When it comes to any finance-related questions, I am fair game, and those questions usually span the spectrum, from what I think about Warren Buffett (or why I don’t agree with everything he says) to whether tech stocks are in a bubble (a perennial question for worry warts). In the last few months, though, I have noticed that I have been getting more and more questions about crypto currencies, especially Bitcoin and Ether, and whether the price surges we have seen in these currencies are merited. While I have an old post on bitcoin, I have generally held back from talking about crypto currencies in this blog or in my other teaching for two reasons. First, I find that any conversation about bitcoin quickly devolves into an argument rather than a discussion, since both proponents and critics tend to hold strong views on its use (or uselessness). Second, I find that some of the technical underpinnings of bitcoin, ether and other cryptocurrencies are beyond my limited understanding of block chains and technology and I risk saying something incredibly ill informed. While both reasons still persist, I am going to throw caution to the winds and put down my thoughts about the rise, the mechanics and the future, at least as I see it, of crypto currencies in this post.

The Market Boom

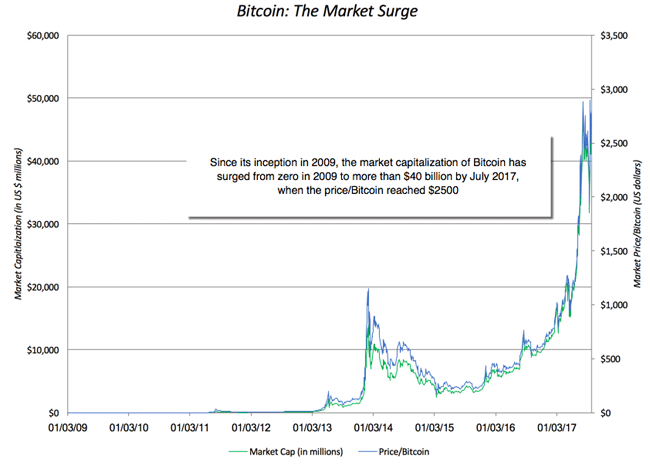

Any discussion of crypto currencies has to start with the recognition that the experiment is still young. Satoshi Nakamoto’s paper on bitcoin was made public in October 2008 and implemented as open source in January 2009. Less than ten years later, the market capitalization of bitcoin alone is in excess of $40 billion and the success story, at least in terms of bitcoin as an investment, can be seen in the graph below:

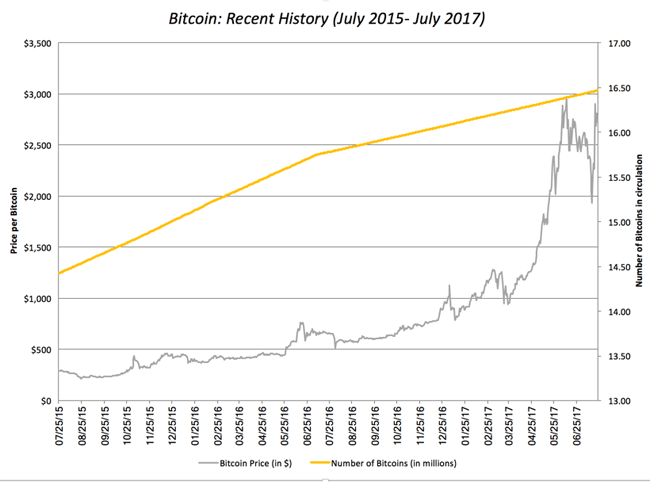

The initial rise could have been a flash in the pan, a fad attracting speculators, but in the last two years, Bitcoin seems to have found new fans, as can be seen below:

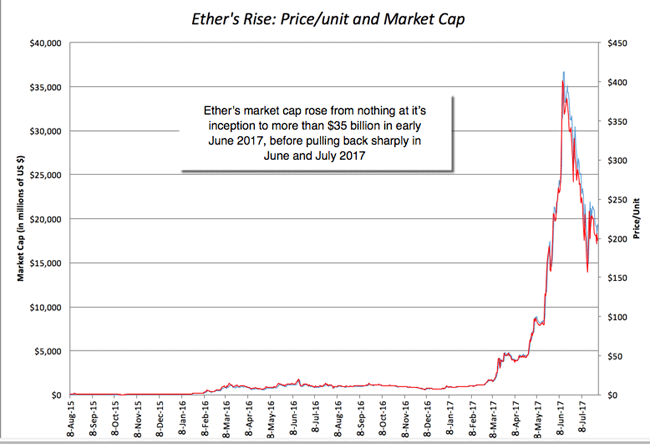

Bitcoin’s success, at least in the financial markets, has attracted a host of competitors, with Ethereum (Ether) being the most successful. Ether’s rise in market price, since its introduction in 2015 has been even more precipitous that Bitcoin’s, though it has pulled back in recent weeks:

The list of crypto currencies gets added to, by the day, with a complete list available here, with the market caps of each (in US dollars) listed. At least from a market perspective, there is no doubting the fact that crypto currencies have arrived, and enriched a lot of people along the way.

The Mechanics

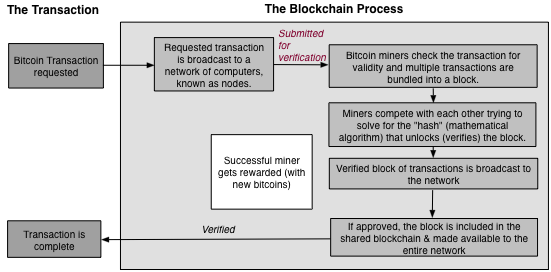

While the crypto currencies emphasize their differences, the most successful ones share a base architecture, the block chain. A block chain is a shared digital ledger of transactions in an asset where the validation of transactions is decentralized. I know that sounds mystical, but the picture below (using bitcoin to illustrate) should provide a better sense of what’s involved:

The key features of a block chain are:

- Decentralized verification: The validation and verification of a transaction is sourced to members, called miners in the crypto currency world. Verification usually involves trying different algorithms (hashes) to find the unique one that matches the transaction block, and the successful miner is rewarded, currently with the crypto currency. At least, as I understand it, this process requires more brute force (powerful processors trying different algorithms before you find a match) than intellectual firepower.

- Complete and open records: Every transaction, once validated and verified, is converted into a block of data that is recorded in the block chain ledger, which is accessible to everyone in the network. If you are worried about privacy, the transaction records do not include personal data but take the form of encrypted data (hashes).

- Incorruptible: A block chain, once recorded and shared, cannot be changed since those changes are visible to everyone in the network and are quickly tagged as fraudulent. Thus, the ledger, once created, becomes almost incorruptible.

In effect, a block chain is a digital intermediation process where transactions are checked by members of the network, and recorded, and once that is done, cannot be altered fraudulently. As you can see from its description, the block chain technology is about far more than crypto currencies. It can be used to record transactions in any asset, from securities in financial markets to physical assets like houses, and do so in a way that replaces the existing intermediaries with decentralized models. It should come as no surprise that banks and stock exchanges, which make the bulk of their money from intermediation, not only see block chains as a threat to their existence but have been early investors in the technology, hoping to co-opt it to their own needs.

The Currency Question

If you define success as a rise in market capitalization and popular interest, crypto currencies have clearly succeeded, perhaps more quickly than its original proponents ever expected it to. But the long term success of any crypto currency has to answer a different question, which is whether it is a “good” currency. Harking back to Money 101, you measure a currency’s standing by looking at how well it delivers on its three purposes:

- Unit of account: A key role for a currency is to operate as a unit of account, allowing you to value not just assets and liabilities, but also goods and services. To be effective as a unit of account, a currency has to be fungible (one unit of the currency is identical to any other unit), divisible and countable.

- Medium of exchange: Currencies exist to make transactions possible, and this is best accomplished if the currency in question is easily accessible and transportable, and is accepted by buyers and sellers as legal tender. The latter will occur only if people trust that the currency will maintain its value and if transactions costs are low.

- Store of value: To the extent that you hold some or all of your wealth in a currency, you want to feel secure about leaving it in that currency, knowing that it will not lose its buying power while stored.

Given these requirements, you can see why there are no perfect currencies and why every currency has to measured on a continuum from good to bad. Broadly speaking, currencies can take one of three forms, a physical asset (gold, silver, diamonds, shells), a fiat currency (usually taking the form of paper and coins, backed by a government) and crypto currencies. Gold’s long tenure as a currency can be attributed to its strength as a store of value, arising from its natural scarcity and durability, though it falls short of fiat currencies, in terms of convenience and acceptance, both as a unit of account and as medium of exchanges. Fiat currencies are backed by sovereign governments and consequently can vary in quality as currencies, depending upon the trust that we have in the issuing governments. Without trust, fiat currency is just paper, and there are some fiat currencies where that paper can become close to worthless. For crypto currencies, the question then becomes how well they deliver on each of the purposes. As units of account, there is no reason to doubt that they can function, since they are fungible, divisible and countable. The weakest link in crypto currencies has been their failure to make deeper inroads as mediums of exchange or as stores of value. Using Bitcoin, to illustrate, it is disappointing that so few retailers still accept it as payment for goods and services. Even the much hyped successes, such as Overstock and Microsoft accepting Bitcoin is illusory, since they do so on limited items, and only with an intermediary who converts the bitcoin into US dollars for them. I certainly would not embark on a long or short trip away from home today, with just bitcoins in my pocket, nor would I be willing to convert all of my liquid savings into bitcoin or any other crypto currency. Would you?

So, why has crypto currency not seen wider acceptance in transactions? There are a few reasons, some of which are more benign than others:

- Inertia: Fiat currencies have a had a long run, and it is not surprising that for many people, currency is physical and takes the form of government issued paper and coins. While people may use credit cards and Apple Pay, their thinking is still framed by the past, and it may take a while, especially for older consumers and retailers, to accept a digital currency. That said, the speed with which consumers have adapted to ride sharing services and taken to social media suggests that inertia cannot be the dominant reason holding back the acceptance of crypto currencies.

- Price volatility: Crypto currencies have seen and continue to see wild swings in prices, not a bad characteristic in a traded asset but definitely not a good one in a currency. A retailer or service provider who prices his or her goods and services in bitcoin will constantly have to reset the price and consumers have little certitude of how much the bitcoin in their wallers will buy a few hours from now.

- Competing crypto currencies: The crypto currency game is still young and the competing players each claim to have found the “magic bullet” for eventual acceptance. As technologies and tastes evolve, you will see a thinning of the herd, where buyers and sellers will pick winners, perhaps from the current list or maybe something new. It is possible that until this happens, transactors will hold up, for fear of backing the wrong horse in the race.

Ultimately, though, I lay some of the blame on the creators of the crypto currencies, for their failure, at least so far, on the transactions front. As I look at the design and listen to the debate about the future of crypto currencies, it seems to me that the focus on marketing crypto currencies has not been on transactors, but on traders in the currency, and it remains an unpleasant reality that what makes crypto currencies so attractive to traders (the wild swings in price, the unpredictability, the excitement) make them unacceptable to transactors.

The Disconnect

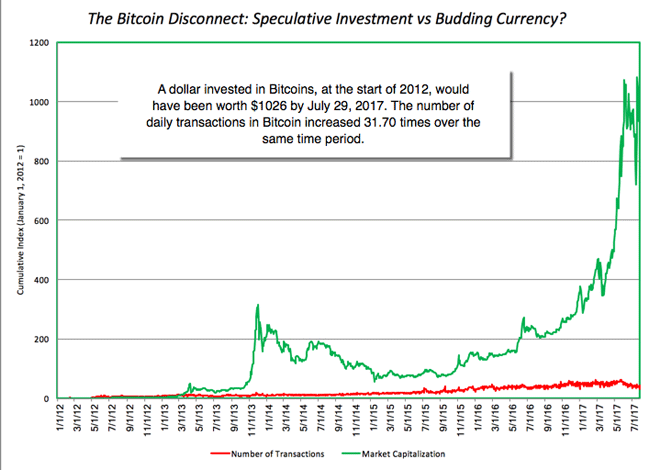

You can see the disconnect in how crypto currencies have been greeted, by contrasting the rousing reception that markets have given them with the arms length at which they have been held by merchandisers and consumers. In the graph below, I focus on the divergence between the market price rise of bitcoin and the increase in the number of transactions involving bitcoin:

While the price of bitcoin has increase more than a thousand fold, since the start of 2012, the number of transactions involving bitcoin was only about thirty two times larger in July 2017 than what it was at the start of 2012. In my view, there are three possible explanations for the divergence, and they are not mutually exclusive:

- Markets are forward looking: If you are a believer in crypto currencies, the most optimistic explanation is that markets are forward looking and that the rise in the prices of Bitcoin and Ether reflects market expectations that they will succeed as currencies, if not right away, in the near future.

- Speculative asset: I am second to none in having faith in markets, but there is a simpler and perhaps better explanation for the frenzied price movements in crypto currencies. I have long drawn a distinction between the value game (where you try to attach a value to an asset based upon fundamentals) and the pricing game, where mood and momentum drive the process. I would argue, based upon my limited observations of the crypto currency markets, that these are pure pricing games, where fundamentals have been long since forgotten. If you don’t believe me, visit one of the forums where traders in these markets converse and take note of how little talk there is about fundamentals and how much there is about trading indicators.

- Loss of trust in centralized authorities (governments & central banks): There can be no denying that the creators of Bitcoin and Ether were trying to draw as much inspiration for their design from gold, as they were from fiat currencies. Thus, you have miners in crypto currency markets who do their own version of prospecting when validating transactions and are rewarded with the currency in question. For ages, gold has held a special place in the currency continuum, often being the asset of last resort for people who have lost faith in fiat currencies, either because they don’t trust the governments backing them or because of debasement (high inflation). While gold will continue to play this role, I believe that for some people (especially younger and more technologically inclined), bitcoin and ether are playing the same role. As surveys continue to show depleting trust in centralized authorities (governments and central banks), you may see more money flow into crypto currencies.

The analogy between gold and crypto currency has one weak link. Gold has held its value through the centuries and is a physical asset. For better or worse, it is unlikely that we will decide a few years from now that gold is worthless. A crypto currency that few people use as currency ultimately will not be able to sustain itself, as shiner and newer versions of it pop up. Ironically, if traders in bitcoin and ether want their investments in the crypto currencies to hold their value, the currencies have to become less exciting and lucrative as investments, and become more accepted as currencies. Since that will not happen by accident, I would suggest that the winning crypto currency or currencies will share the following characteristics;

- Transaction, not trading, talk: From creators and proponents of the currency, you will hear less talk about how much money you would make by buying and selling the currency and more on its efficacy in transactions.

- Transaction, not trading, features: The design of the crypto currency will focus on creating features that make it attractive as a currency (for transactions), not as investments. Thus, if you are going to impose a cap (either rigid like Bitcoin or more flexible, as with other currencies), you need to explain to transactors, not traders, why the cap makes sense.

- Trust in something: I know that we live in an age where trust is a scarce resource and I argued that that the growth in crypto currencies can be attributed, at least partly, to this loss of trust. That said, to be effective as a currency, you do need to be able to trust in something and perhaps accept compromises on privacy and centralized authority (at least on some dimensions of the currency).

It is also worth noting that the real tests for crypto currencies will occur when they reach their caps (fixed or flexible). After all, bitcoin and ether miners have been willing to put in the effort to validate transactions because they are rewarded with issues of the currency, feasible now because there is slack in the currency (the current number is below the cap). As the cap becomes a binding constraint, the rewards from miners have to come from transactions costs and serious thought has to go into currency design to keep these costs low. Hand waving and claiming that technological advances will allow this happen are not enough. I know that there are many in the crypto currency world who recognize this challenge, but for the moment, their voices are being drowned out by traders in the currency and that is not a good sign.

If you expected a valuation of bitcoin or ether in this post, you are probably disappointed by it, but here is a simple metric that you could use to determine whether the prices for crypto currencies are “fair”. Currencies are priced relative to each other (exchange rates) and there is no reason why the rules that apply to fiat currencies cannot be extended to crypto currencies. A fair exchange rate between two fiat currencies will be on that equalizes their purchasing power, an old, imperfect and powerful theorem. Consequently, the question that you would need to address, if you are paying $2,775 for a bitcoin on August 1, 2017, is whether you can (or even will be able to) but $2,775 worth of goods and services with that bitcoin. If you believe that bitcoin will eventually get wide acceptance as a digital currency, you may be able to justify that price, especially because there is a hard cap on bitcoin, but if you don’t believe that bitcoin will ever acquire wide acceptance in transactions, it is time that you were honest with yourself and recognized that is just a lucrative, but dangerous, pricing game with no good ending.

Conclusion

Crypto currencies, with bitcoin and ether leading the pack, have succeeded in financial markets by attracting investors, and in the public discourse by garnering attention, but they have not succeeded (yet) as currencies. I believe that there will be one or more digital currencies competing with fiat currencies for transactions, sooner rather than later, but I am hard pressed to find a winner on the current list, right now, but that could change if the proponents and designers of one of the currencies starts thinking less about it as a speculative asset and more as a transaction medium, and acting accordingly. If that does not happen, we will have to wait for a fresh entrant and the most enduring part of this phase in markets may be the block chain and not the currencies themselves.

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply