Sterling, sterling, sterling. Macro Man’s email and Bloomberg in-boxes are filled with all things sterling today. The GBP can be a fun currency, not least because of the jokes that a guy like Macro Man can make with it (“sterling’s looking a bit tarnished”, “GBP = Gordon Brown’s peso”, etc.)

Thus far this morning, the British Pound truly has been Great, carrying on a trend of the past few days. Que pasa?

Well, there have been a few things driving sterling. The most obvious (and most credible) source of GBP strength has been the takeover frenzy surrounding Cadbury, with a host of foreign firms circling the purveyor of Creme Eggs like so many buzzards. It looks like Kraft (NYSE: KFT) has sweetened their offer just enough to make it palatable to the Cadbury (LON: CBRY) board; at a reported all-in price of 850p/share (including dividends), the whole business has been a tasty treat for Cadbury shareholders.

(click to enlarge)

More viscerally for sterling, however, is the 500p/share cash component of the offer. With 1,373,866,000 or so shares outstanding, that translates to a £6.9 billion cash bung to Cadbury shareholders from Kraft’s coffers. It’s always difficult to know exactly how and when the cash component of cross-border M&A deals will be effected, but it seems reasonable to assert that a decent chunk will need to be transacted in the marketplace. And contrary to the apparently common perception of non-experts (“but there’s $4 trillion of daily turnover!”), a time-sensitive flow of that magnitude that everyone knows is coming can have a significant short-term effect on the marketplace.

Of course, that effect will have long faded by the time that Kraft is able to jam American shelves with Fruit and Nut or Turkish Delight bars. And from there, sterling will be left to rise or fall on its own merits. In that regard, there are a couple more factors that bear watching. While Macro Man asserted in his list of non-predictions that the UK would avoid a hung Parliament, the risk of one is very real, given the farcically gerrymandered electoral districting.

In that vein, it is clearly worth keeping an eye on Labour’s electoral strategy, which has turned abruptly over the last week or two. Following on from an apparent declaration of class war a few weeks ago, Labour has performed an abrupt about-face (courtesy of the unpopularity of their prior strategy) and is now sounding almost Tory-ish. Noted creature of the underworld Peter Mandelson was in the weekend press suggesting that the 50% to tax rate would only be temporary, and today’s press is aflutter with Alistair Darling promising steep budget cuts, apparently stealing a key plank in the Tories’ election platform. ‘T would be tempting to call it Machiavellian, but that word connotes a degree of artifice that is notably lacking in most of the current crop of Labour politicos (with Mandelson as an obvious exception.)

It’s difficult to see how this will play out. A legitimate commitment to fiscal discipline should prove supportive for sterling in the medium term, though any near-term negative impact on growth could have the opposite effect. But if Labour’s naked play for the middle class convinces enough voters to generate a hung Parliament, the impact on sterling would almost certainly be negative.

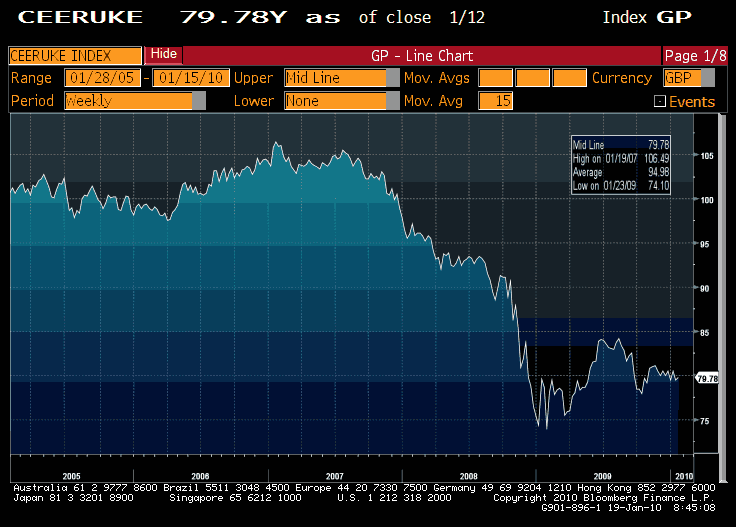

Finally, the press is also trumpeting a GS call that the UK growth will outperform that of other developed economies this year. While that may end up being the case, given the depth and duration of the UK recession (which could thereby mechanistically generate a sharp recovery), from Macro Man’s perch the rationale for UK out-performance is not particularly compelling. Macro Man struggles to see much positive impact from sterling’s protracted period of weakness; as you can see from the chart below, the TWI has been in the toilet for a good year and a half now.

(click to enlarge)

The most notable impact that Macro Man can see is that the price of certain imported goods has gone up and that the volume of supply has gone down (it’s been easier to find El Dorado that a 3 liter TDI A6 Estate.) CPI data would appear to back up that anecdotal impression; for what seems like the twelfth month in a row, inflation surprised to the upside, with even core CPI now up 2.8% y/y!

As for the trade account, it looks to Macro Man like the bulk of the improvement is past us. You can see from the chart below that the trade deficit narrowed sharply during the teeth of the crisis but has, if anything, started to widen in recent months. The reason for this is not hard to deduce; import growth has begun to exceed that of exports.

Much like the US, exports have to dramatically outperform imports on a percentage basis for the trade deficit to improve; over the last six months, imports have risen 8% while exports have risen 7%. That explains the recent widening of the trade deficit, and frankly Macro Man cannot see why it wouldn’t continue. So while Macro Man certainly expects that the UK will return to growth this year, hopes of an export-led boom would appear to wide of the mark.

So whither sterling? Macro Man has no position at the moment (other than in his p.a.), and so can view sterling through a relatively unbiased prism. And from his perspective, the most bullish outcome for the pound (fiscal retrenchment and monetary tightening) are unlikely to occur simultaneously for a long time; if anything, if one leg materializes soon, the other is likely to go the opposite way.

And so while the British pound might be doing great today, if anything the current bull could well set up a great selling opportunity sooner or later. Macro Man will be watching and waiting.

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply