Dean Baker, responding to this Wall Street Journal article, sees an opportunity to make us aware on the distributional impacts of monetary choices. Specifically, Baker responds to the claim that inflation erodes earnings:

Actually, most wages follow in step with inflation, although some workers do see declines in real wages when inflation rises.

People seem to forget the connection between inflation and wages. A sustained increase in inflation needs to be accompanied by a matching increase in wages, otherwise higher inflation would simply undermine real purchasing power, leading to slower growth and a subsequent decline in the inflation rate. To be sure, as Baker notes, while on average higher inflation is matched with higher nominal wages, it does not affect all workers equally – workers with less bargaining power could see their real wages decline even if average real wages hold constant.

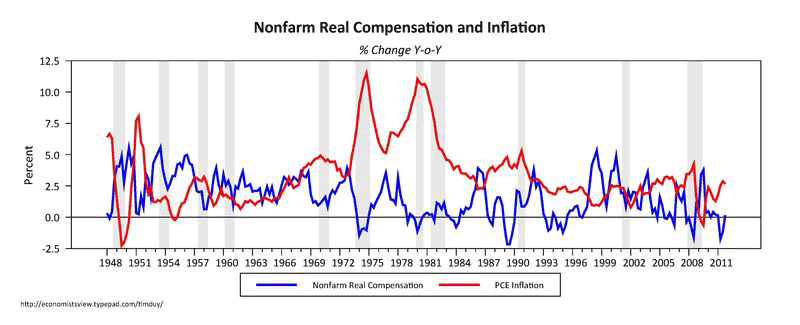

Baker identifies this basic chart (I replaced CPI with PCE inflation) to support his argument :

(click to enlarge)

Notice that Baker correctly shifts from real wages to the broader measure of real compensation. He says:

These series give the basic story, although they are not perfect for reasons that you do not want to hear about. If you can see a negative relationship (i.e. higher inflation leads to lower real wage growth) you have better eyesight than me.

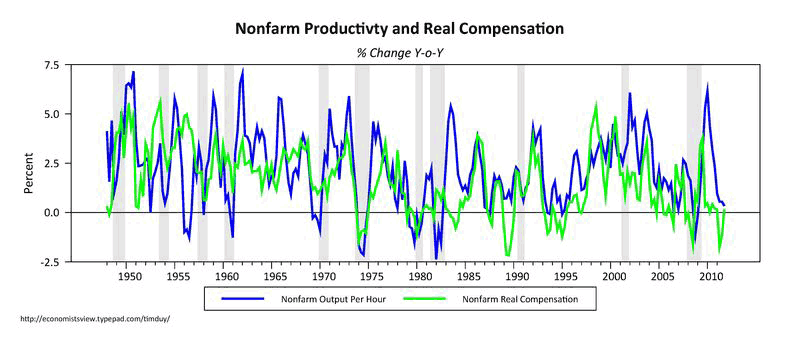

In fact, the correlation between these two series is 0.36. In other words, there is a weak positive relationship between inflation and real compensation – although I would be wary about calling it a causal relationship, and instead only point out that although it is often claimed that inflation erodes real wages, this is not obvious. What is more evident, and causally related, is the link between productivity and real compensation:

(click to enlarge)

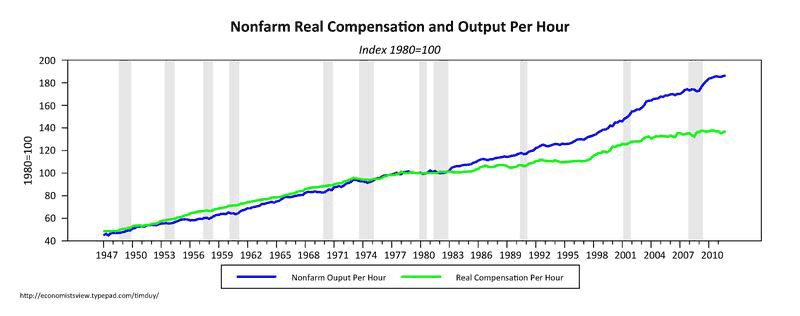

The correlation is 0.75, and the story is a familiar one – we expect that higher productivity growth results in higher real wage growth. That said, a careful eye will notice that the growth rates are not identical, yielding this well-known result:

(click to enlarge)

Certainly since the 1980s, the gap between output and real compensation is rising. Another version of this issue is that labor’s share of income has been falling since 1980. What is of course curious is that this occurs despite the sustained period of disinflation. Those who claim that inflation erodes real wage growth seem to miss that the period since 1980 has seen real compensation growth slow to a pace below productivity growth despite falling inflation. This issue is taken up by Steve Randy Waldman at interfluidity with a thought provoking post:

An increase in unit labor costs can mean one of two things. It can reflect an increase in the price level — inflation — or it can reflect an increase in labor’s share of output. The Federal Reserve is properly in the business of restraining the price level. It has no business whatsoever tilting the scales in the division of income between labor and capital.

Yet throughout the Great Moderation, increases in unit labor costs were the standard alarm bell cited by Fed policy makers as an event that would call for more restrictive policy. And all through the Great Moderation, except for a brief surge during the tech boom, labor’s share of output was in secular decline…

…even if the Fed didn’t “cause” the decline in labor’s share, Great Moderation monetary policy made it very difficult for labor’s share to grow…

…Since the early 1990s, all actors in the US political system have understood that policies that increase unit labor costs risk a response by the “inflation fighting” central bank, whose “credibility” was swaggeringly defined as a willingness to provoke recession rather than risk inflation. In this environment, the decline of labor unions and their shift in focus from wage growth to working conditions was understandable…

Waldman is saying that the Federal Reserve is at least complicit in allowing the competition between capital and labor to be tilted toward capital (not sure this should be a surprise – I don’t see a revolving door between the Federal Reserve and the AFL-CIO). In other words, monetary policy has a direct impact on the distribution of income. It’s not just simply raising and lowering interest rates to affect the level of output – it has an impact on how the subsequent output is split up. Waldman offers some policy advice:

All of this is one more reason to prefer the NGDP path target promoted by Scott Sumner and his merry Market Monetarists. It might prove difficult in practice to target inflation without paying some especial attention to wage growth. But a central bank can target the path of aggregate expenditure without playing favorites about who pays what to whom. Simple neutrality by the central bank in the contest between capital and labor would be a huge improvement over the status quo.

Note that even if the central bank is no longer playing “favorites”, monetary policy would still have a distributional impact. For example, reverting to the pre-recession path of nominal spending would likely entail a temporarily higher rate of inflation than currently expected. And higher than expected inflation will indeed create some winners and losers:

However, the biggest losers are creditors who are almost by definition wealthy, since people owe them money. If a creditor has lent out $100 million at 2 percent interest (e.g. buying a 10-year U.S. or German government bond) and the inflation rate rises from 2 percent to 4 percent, this creditor has lost an amount equal to 100 percent of his expected income or 2 percent of his wealth. This is a far larger loss than any worker could experience as a result of this increase in the inflation rate.

Who would be the winners?

Also, most workers are debtors to some extent. They are likely to have mortgage debt, credit care debt, student loan debt and or car debt. A higher rate of inflation means that they can repay this debt in money that is worth less than the money they borrowed.

And once again, we get to the same place – changing monetary policy at this juncture would likely have significant impacts on the distribution of income and wealth. And an unwillingness to alter this current distribution is likely another reason we would not expect the Federal Reserve to change their basic policy framework away from the current 2 percent inflation target regime.

- Bulenox: Get 45% to 91% OFF ... Use Discount Code: UNO

- Risk Our Money Not Yours | Get 50% to 90% OFF ... Use Discount Code: MMBVBKSM

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply