Several US states have recently implemented laws requiring the collection of sales tax on online purchases. In practice, however, only Amazon.com has been affected. This column shows that households living in these states have reduced their Amazon expenditures by 9.5%. It also shows that the decline in Amazon purchases is offset by a 2% increase in purchases at local brick-and-mortar retailers and a 19.8% increase in purchases through the online operations of competing retailers.

Over the past decade, online retail transactions have increased dramatically in volume. Many factors have contributed to this growth in online sales, one of which is that out-of-state online retailers do not charge sales tax, which has generally given them a price advantage over retailers with a presence in the state. This sales tax collection loophole has not gone unnoticed by state governments or by competing retailers. Because the tax-advantage status of online retailers could reduce the demand for local retailers, state governments are concerned about depressed local employment and eroded income tax revenues. Many states have responded by adopting laws commonly referred to as an “Amazon Tax.” Though the laws are written generally to apply to all online retailers, Amazon is usually the only retailer to have been affected by such laws because it dominates the online retail space. Previous empirical work shows that consumers are sensitive to prices and to sales tax, especially in the online retail arena (e.g. Agarwal et al. 2013; Einav et al. 2014), yet little empirical evidence has been gathered about the effects of wide implementation of such a tax on online and brick-and-mortar retail. As more and more states begin to implement Amazon Tax laws, it is important to study their effects on the internet and local retail landscapes.

Sales tax and online shopping

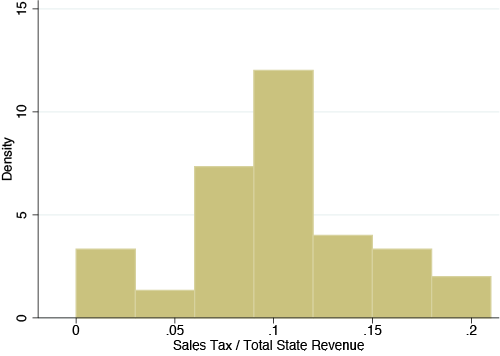

State governments have increased their attention to the issue of sales tax collection in light of the Great Recession and the recent growth in online retail volume. General sales taxes represent an important part of state revenue. For example, in 2011 the collection of general sales tax constituted 10.4% of revenues. Figure 1 shows that the importance of this tax varies considerably across states, ranging from 0% of state revenues in states without sales tax (such as Oregon and Alaska) to as high as 21% of state revenues for Washington. Recently, the issue has received federal attention. The Marketplace Fairness Act of 2013, which would enable all states to collect sales tax on purchases made from out-of-state retailers, has been approved by the Senate and is currently being debated in the House of Representatives.1 The recent recession has added fuel to the debate. Proponents of the online sales tax collection bill often tout the elimination of the internet retailer sales tax advantage as “levelling the playing field” and helping to restore business and jobs to local economies.

Figure 1. Histogram of sales tax revenue/total state revenue for the 50 states in 2011

Source: 2011 US Census Annual Survey of State & Local Government Finance

Online retailers that are not required to collect sales tax enjoy a price advantage. As a result, we hypothesise that the introduction of the Amazon Tax would lead to a decline in Amazon’s sales and substitution to alternative retailers (Baugh et al. 2014). With effective sales tax rates as high as 10% in some jurisdictions (after accounting for state, county, and city taxes), this price advantage can be sizable. Gene DeFelice, vice president of Barnes and Noble, the largest book retailer in the US, summarised the issue succinctly: “We are at a serious competitive disadvantage against out-of-state, online retailers who pay no taxes.” An additional factor that is likely to facilitate customer migration from Amazon to alternative outlets is the low search cost of online shopping.

Our work is related to studies exploring the sensitivity to sales tax in the specific context of online retail. Goolsbee (2000a, 2000b) uses survey data to estimate that the number of online shoppers would drop by 24% if the tax-advantaged status of internet retailers were removed. Alm and Melnik (2005), Ballard and Lee (2007), and Scanlan (2007) address the question as well, though they find smaller magnitudes for the effect. Goolsbee et al. (2010) ascertain that the penetration of the Internet is correlated with lower sensitivity of cigarette sales to local taxes, suggesting that smokers use the internet to purchase tax-free cigarettes. Ellison and Ellison (2009) explore the price elasticity of memory modules sold by a particular retailer and determine that consumers are price sensitive both to net prices and to state taxes. Einav et al. (2014) document a strong preference among eBay customers for out-of-state sellers, for whom sales taxes do not apply. Anderson et al. (2010) show that when retail chains open their first store in a new state, they experience a decline in their internet sales shipped to that state because of the sales tax, but the researchers find no similar effect on catalogue sales.

Measuring the sensitivity of Amazon’s sales to the Amazon Tax

In this study, we focus on five states – California, New Jersey, Pennsylvania, Texas, and Virginia – that began a permanent collection of taxes on Amazon purchases between 2012 and 2013. We analyse the impact of the tax on internet commerce as well as on brick-and-mortar retail activity. Our dataset contains high-frequency household-level transaction data for three million households, allowing us to closely examine consumers’ purchase behaviour around the introduction of the tax.

Our results show that the introduction of the Amazon Tax resulted in a large decline across all states of 9.5% in the value of products (net of sales tax) purchased on Amazon. Given that sales tax rates in the affected states vary from 5.0% (Virginia) to 8.2% (California), we calculate that the elasticity is –1.3. The magnitude of the elasticity is similar to that documented by Einav et al. (2014) of –1.7. We rule out the possibility that this result is due to an anticipation effect (i.e. buyers temporarily increase purchases just before the implementation of the tax). In fact, the magnitude of the effect increases as we increase the window around the tax implementation date, suggesting that the decrease in Amazon sales is not driven by a temporary acceleration of purchases prior to the implementation of the law.

We document that the reduction in Amazon purchases is driven by larger purchases, as consumers would garner the greatest savings by avoiding tax on such purchases. Consumers decrease their spending by 15.5% on purchases larger than $150, and by 23.8% on purchases equal to or larger than $300. These figures imply elasticities of –2.1 and –3.2, respectively.

We examine whether the decline in demand for Amazon products extends beyond average spending to the likelihood of shopping at Amazon during any particular week. We find that the likelihood of doing so in any given week declined by 0.7 percentage points, representing a relative decline of 3.7%. Similarly, we look at the frequency of purchases and find that the number of transactions per week declined by 4.2% following implementation of the tax.

Substitution to other retailers

We document that households substitute away from Amazon to competing retailers, whether brick-and-mortar or online. We show a 19.8% increase in purchases at the online operations of competing retailers. We also find a 2.0% increase in local brick-and-mortar expenditures at these retailers. When we look at large purchases, the substitution effect is more pronounced. For purchases over $300, we find a 23.7% increase in purchases at other online retailers and a 6.5% increase in purchases at local brick-and-mortar retailers. When we look at the sales of Amazon Marketplace merchants, who are generally not subject to the Amazon Tax, the large sales (≥$300) of these retailers increase by 60.5% after the tax goes into effect. We conclude that to a small degree, the tax legislation achieved its objective of restoring retail activity to local communities, though most of the gains in “levelling the playing field” are garnered by the online operations of retailers.

Conclusion

Our study shows that Amazon experiences a decline of about 10% in sales following the implementation of an Amazon Tax. The decline in sales is sharper – above 23% for large purchases (above $300). This suggests that about 10% of Amazon’s sales (and 23% of large sales) were driven by a tax advantage over its competitors.

Furthermore, the fact that households reduce their shopping with Amazon indicates that indeed households do not voluntarily pay the use tax to their states.

We document that households substitute Amazon with other retailers. About half of substitution we observe takes place with brick-and-mortar big box retailers (e.g. Walmart). The rest of observed substitution is split between online retail arms of the big box retailers (e.g. walmart.com), and Amazon Marketplace. While the online retail arms of the big box retailers collect sales tax, Amazon Marketplace does not require sales tax collection in most cases. Due to data limitations, we are not able to measure the effect of the Amazon Tax on small mom and pop stores.

Overall, our study documents that online consumers are very sensitive to total prices, and showing that the implementation of sales tax hurt Amazon and benefited local retailers.

References

•Agarwal, Sumit, Souphala, Chomsisengphet, Teck-Hua Ho, and Wenlan Qian (2013), “Cross-Border Shopping Do Consumers Respond to Taxes or Prices”, Working Paper, National University of Singapore.

•Alm, James, and Mikhail I. Melnik (2005), “Sales Taxes and the Decision to Purchase Online”, Public Finance Review 33, 184–212.

•Anderson, Eric T., Nathan M. Fong, Duncan I. Simester, and Catherine E. Tucker (2010), “How Sales Taxes Affect Customer and Firm Behavior: The Role of Search on the Internet”, Journal of Marketing Research 47, 229–239.

•Ballard, Charles, L. and Jaimin Lee (2007), “Internet Purchases, Cross-Border Shopping, and Sales Taxes”, National Tax Journal 60(4), 711–725.

•Baugh, Brian, Itzhak Ben-David and Hoonsuk Park (2014), “The ‘Amazon Tax’: Empirical Evidence from Amazon and Main Street Retailers”, Charles A. Dice Center Working Paper No. 2014-05.

•Einav, Lira, Dan Knoepfle, Jonathan Levin, and Neel Sundaresan (2014), “Sales Taxes and Internet Commerce”, American Economic Review 104(1): 1–26.

•Ellison, Glenn, and Sara Fisher Ellison (2009), “Tax Sensitivity and Home State Preferences in Internet Purchasing”, American Economic Journal: Economic Policy 1(2), 53–71.

•Goolsbee, Austan (2000a), “In a World without Borders: The Impact of Taxes on Internet Commerce”, Quarterly Journal of Economics 115(2), 561–567.

•Goolsbee, Austan (2000b), “Internet Commerce, Tax Sensitivity, and the Generation Gap”, Tax Policy and the Economy 14, 45–65.

•Goolsbee, Austan, Michael F. Lovenheim, and Joel Slemrod (2010), “Playing with Fire: Cigarettes,Taxes, and Competition from the Internet”, American Economic Journal: Economic Policy 2(1), 131–154.

154.

•Scalan, Mark A. (2007), “Tax Sensitivity in Electronic Commerce”, Fiscal Studies 28(4), 417–436.

1 The text and status of the bill are found here.