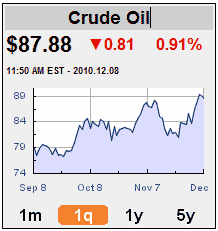

The price of oil moved above $90 a barrel yesterday. Is it time to become concerned about the possible macroeconomic effects?

The price of oil moved above $90 a barrel yesterday. Is it time to become concerned about the possible macroeconomic effects?

In the early part of this decade, consumers seemed to be largely ignoring oil prices, in part because energy expenditures had become a smaller part of their budget than they had been in the late 1970s. But as the price of oil rose over the decade, energy expenditures returned to a position of importance in consumer budgets. I’m persuaded that the oil price shock of 2007-2008 made a measurable contribution to the initial downturn of the Great Recession.

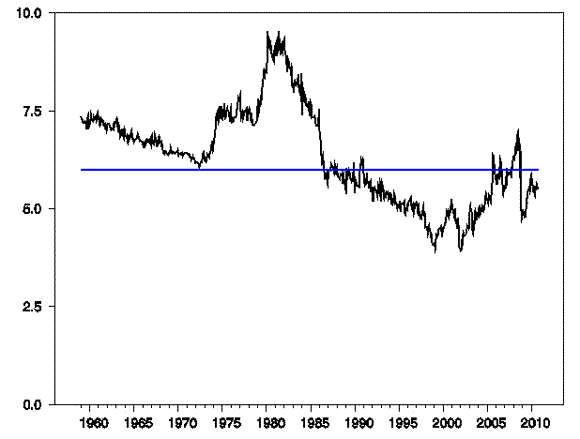

Based on the BEA breakdown of consumer expenditures, as of October consumer spending on energy goods and services constituted 5.5% of total spending, a bit below the 6% levels at which we saw significant consumer responses two years ago.

Energy expenditures as a percentage of consumer spending. Calculated as 100 times nominal monthly consumption expenditures on energy goods and services divided by total personal consumption expenditures. Data source: BEA Table 2.3.5U. Blue line is drawn at 6.0%

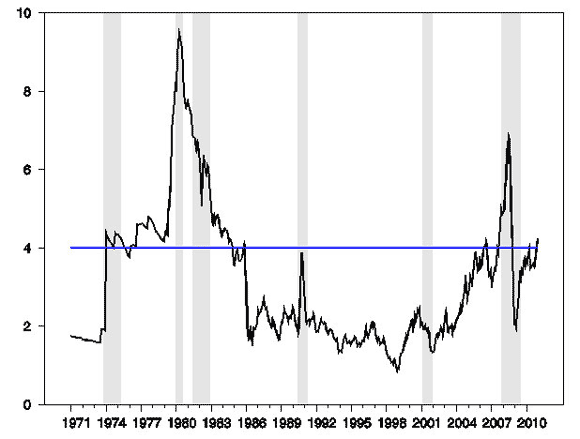

But crude oil was selling for $75 a barrel in the fall, and has made a significant move up since then. Steve Kopits suggests using a rough estimate of the monthly value of U.S. crude oil purchases as a percentage of GDP, and concludes that the economy stumbles when this gets above 4%. If oil stays above $90 a barrel for December, that would probably put us above that threshold.

Oil expenditures as a percentage of U.S. GDP. Recessions are indicated by shaded areas and blue line is drawn at 4%. Oil expenditures calculated as average monthly price of West Texas Intermediate (from FRED) times 365 times average daily petroleum product supplied to U.S. markets over the last 12 months (from EIA). Nominal GDP from quarterly BEA Table 1.1.5 interpolated to form a monthly series. Recessions drawn as shaded areas. Figures for 2010:Q4 use following estimates: nominal GDP grows at a 4% annual rate from Q3, oil consumption grows at a 2% annual rate from Q3, and oil price for December 2010 averages $90/barrel

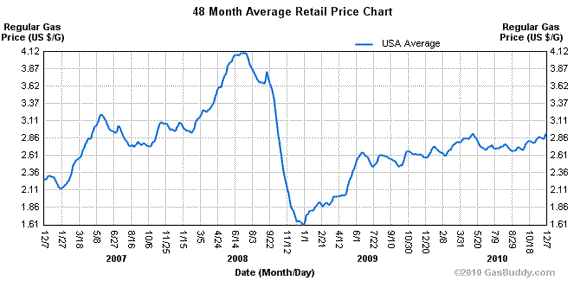

Academic research suggests a nonlinear response of GDP to oil price changes. The abruptness of the price increases in 2007-2008 likely contributed to their disruptiveness on other categories of consumer spending. The price of gasoline has moved modestly up over the last year, but is still well below the levels we saw in 2008. The model many researchers have been using implies that oil prices only start to matter when they make a new 3-year high. We probably won’t have to worry about crossing that threshold until June of 2011, which would put the big spike in oil prices 3 years behind us. But really those models are just a guess– we don’t have the ability to make precise inferences about the details of these nonlinear responses on the basis of the available data.

Average U.S. retail price of gasoline (dollars per gallon). Source: NewJerseyGasPrices.com

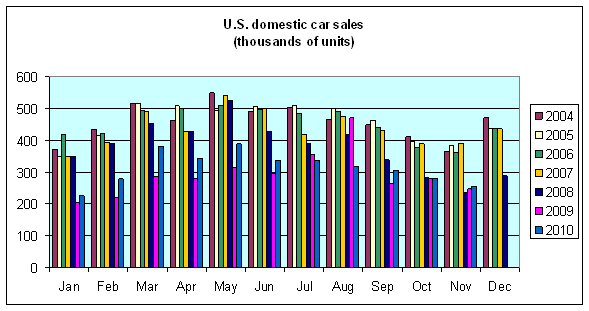

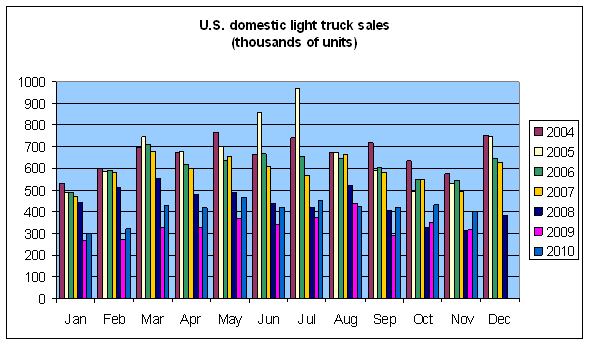

An oil price increase that simply reverses a recent decline seems to have a more modest effect on the economy. One of the reasons is that patterns of consumer spending are still based in part on the expectation that oil prices could go back up where they were in recent memory, so that if they do go back up, the changes in spending aren’t that dramatic. However, the recent modest rebound in auto sales seems to have been led by light trucks and SUVs rather than cars– the auto sector is more vulnerable to these developments today than when it was flat on the bottom a year ago.

Data source: Wardsauto.com

Data source: Wardsauto.com

I could certainly imagine that an abrupt move up in gasoline prices from here could hurt the struggling recovery of the domestic auto sector and dampen overall consumer spending. I do not think it would be enough to give us a second economic downturn, but it could easily be a factor reducing the growth rate.

And the growth rates most of us had been expecting with oil still at $75/barrel were not all that hot.

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply