If you went home happy and risked-up on Friday, you’ve probably seen a mushroom cloud rising over the ashes of your erstwhile-profitable portfolio, as the Europeans have engaged the nuclear option in response to the current crisis.

While the sums involved are not quite a match for those used by US authorities last year, they nevertheless reside in the same neighborhood (assuming they can be fully deployed); the zillion dollar question is whether they’ll have a similar impact.

How shall I help thee? Let me count the ways:

* €60 billion in cash from the European Commission, funded by bond sales

* €440 billion in loan guarantees, via pooled support of member governments

* Up to €220 billion from the IMF

* Outright bond purchases from the ECB, to be sterilized (this has evidently already started)

* 3m and 6m full-allotment LTROs

* Reactivation of FX swap lines

As always when it comes to Europe, Macro Man has to bite back scepticism. In this case, he finds himself switching from “show me the money!” to “wow, that’s big…who’s payin’?” with remarkable ease.

That is, of course, unfair…to a degree. But the remarkable ability of this situation to look hideous from every angle simply highlights the fundamental flaws in the Eurozone project (i.e., allowing any old country in, regardless of competitiveness, and the lack of a harmonized fiscal stance.)

Nonetheless, the immediate requirement for funding from European governments is not particularly high, which is probably a good thing given the spanking the CDU received in NRW over the weekend.

(One is also left to wonder how much a country like, oh, the US will be asked to contribute to IMF aid to Europe, and how well that will go down in a country with a gargantuan budget deficit and mid-term elections rapidly approaching. But I digress….)

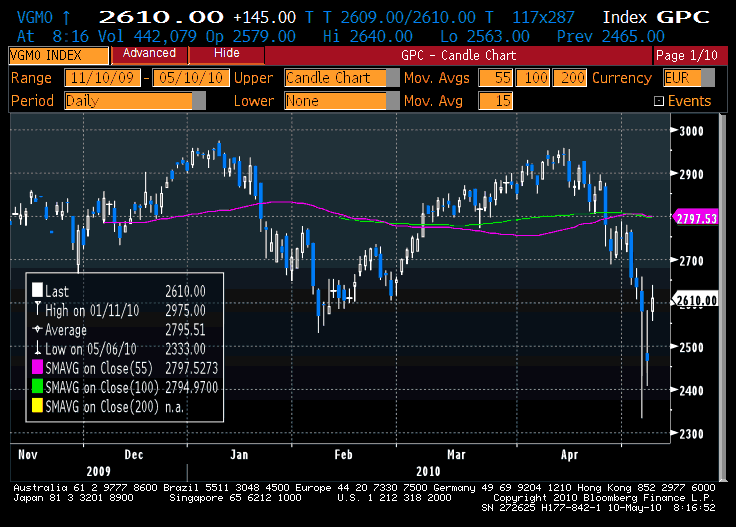

Unsurprisingly, all of this has brought about another 180 degree turn in market sentiment, and everything that was cratering at the end of last week is doing its best Superman impression (up, up and away…)

That’s a cheeky 6% in Eurostoxx…

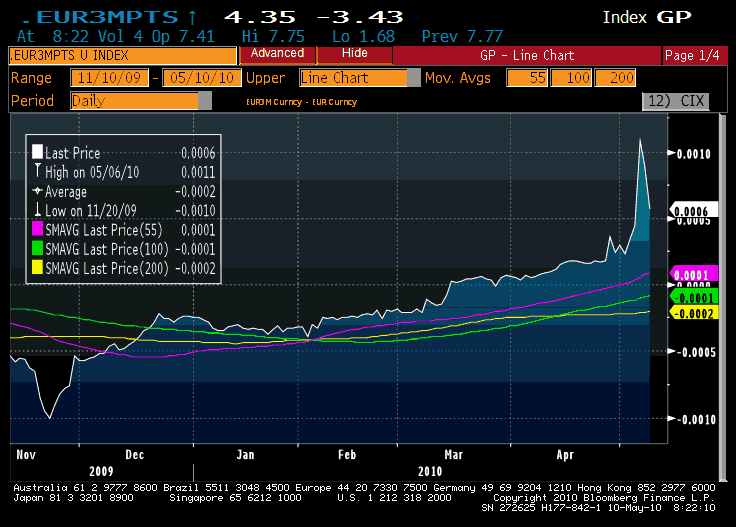

…and FX swap points have come back…though not all the way.

It is certainly tempting to point at the bounce off the market low of last March and extrapolate forwards, given that Europe has unveiled its version of QE and bailouts. And in the near term, there is no telling how far stuff can run.

As always in the Eurozone, conditionality and enforcement are paramount issues that will be tricky to solve. No doubt Portugal, Spain, et al. will say the right things and appear to toe the line…but what happens when growth undershoots and so do fiscal revenues? Which will give way…living standards for civil servants, or fiscal rectitude? (This, as an aside, is the primary argument for IMF involvement: so the German’s won’t have to play “bad cop.”)

So what we’re left with is that a financial firestorm with its genesis in private sector off balance sheet SPVs is being solved at the sovereign level with a limited-funding SPV to guarantee to the periphery. Niiiiceeee….

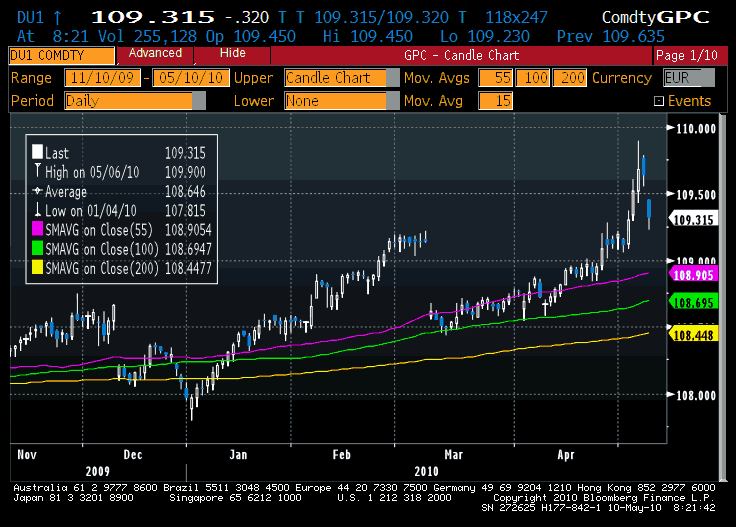

In the meanwhile, as risk asset and euro shorts lick their wounds, there would appear to be one trade that makes loads of sense: short Schatz. The Germans will be on the hook for quite a bit of whatever cash is required, and with Schatz yields still under 0.70% it makes a whole lotta sense to fund early and often.

Sadly, Macro Man has a visit to the dentist this morning, so euro and equity shorts won’t be the only ones in pain……

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply