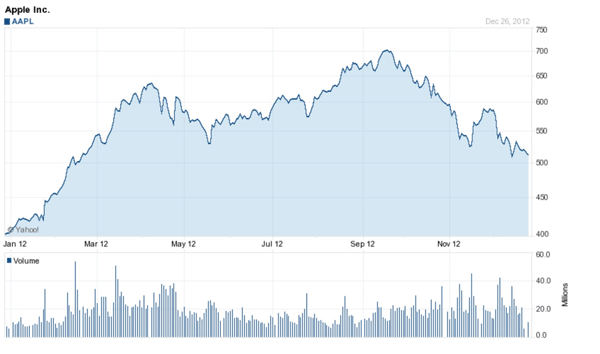

As the year winds to a close, I don’t think that there can be much debate that this was Apple’s year, for better or for worse. In my view, no company has dominated the financial news and the cultural landscape in any year as much as Apple (AAPL) did during 2012. Not only were Apple’s earnings announcements greeted with mass hysteria, but Apple’s products were bigger news than any celebrity on Hollywood. At the risk of adding to the heated discussion that accompanies almost any mention of the company, here is my attempt to pull together what happened to the company this year.

January 2012: How much cash is too much cash?

The year began with a great deal of breast beating, at least among some of the pundits & portfolio managers about how big Apple’s cash balance was, as well as ill conceived arguments about why the cash was hurting Apple’s stockholders. In my post on Apple’s cash balance on January 19, 2012, I took on the argument that cash is a bad investment simply because it earns a low rate of return, and presented my thesis that a large cash balance can have a positive, neutral or a negative effect on assessed value, with the judgment depending upon how much you trust the management of the company holding the cash. With Apple’s impeccable track record on both internal investments and stock price performance over the last decade, I argued that as an investor, I was comfortable with the company holding my cash for me and that the market was not punishing Apple for accumulating cash. In a later post on trapped cash in August 2012, I took note of the fact that a significant portion of Apple’s cash was trapped in foreign markets and that returning the cash to the US would generate a significant tax bill.

March 2012: Dividends or Buybacks?

By March 2012, Apple’s cash balance was approaching $100 billion, creating a second round of debate about whether it should return the cash to its stockholders. Rather than leave well enough alone, Apple opened the door to much greater pressure to do something with the cash, when Tim Cook, its CEO, conceded that Apple had more “cash than we need to run the company”. Once that admission was made, I argued in a post on March 1, 2012, that Apple had no choice but to take action and return cash to its stockholders. Looking at the choice between paying dividends and buying back stock, I argued that there were four considerations that came into play in making this decision: (1) whether urgent action was necessitated by the presence of acquirers or activist investors, (2) whether stockholders in the company were more motivated by dividends or capital gains in buying the stock, (3) what the tax consequences to investors were from receiving dividends/capital gains and (4) whether the stock was under or over valued. By my assessment, Apple’s market cap made it invulnerable to outside pressure, its existing stockholders had generated all their returns from price appreciation and the stock was under valued (my value per share was approximately $ 710). I argued for a stock buyback of roughly $60- $ 70 billion, with a cap set on the buyback price.

April 2012: The Clash of Investor Clientele

Apple did make a decision to return cash to its stockholders, but far less than I had argued for ($20 billion, rather than $60 billion) with half as a regular cash dividend. In a post on April 3, 2012, I explained a personal decision that I had made to sell Apple and laid out my reasons, though they were still misunderstood. After explaining how much I loved the company and how grateful I was for the returns that the stock had made for me from my original investment in 1997, I also was categorical that at $600+ a share, I felt that the stock was still a good value (based upon my assessment of value at $710/share). However, there were two forces at play in my decision to abandon the stock. First, the stock’s incredible ascent over the previous decade had made it a large portion of my personal portfolio, making my wealth vulnerable to swings in the stock. Second, the decision to pay dividends, in my view, opened the door to a new group of “dividend” stockholders investing in the stock, with very different expectations of what the company should do in the future than the “growth seeking” stockholders who already held the stock. If you added the “momentum” investors who had joined in the mix, drawn by the large market cap and price surge in the stock, you had an investor base that was at war with itself. Every news story and corporate action, I felt, would be scrutinized and found wanting by one or more of these groups, which, in turn, would lead to wild price swings that I could not afford in my portfolio.

That post exposed me to a fair amount of backlash (including anonymous voice mails on my office phone) and the critique that I was being emotional and not staying true to my intrinsic value roots. While I have a thick skin, I did feel the urge to follow up with a post on April 6, 2012, where I pleaded guilty to both charges, by admitting that my original investment in Apple in 1997 was an emotional one (I felt sorry for the company) and arguing that being right on intrinsic value was only half of winning the investment game. In fact, this tension between intrinsic value and price became a theme that I returned to repeatedly, during the rest of the year.

August 2012: The iPhone Launch

In late August, the world was agog (and I am not using hyperbole) with the coming of the iPhone 5. As I listened to my youngest (thirteen) tell me about every new rumored feature that the phone was going to have, I did my part by valuing the iPhone franchise in a post on August 29, 2012, based on five value drivers: (a) an after-tax operating margin of 21% on the product, (b) a 6% growth rate in the smartphone market, (c) a product life cycle of 2 years, (d) only 5% of iPhone users would switch to competitors, whereas 10% of competitors would switch to the iPhone and (e) a risk level commensurate with the top decile of US stocks. The resulting value for the franchise that I obtained was $ 307 billion.

The iPhone franchise valuation did point to a danger that Apple investors need to be aware of. Since half or more of Apple’s value comes from the iPhone, the short life cycle for the product will inevitably create an ebb and a flow to the stock, with each new version of the product being scrutinized for signs of slippage, just as the iPhone 5 has.

October 2012: The Maps fiasco

The iPhone did launch and while it was the most successful smartphone launch in history, what happened in the weeks following provides an illustration of the power of expectations. The assumption that Apple could do no wrong had become such an entrenched part of investor beliefs that every misstep on the iPhone put under the microscope. In a post on October 9, 2012, on expectations, I noted the contrast in market reactions to Research in Motion reporting that revenues dropped by 31% (its stock price jumped 18%) and to Apple’s mishandled free Map app (which was associated with a drop in Apple’s market cap of $40 billion).

While the expectations game has worked against Apple for the last few months of 2012, the perceived disappointments in Apple’s financial and operating results may carry a silver lining, insofar as they lead to lower expectations for the future. So, I would not be surprised if Apple’s first quarter earnings beats expectations and the game goes on…

December 2012: Blame the fiscal cliff?

As the end of the year approached, Apple seemed to go into a tail spin, starting with a disappointing earnings report in November but with the price drop accelerating as the year end approached.

Not surprisingly, analysts and pundits were looking for something or someone to blame and the fiscal cliff became a favored target. Apple’s stock price was collapsing, they argued, because capital gains taxes would increase in January 2013 and investors in Apple were therefore booking their capital gains in 2012. While I have argued that stock prices would be negatively affected if we go off the fiscal cliff, I don’t see it as the primary factor behind Apple’s fall. While the initiation of dividends in March 2012 has increased the exposure of Apple’s investors to the tax law changes coming in January 2013, large dividend paying companies such as Coca Cola and P&G should have seen much worse carnage than Apple did, if the fiscal cliff is to blame.

Looking forward to 2013

So, what now? As Apple’s stock price tests the $500 level, is it now a buy? Is the new year likely to bring changes to the company? I don’t claim to be a pundit or a financial advisor, but here are some suggestions I would have for anyone thinking about investing in Apple now or in the near future:

- Absolute versus Percent: When a company has a market capitalization of $500 billion and its stock price is $500, small percentage changes in the stock will translate into large absolute values. While that is stating the obvious, there is a psychological component that any investor in Apple has to deal with. A $25 drop in Apple’s stock price will feel like a bigger drop than a $1.50 drop in Facebook’s price, though both amount to roughly 5% of their respective prices. Put differently, Apple will feel more risky or volatile than it truly is, simply because investors are unused to $500 shares.

- Momentum shifts will continue to be the name of the game: Notwithstanding the ‘psychological’ effect of higher absolute price changes, the sudden shifts in momentum that we saw with Apple stock through 2012 will continue into 2013, as the different investor groups fight over the future direction of the company. Eventually, one or more of these disparate groups will abandon the company and move on to better targets, but that will not happen overnight. If you are an investor in Apple, be clear about what you see in the company and which group you attach yourself to.

- Don’t get distracted by small details: I subscribed to a news site that aggregates opinion pieces about Apple as an investment and I was flabbergasted at how many of these pieces were based upon non-news. The process hit a climax, for me, when a unsourced blog post/news story/tweet that there was only one person outside the Apple Shanghai store when the iPhone 5 was introduced there caused the stock to lose $15 billion in market value. Much of what you will read about Apple (the size of the iPad mini screen, whether the Google maps app is better than the Apple Maps app, when the next iPhone is coming out) matters little in the big picture.

- Focus on Apple’s value and its value drivers: The drivers of Apple’s value are not difficult to decipher and I have attempted to make them transparent in my updated valuation of Apple. If you download the spreadsheet, you will note that my estimate of the value per share has dropped to $609 per share (from my March 2012 estimate of $710/share). While my revenue and margin numbers (the growth rate in revenues is lower, but the dollar revenues over time are similar) in the new valuation are very close to my March 2012 estimates, I have reassessed the cost of capital to reflect Apple’s increasing dependence on Asia for future growth: that growth will come with higher risk (which shows up as a higher risk premium). I have also been conservative in assuming that the trapped cash will be subject to an immediate tax penalty of about $18.4 billion (when, in fact, it will be paid over a long period of time or perhaps not at all). If you are investing in Apple stock, you should make your own assessment of the company rather than trust mine (or anyone else’s).

- Ignore the experts/analysts: During the last year, equity research analysts collectively have never been ahead of the curve on Apple’s share price. Every increase in the stock price seems to lead analysts to increase their estimated value for the stock and every drop precipitates a drop in assessed values. So, ignore the buy, the sell and the hold recommendations from analysts, since they are agents of momentum rather than oracles of change.

Bottom line: At $500/share, in my view, Apple is under valued and I believe that my assessment of value is a sober one, with little built in value added from future game changers. Apple reinvented the personal music player business (with the iPod), inspired the smart phone business (with the iPhone), created the tablet business (with the iPad), reconfigured the entertainment retail business (with iTunes and the Apple stores) and there is no reason why it cannot change other businesses and generate additional value for its investors. I am still nervous about my fellow travelers in this stock and how they may cause the price to deviate from value, but I am more sanguine than I was in April for two reasons. First, many of these investors are fickle and I would not be surprised to see the same momentum investors, who jumped on the bandwagon when the stock was going up, abandon it now. Second, l can live with the price noise if Apple were a smaller portion of my portfolio and I can make that choice. So, I have a buy limit order for Apple at $500 and I may or may not be an Apple stockholder this new year, depending on what the stock does in the next two days. I am okay either way!

- Bulenox: Get 45% to 91% OFF ... Use Discount Code: UNO

- Risk Our Money Not Yours | Get 50% to 90% OFF ... Use Discount Code: MMBVBKSM

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply