Here is a thought experiment: what if the US economy entered a recession next month? Would it be too early for a recessions? How would it compare to previous recessions? And what stories we would tell to explain why the recession happened?

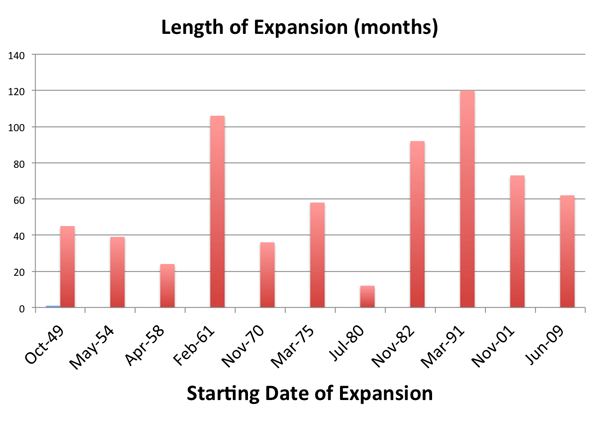

Let’s start counting months using the two phases of the business cycle as defined by the NBER business cycle dating committee. How long is the current expansion? The current expansion started in June 2009, which makes it already 62 months. Compared to all the previous post-WWII expansions it is already above average (60.5 months).

Another way to look at it is to realize that we are only one year away from reaching the length of the previous expansion (73 months). It is true that we are still far from reaching the 92 or 120 months of the previous two, but these were two of the largest expansion the US has ever seen. So for those who like to think about expansions and recessions in terms of length and they have the idea that crisis happen with a “certain” frequency, there would be nothing unusual if a recession started today.

What would be more unusual is the way the economy would look like as it entered a recession. There are no indications of the economy running out of slack (inflation, wage growth). It would also be very hard to find large financial excesses as we saw at the end of the 90s (the stock market reached price-earning ratios that are a lot higher than what we see today) or something similar to the large increase in investment in real estate in addition to highly overvalued housing prices that we saw in the years prior to the December 2007 recession. We could of course argue that the recession happened because of geopolitical uncertainty but any historical analysis of political events over the last decades would suggest that what we are seeing today (so far, keeps fingers crossed) is not that unusual.

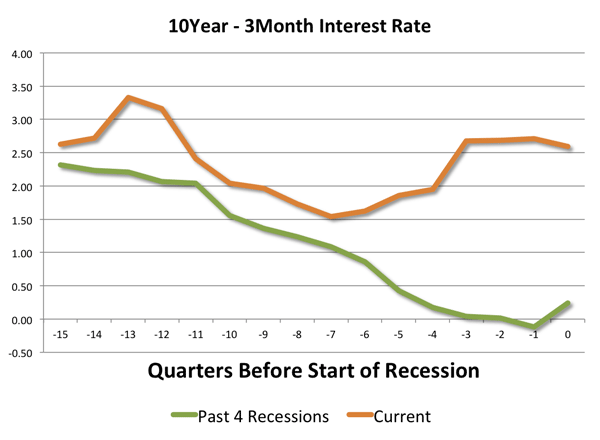

And if a recession started today, one pattern that would also be very different is the stance of monetary policy. If we measure it by the difference between long-term and short-term rates we typically see that this difference displays a strong and consistent downward trend as we approach a recession, something that we have not seen at all in recent months (or years). Here is a quick comparison of the difference between 10 year and 3 month interest rates for the average of the last four recessions compared to what the data would look like for a recession starting today.

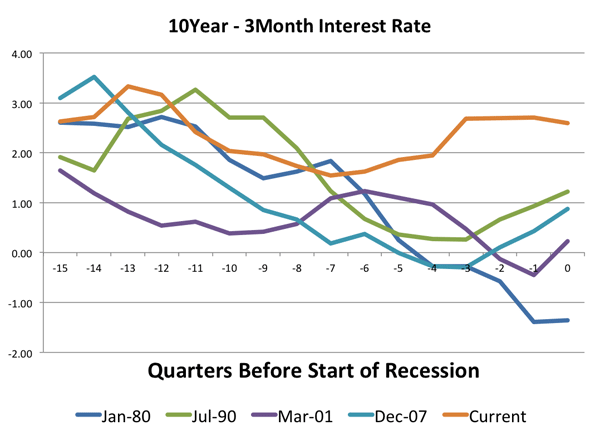

The average of the past 4 recessions shows that the interest rate difference displays a steady downward trend towards zero in the quarters that precede the recession. And if you want more details, here is the data for those 4 recessions (I am removing the July 1981 recession because the expansion before was too short to say anything meaningful).

While there are some differences across each of the cycles, they all share the same overall trend. We have not seen any of this pattern over the last quarters or years. The difference between 10 year and 3 month interest rate remains flat. And while it is possible that short term interest rates are about to start increasing in the US, it is very likely that when they do we also see increases in the 10-year rate. So if this was a typical cycle, we are far from seeing a flat or downward-slopping yield curve.

So what would a US recession today do to our understanding of business cycles? While it would not be a large surprise in terms of how soon it happened relative to the previous one, it would open many questions about the reasons why recessions happen and about the behavior of interest rates and monetary policy around the turning point of the cycle. It would be yet another “new normal”, this time for business cycles.

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply