I’ve said this before in different ways, but I will say it once more, “Governments are smaller than markets; markets are smaller than cultures.” The reasoning is simple:

- Governments can only control a fraction of what an economy or culture does. Governments that are overbearing on an economy or culture may gain greater proportional control, but the size of the pie will shrink. More of the economy or culture goes into hiding, away from the prying eyes of the government.

- Markets only express a fraction of what mankind does. They cover the tradeable aspects of what we do, but typically do not give us our deeper goals or desires for ourselves, and the culture as a whole.

When I look at the biggest economic problems facing the world today, many of them stem from deeper cultural problems. Let’s start with the current poster child, or, canary in the coal mine, Greece.

Greece got into the Eurozone via subterfuge; they lied about the true status of their indebtedness, and Wall Street (with its counterparts in European investment banking) helped them do it. So did a number of the other nations in the Eurozone that are presently under stress.

Now, the core members of the Eurozone wanted the Euro to grow as a currency — they were committed to an ever-wider and -deeper union. The dream of a united Europe made them willfully blind to the low probability that the nations which were fiscal basket cases had genuinely changed. The core should have been skeptical, and now they are paying the price, though not paying any money, yet.

The core nations that could pay or guarantee to help Greece are playing a tight game. They act as an internal European IMF, insisting on reductions in the Greek budget deficit. Greece does its part by saying it hasn’t asked for aid, which is unlikely. At the same time, reductions in the Greek budget deficit bring the competing political factions inside Greece out in force. Protests! Strikes! There are few arguing for what is best for Greece overall, and many arguing for a larger piece of what is a shrinking pie. In a situation like this, it might be better for outsiders to let Greece fail,but they won’t do that. Why?

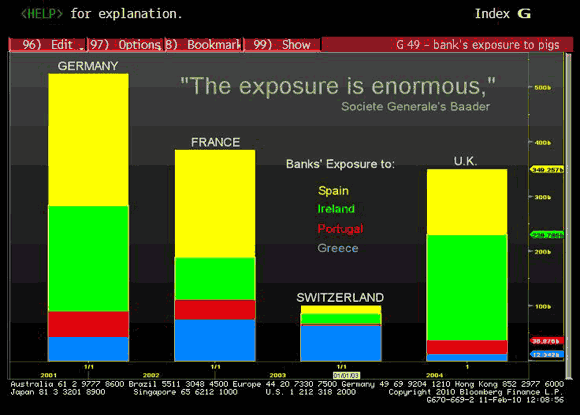

The banks in the core nations can’t afford a default by Greece if by contagion it leads to defaults in Portugal, Spain, Italy, and Ireland. A failure of the banking system does not conduce well to maintaining power for elites.

I have already talked about the perverse incentives for the core European nations to do anything to support Greece. If Europe was rational, they would abandon the experiment now, or press for a Federal Europe akin to the US. I don’t see either happening — I just see slow suffering for now, and futile playing for time.

Dubai is a place where anything can get done. Anything indeed, but who pays the bills? Dubai is a place of big ideas and little responsibility. It is a moral flaw to bite off more than you can chew, particularly if you do so on behalf of others.

Many US States and Municipalities are in a world of hurt, because they compromised their long-term financial position to solve short-run budget crises. That is the nature of the crises that we face today.

The same is true of the current US government — they fight for short term political advantage, rather than the long term good of the nation. Who will favor the long-term and sacrifice for the greater good?

A simple summary statement here is “Greed is not good.” Societies that are willing to sacrifice self interests have a much better probability of succeeding than societies that pursue self interest.

That’s all for now, I will pick this up in part II.

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply