To the titular question, Steve Williamson thinks the answer is “yes“:

… the behavior of the FOMC has changed. Either it cares about some things it did not care about before (and in a particular way), or it cares about the same things in different ways—in particular it is less concerned about its price stability mandate.

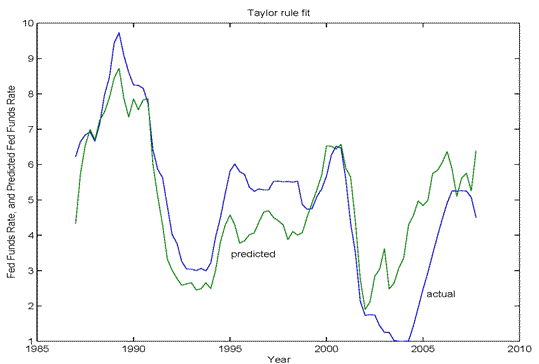

Part of the Williamson case relies on an earlier post, where Williamson illustrates deviations of the actual path of the federal funds rate paths from his own estimated version of the Taylor rule:

New Keynesians like to think about monetary policy in terms of a Taylor rule, which specifies a target for the federal funds rate as a function of the “output gap” and the deviation of the actual inflation rate from its target value. According to standard Taylor rules, the fed funds target should go down when the output gap rises and up when the inflation rate rises. You can even fit Taylor rules to the data. I fit one to quarterly data for 1987-2007, and obtained the following:

R = 2.02 – 1.48(U-U*) + 1.17P,

where R is the fed funds rate, U is the unemployment rate, U* is the CBO natural rate of unemployment (so U-U* is my measure of the output gap) and P is the year-over-year percentage increase in the PCE deflator. You can see how it fits the historical data in the next chart.

So that’s how the Fed behaved in the past. If it were behaving in the same way today, what would it be doing? Given that U = 7.8, U* = 6.0, and P = 1.5, my Taylor rule predicts R = 1.1%….

So, the Fed’s behavior seems to have changed.

An obvious point: It is clear from Williamson’s chart above that the predictive power of his version of the Taylor rule is far from perfect. In fact, through 2007 the standard deviation of the estimated rule’s prediction error is 1.3 percentage points. From that perspective, the difference between a Williamson-Taylor rule funds-rate prediction of 1.1 percent and the actual current value of 0.14 percent doesn’t seem so dramatic. I don’t really see an obvious deviation from previous behavior.

More to the point, unless the metric is an absolutely slavish devotion to a particular form of the Taylor rule, I’m not exactly sure what evidence supports a conclusion that the Federal Open Market Committee (FOMC) is now “less concerned about its price stability mandate.” As I argued a few weeks back, I think it is not too much of a stretch to construct a justification of post-crisis Fed actions up to the September decision entirely in terms of support for the FOMC’s price stability mandate.

I don’t take any great exception to Williamson’s claim that, with respect to the FOMC’s stated inflation objective, things look pretty much on target:

If we look at a longer horizon, as I did here, from the beginning of 2007 or the beginning of 2009, you’ll get something a little higher than 2.0% (I didn’t have the most recent observation in the chart in the previous post). Too low? I don’t think so.

Furthermore, in my previous post I noted that while there is a plausible case that previous asset purchase programs were required to maintain this salutary record on the inflation front, the case is arguably less plausible for “QE3.” But, to my mind, that just isn’t enough evidence to conclude that the FOMC has downgraded its price stability goals.

Consider a homeowner with the dual mandate of keeping both the roof of the house and the driveway in good repair. If the roof isn’t leaking but there are cracks in the driveway, I think you would expect to see the owner out on the weekend patching the concrete. I don’t think you would conclude as a result that he or she had ceased caring as much about the condition of the roof. I do think you would conclude that attention is being focused where the problem exists.

I suppose the argument is that the Fed is raining so much liquidity down on the world that the roof is, sooner or later, bound to leak. The FOMC has expressed confidence that, if this happens, it has the tools to patch things up and will deploy those tools as aggressively as required to meet its mandate. I guess Steve Williamson feels differently. But that, then, is a difference of opinion about things to come, not about the facts on the ground.

Leave a Reply