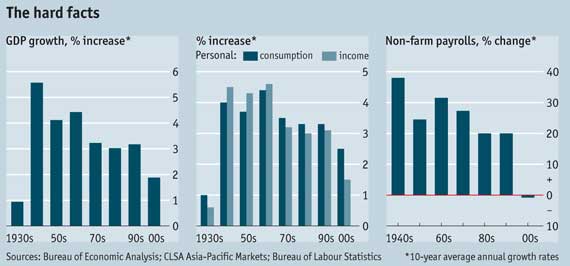

A few weeks back, The Economist published a story touting the well-known fact that the “American economy just had its worst decade since the 1930s.” Whether looking at gross domestic product (GDP), consumption, income, or nonfarm payrolls, the decade from 2000 to 2010 generally looks bad from an economic perspective. During this decade, of course, the nation has experienced two recessions—the latter being the most severe since the Great Depression. (See the graphs below, reproduced from the February 25 article in The Economist titled “Back to The Crash.”)

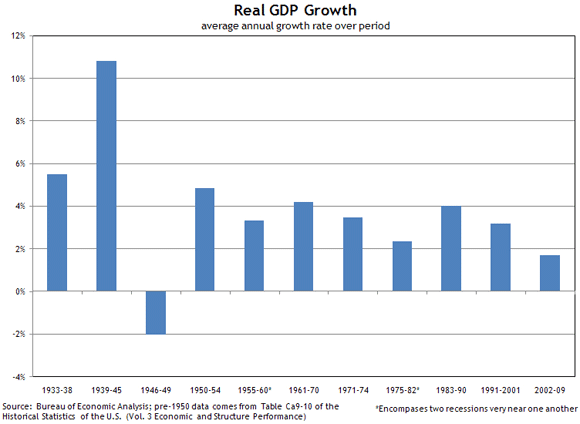

But given that decades are rather arbitrary economic demarcations, why not examine other time periods? So here’s another approach: Using the yearly trough-to-trough periods according to National Bureau of Economic Research (NBER) recession dating, the charts below have replicated the ones shown above from The Economist. (Note: The NBER only designates troughs by quarter. So for a trough ending in first or second quarter, the calendar year in which the trough falls is designated as the “trough year.” If the trough falls in third or fourth quarter, the following calendar year is the trough year. For these calculations, we use annual data instead of quarterly because pre-1947 quarterly data are unavailable.) This simple exercise sheds some interesting light on the recent experience of the U.S. economy—namely, that it was bad by any measure.

Looking at real GDP growth over these periods, the 2002–09 era looks very weak, with only 1946–49 having a lower average annual rate of growth (in these years, GDP averaged an annual decline of 2.01 percent). Average annual real GDP growth was 1.72 percent for the 2002–09 period, much lower than the average of 3.97 percent for the previous 10 trough-to-trough periods.

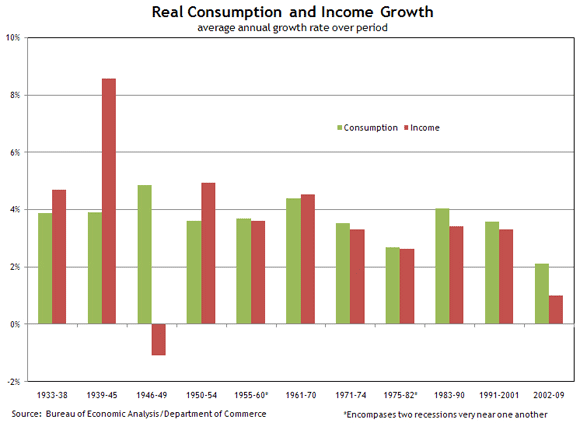

Similarly for real consumption and income growth, the 2002–09 period is also bleak. Average annual consumption and income growth had averaged 3.81 percent and 3.79 percent, respectively, going into 2002. But during this recent trough-to-trough period, income growth was very weak at 1 percent, with only the 1946–49 period doing worse (–1.09 percent). But consumption growth in 2002–09 was the lowest on record, averaging only 2.12 percent growth annually.

Another interesting observation is the spread between average annual consumption and income growth. The 1946–49 and 2002–09 periods are where it’s the largest, at 5.9 percent and 1.1 percent, respectively. These large imbalances could possibly reflect growth in household debt and/or lower saving rates, as consumption growth far outstrips income growth. Indeed, debt grew and savings declined notably during 2002–09.

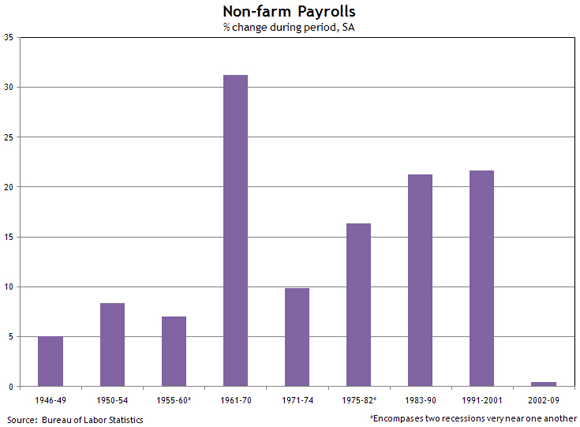

Lastly, a look at the nonfarm payroll growth confirms the most recent trough-to-trough period as one of extraordinary weakness. Given that data prior to 1939 are unavailable, the previous eight bottom-to-bottom periods saw average annual growth of 13.5 percent in payrolls. But for 2002–09, average annual payroll growth of 0.44 percent reaffirms the so-called “jobless recovery” from the 2001 recession and the large decline in payrolls during this current recession. No other previous period comes close.

By Andrew Flowers, economic research analyst, at the Atlanta Fed

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply