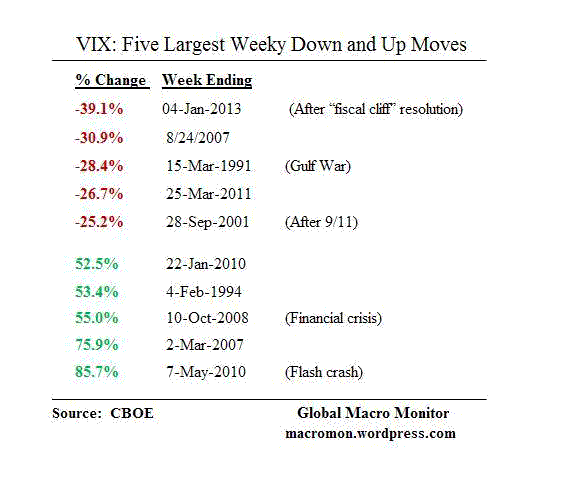

The CBOE has a nice piece out noting this week’s VIX collapse of 39.1 percent was the largest weekly percent down move since the index was launched in January 1990. The week also saw record volume days for the VIX futures.

The move even exceeds the largest weekly down move on the VXO, the vol index on the S&P 100, which was the market standard volatility measure prior to January 1990. The VXO fell 37.9 percent the following week of the of the October 1987 stock market crash.

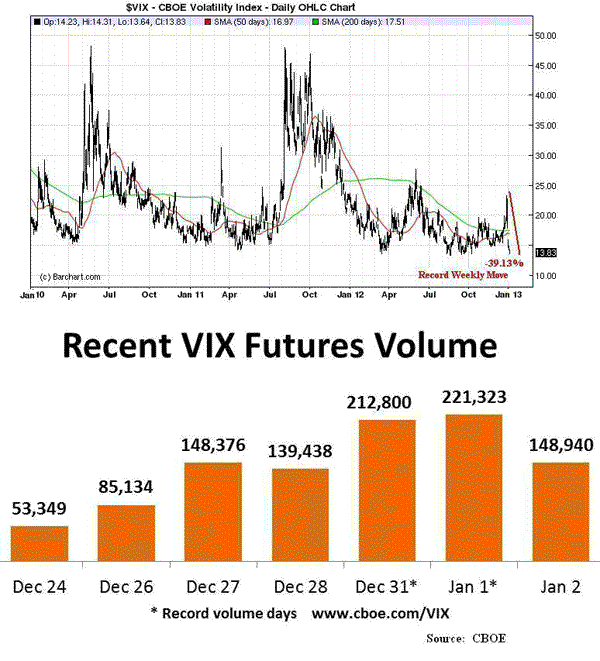

Since the March ’09 stock market bottom the VIX has only closed lower twice, on August 13 and 17, 2012. Note the July VIX futures contract closed the week at 21.40, 53 percent above the cash index.

The upshot?

Nassim Nicholas Taleb is probably less comfortable. It’s also difficult to extract much info from this move relative to the others given the rise of high frequency trading and short-term trader dominance of the markets. Furthermore, the move was likely exaggerated by the fact it happened during a major holiday shortened week with many of the big players still out and yet to begin their year.

Nevertheless, some believe stocks will only return 5 percent this year and given the huge move last week the gains for the year have already been had. We don’t know with certainty but our priors are this year could be bubblicious and the central banks will see to it until they can’t.

This could be the tipping point year where markets revolt against deficits and hyper lose monetary policy, or maybe not. For now, the markets enjoy the crack, the trend in equities is positive, and new highs are at hand.

Given this week’s huge move, coupled with the fact earnings season really gets going next week, it’s probably not a good entry here, however.

We thought that about dollar/yen at 85, however, but it keeps repricing like an emerging market currency with high inflation. Granted it was hugely oversold, but 12 percent since November 9th? Tokyo is not Buenos Aires, Toto! At least, not yet.

We always worry when central banks print money to monetize deficits and fear that money demand could collapse as holders begin to lose confidence in its future purchasing power. We seen this happen, first hand, in many countries.

Stocks will move higher and the currency lower as this begins. Though gold has been trading poorly and may have more downside on a technical basis, it should also begin to move as the printing presses begin to fire up. Asset picking becomes more complicated when most of the hard (well not so hard) currency central banks are expanding their balance sheets on such a massive scale. This is nitro when credit begins to expand.

Though they lengthened the duration of their portfolio with Operation Twist, the Fed’s balance sheet has been stable since the end of QE2. So this year should be interesting if Chairman Bernanke follows through with the announced trillion dollar asset purchase. Add that to the expected monetization the yen and Nikkei are pricing from the Bank of Japan and the potential for OMTs from the ECB with, say, a Spanish or Italian intervention, which will surely not be completely sterilized.

Furthermore, credit markets are starting to heal and the monetary aggregates are growing at annual rate well in excess of nominal GDP growth. That’s, more yield/return chasing liquidity. Could be wrong, but think we’re in for some Fireworks!

- Bulenox: Get 45% to 91% OFF ... Use Discount Code: UNO

- Risk Our Money Not Yours | Get 50% to 90% OFF ... Use Discount Code: MMBVBKSM

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply