Remember when Obi Wan Kenobi lept up from that bottomless pit on Naboo and sliced Darth Maul in half? That’s what comes to mind when I think about today’s Citigroup news.

Citigroup’s (C) recent woes are a perfect reminder of what investors in corporate bonds and preferred stock are up against in 2009. Yes, government support is nice. But it isn’t everything.

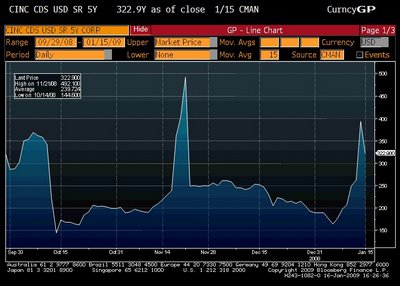

First the chart on Citigroup’s credit default swaps (CDS). Higher CDS rates (also called the spread) indicate a higher price to insure against Citigroup defaulting.

We see the CDS fall drastically on October 13-14, when the Treasury initially made TARP investments in Citigroup and several other banks. The spread then rose to nearly 500bps in late November before the government made another injection into Citigroup that weekend. Once again the spread plummeted, settling in the mid to low 200’s before rising in recent days. The chart doesn’t show it, but today’s announcement from Citigroup caused CDS to drop another 50 bps to +275.

The trading pattern is that Citi goes wider, the government steps in to help. So why worry? The Treasury is telling you that Citi is too big to fail right?

Step back and ask yourself why Citi is too big to fail. Its because of the interlocking nature of the financial markets. Its because Citi is a major counter-party to all stripes of derivatives. Its because Citi is a major market-maker in the financial markets. Etc. etc. It isn’t because Citi bond holders or preferred stock holders need to be protected.

Another way to read the CDS chart above is that Citi would have been bankrupt not once, but twice if it hadn’t been for government support. Now, I fully expect the government to continue to support Citigroup, but what is this new good bank/bad bank split going to look like for bond investors? Debt holders aren’t likely to be backed entirely by the good bank, because that bank would be over-leveraged. Some of the debt is going to go to the bad bank. It could wind up where the bad bank does some sort of tender and re-issue, and existing bond holders turn out just fine. But we don’t know that.

There was talk that Citi could be nationalized. Again, the simplistic investor is assuming this would be good for debt holders. But in a nationalization, the government would probably move to break up the bank even faster than what is currently underway. If Citi breaks into three pieces, which piece would bond holders be tied to? Before you make a guess, remember that if the government gets involved, anything can happen.

I’ve heard many times a recommendation to “buy what the government is supporting.” But I suggest investors take an alternate but similar approach. In the bond market, buy what the government is supporting to maintain liquidity, not what the government is supporting to avoid insolvency. There is now, or may be in the near future, strong government support of several bond sectors that would be money good anyway, but are trading cheap because of poor liquidity. Student Loan-backed bonds, municipal bonds, GSE-backed mortgages, etc. Why are people buying Citigroup bonds at around 6% yield with so much uncertainty surrounding it?

Citigroup is clearly a declining situation. It may well be that with government support, Citi survives and eventually becomes a thriving company again. But its also distinctly possible that in a break-up, bond holders are left with something less than full government support. Buyer beware.

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply