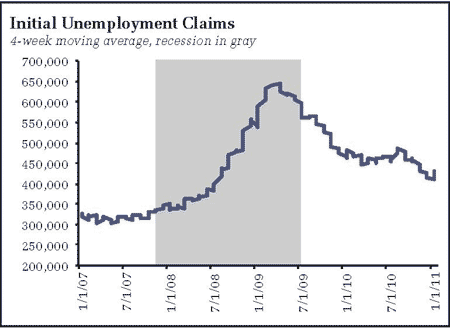

Looks like the economy shook off the summer slowdown, putting order back on the uptrend. Somewhat disappointing was the partial reversal of recent improvement in initial unemployment claims. That said, looking at the four-week moving average, the downtrend looks intact:

Of course, if final demand is growing at a 7.1 percent pace, the overall improvement in the final months of 2010 should come as no surprise. Finally, also not surprisingly, the Case-Shiller Index reported ongoing home price weakness. Housing has offered almost nothing to the recovery and, quite frankly, is yesterday’s story. Housing is returning to its appropriate place in the economy – a product that provides a service, not an investment or, worse yet, a gamble.

Bottom Line: The GDP report revealed what could be, the glimmers of hope of a V-shaped recovery. If final demand even near the 4q2010 could be maintained, Federal Reserve policymakers makers would be forced to take notice by mid-year. Still, setting aside the usual risk factors (including the fresh possibility that Mideast unrest triggers a fresh oil shock) the sustainability of this final demand is directly dependent upon the evolution of the external accounts. If this demand surge is satisfied with an import surge in coming quarters, we can expect the recovery will remain tepid in comparison to previous deep recessions. If rebalancing were to maintain some traction, this could be simply the first in a long-waited string of data that would proved a clear exit to the current period of relative economic stagnation.

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply