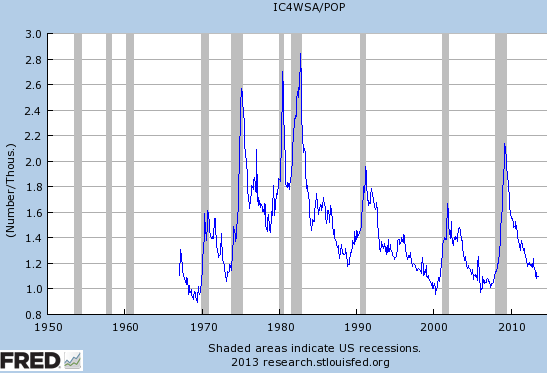

The new claims for unemployment this week was a shockingly low 320,000, bringing the 4 week average down to 335,000, which is the lowest since October 2007. This graph shows the ratio of the 4 weeks average to US population (times 1000 to make it easier to read.)

The most recent week on the graph is at about 1.1, but today’s figures are at 1.058, if they were added. This means the ratio of new claims to pop is roughly back to the boom levels of 1999-2000 and 2006-07. And yet the other indicators (total jobs, unemployment rate, etc), remain deeply depressed. I can think of two ways to interpret this data:

- Casey Mulligan is right, we have lots of structural issues that are causing high unemployment right now. The job market’s not that bad, it’s just that lots of people don’t want to work at the wages being offered, or are frozen out by the 40% rise in minimum wages during the housing bust.

- AD is still the main problem, but since 1975 there’s been a long term downward trend in the claims/pop ratio, for some mysterious reason. That trend would explain why (according to new claims) the labor market looked as good in 2006 as 2000, even though most people think it was not.

In the past I’ve argued that the minimum wage and extended UI benefits probably raised the natural rate by 0.5% to 1.0% at most. I’m sticking with that for now, although I do believe today’s data makes the structural hypothesis a tad more likely. What would it take for me to change my mind? If wage growth stays around 2% (or more) and NGDP growth stays around 4% (or more) and the unemployment rate stops falling for a couple years. Then I’d agree Mulligan is right about the current labor market. Of course unemployment has already fallen from 10% to 7.4%, so it’s almost certain we’ve have above natural rate unemployment over the past few years. And I still believe it will fall further.

Of course there are lots of other puzzles, like the low labor force participation rate.

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply