According to the ‘June Oversight Report’ released today by the Congressional Oversight Panel (COP),” bank stress tests should be repeated if the unemployment exceeds rates beyond levels assumed by federal regulators in a recent round of examinations on the nation’s 19 largest banks. “We recommend that Treasury publicly track the status of its stress test macro-economic assumptions (unemployment, GDP, and housing prices) and repeat the stress test if the adverse scenario assumptions have been exceeded,” the panel said in the report.

The COP monthly report, led by Harvard Law School Professor Elizabeth Warren, also touched on the commercial real estate (CRE) loans situation, whose fundamentals continue to get dramatically weaker across most major property segments:

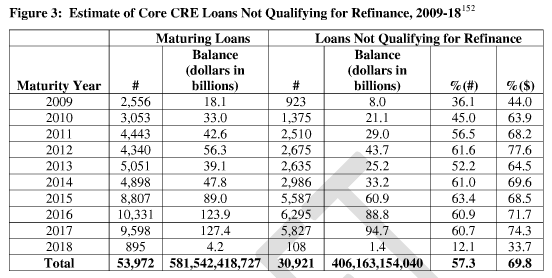

From COP: [B]anks hold $1,068 trillion in core [CRE]. A recent study commissioned by Deutsche Bank suggests that the majority of losses on CRE loans made in the easy credit years (e.g., 2005-2007) will reach maturity and will in many instances fail to qualify for refinancing:

As the report explains, the high percentage of loans not qualifying for refinancing, and hence in danger of default without significant injections of new equity, is attributable to the combined effects of stricter underwriting standards, steep declines in property values, and reduced income streams to finance the loans because of lower rents and increased vacancies. The findings are based on quantitative data for commercial mortgage-based securities (CMBS), which constitute 25 percent of the core CRE market. While the authors of the report state that there was insufficient data to perform a detailed study in the larger non-CMBC sector, the authors say they expects a similar if not higher level of maturity defaults on non-securitized CRE bank portfolio loans because portfolio loans typically have shorter maturities (which would not allow sufficient time for property values to recover from ther present depressed levels) and higher risk profiles than CMBS…The extent to which the stress tests, which were never intended to look more than two or three years in the future, fully grapple with prospect of massive future CRE loan defaults is uncertain.

emphasis added

Table: COP

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply