Goldman Sachs is joining the Research in Motion (NASDAQ:RIMM) bulls this morning with an upgrade to Buy from Neutral with a $16 price target (prev. $9)

– Their Bull case is $31/share based non FY14 EPS of $3.08

Some context on the recent run – RIMM is up 76% from its September low of $6.31, but still down 23% on the year and down 92% from its 2008 high. The recent run has been driven by better–than-expected August quarter earnings, followed by the announcement that BB10 would launch on January 30 and is in the labs of 50 carriers for final testing, as well as a steady drumbeat of emerging bits of information around the new smartphones’ specs and features (which have been generally impressive). Given that short interest in the stock is at an all-time high at 20% of shares outstanding, Goldman believes short covering has contributed to the sharp bounce off the lows.

Goldman notes they are upgrading the stock as they see a positive risk/reward heading into its BlackBerry 10 (BB10) launch on January 30. For the first time in 3 years, they think out-year Street estimates are too low, as they don’t capture: 1) the ASP lift from BB10; 2) the associated margin improvement; and 3) the channel inventory fill for BB10. They now assess a 30% chance of success for BB10 given positive early reviews, broad-based carrier support, attractive features, and interest by carriers and consumers in broadening the field beyond Android/iOS;

(click to enlarge)

Catalyst

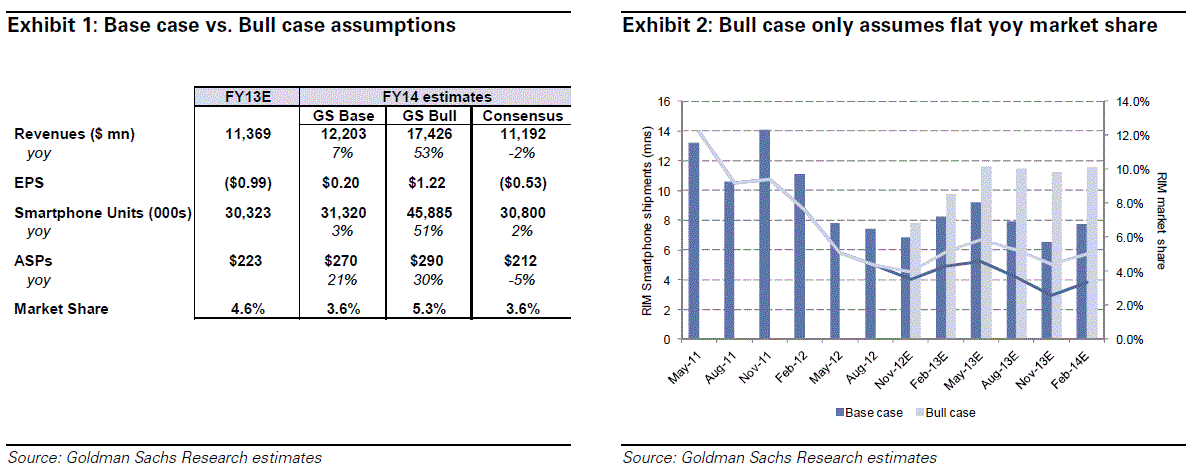

Goldman expects RIM’s results will exceed Street estimates over the next 4 quarters, with their revenue estimates 8% and their quarterly EPS $0.14 above consensus on average. In fact, the firm now estimates that RIM will turn profitable in FY14 (Feb) vs. the consensus view of continued losses. The primary source of upside is their FY14 smartphone ASP estimate of $270, up 21% yoy vs. the consensus view of roughly flat, as they expect BB10 devices priced at over $400 will drive more than a third of the total volume, offsetting sharp declines in emerging markets where ASPs are much lower. Goldman is raising their FY13/14/15 EPS estimates to ($0.99)/$0.20/($0.62) from ($1.07)/($0.52)/($1.61) on higher ASPs and margins as a result of the BB10 ramp, partially offset by much lower units in emerging markets.

A trade or an investment? Time will tell – Even if BB10 is ultimately not successful (which is Goldman\s current base case scenario, at 70% probability) they expect RIMM to outperform over the next 2-4 quarters, as they see upside to Street estimates from higher ASPs and margins as well as channel inventory fill over the next 4 quarters around the BB10 launch. If RIMM does succeed in establishing BB10 as a viable niche ecosystem and sees follow-through demand post the launch (which is Goldman bull case scenario, at 30% probability), then it could further strengthen the long-term investment case.

Notablecalls: The stock took a slight breather following the 2 upgrades (Jeffco and CIBC) that took it from $9.50 to $12 recently.

Now it can proceed higher. I’m thinking $12.50+ today.

- Bulenox: Get 45% to 91% OFF ... Use Discount Code: UNO

- Risk Our Money Not Yours | Get 50% to 90% OFF ... Use Discount Code: MMBVBKSM

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply