Did the first quarter mark the end of the fiscal stimulus? And will it be enough to work?

People are always trying to judge the fiscal stimulus by whether it creates jobs. But that was never the real justification for spending all that money. The theory was that the economy has multiple equilibria–a good equilibrium where everyone is optimistic about the future, companies invest, and households spend, and a bad equilibrium where everyone is locked into a mutually reinforcing gloom about the future. Then a big enough fiscal stimulus can forcibly kick the economy from the bad equilibrium to the good equilibrium.

The key term here is ‘big enough’. I think of the stimulus as a big booster rocket for the economy. If the rocket is strong enough, it can put a satellite (the economy) into a stable orbit. Not enough boost, jobs are created by spending money, but the economy falls back to earth again once the stimulus stops (wow, that was a mixed metaphor, but I’m good with it).

By this measure, the stimulus can only be judged successful or not after it stops firing. Or to put it another way, we want to see if the private sector continues to grow once the government stimulus is removed.

As it looks like tht critical moment has arrived. Based on the latest BEA data, the stimulus ran out of fuel in the first quarter, and we’re about to find out whether it gave the economy enough oomph to get back into orbit.

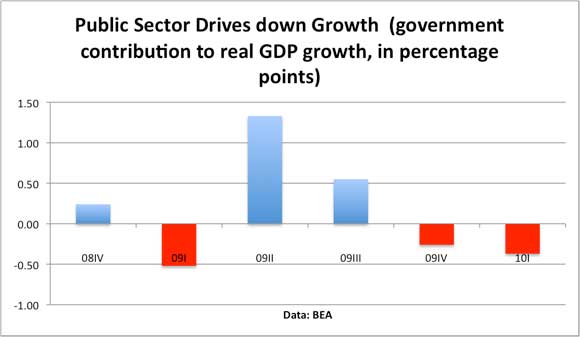

Take a look at these two charts. First, the government contribution to GDP growth was negative in the first quarter–roughly one-third of a percentage point. This reflects mainly contraction of state and local governments–layoffs and reductions in investment. Basically any new building projects on the state and local level have been put into the cold freeze.

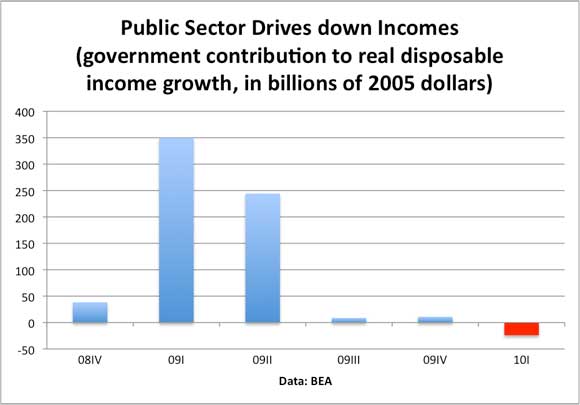

But the GDP stats don’t tell the full story, because transfer payments (Social Security, Medicare, unemployment insurance) are not included in the ‘government’ category of GDP. Instead, they show up in personal income. So I calculated the government contribution to real personal disposable income growth. That includes the change in government benefit payments and government wages and salaries, minus the change in income taxes and payroll taxes.

Surprisingly–at least to me–the government was a net drag on real disposable income growth in the first quarter of 2010. A small drag to be sure–roughly 0.2% of disposable income–but certainly not a boost. An increase in benefits was more than offset by an increase in taxes paid.

In other words, the fiscal stimulus pretty much petered out in the first quarter.

So the second and third quarters will be key. Will the private sector be able to use the boost from the stimulus to get back into some reasonable economic orbit? Or will it fall back to earth again in a big splat?

Right now I’m evenly balanced between the optimistic and pessimistic possibilities in the short-run. I see good signs of life, especially in the communications sector. But I worry about Europe, about cutbacks on state and local level, about trade and borrowing from overseas. But that’s a different post.

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply