From the Forbes article by Louis Woodhill “Gasoline Prices Are Not Rising, the Dollar Is Falling“:

“As this is written (2/22/2012), West Texas Intermediate crude oil (WTI) is trading at $105.88/bbl. All this means is that the market value of a barrel of WTI is 105.88 times the market value of “the dollar.” It is also true that WTI is trading at €79.95/bbl, ¥8,439.69/bbl., and £67.13/bbl. In all of these cases, the market value of WTI is the same. What is different in each case is the value of the monetary unit (euros, yen, and British pounds) being used to calculate the ratio that expresses the price.

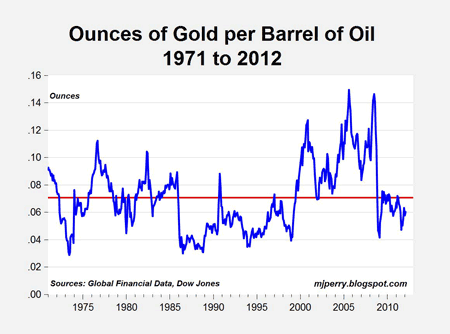

In terms of judging whether the price of WTI is high or low, here is the price that truly matters: 0.0602 ounces of gold per barrel (which can be written as Au0.0602/bbl). What this number means is that, right now, a barrel of WTI has the same market value as 0.0602 ounces of gold.

During the 493 months since January 1, 1971, the price of WTI has averaged Au0.0732/bbl. It has been higher than that during 225 of those months and lower than that during 268 of those months. Plotted as a graph, the line representing the price of a barrel of oil in terms of gold has crossed the horizontal line representing the long-term average price (Au0.0732/bbl) 29 times.

At Au0.0602/bbl, today’s WTI price is only 82% of its average over the past 41+ years. Assuming that gold prices remained at today’s $1,759.30/oz, WTI prices would have to rise by about 22%, to $128.86/bbl, in order to reach their long-term average in terms of gold. As mentioned earlier, such an increase would drive up retail gasoline prices by somewhere between $0.65 and $0.75 per gallon.

At this point, we can be certain that, unless gold prices come down, gasoline prices are going to go up—by a lot. And, because the dollar is currently a floating, undefined, fiat currency, there is no inherent limit to how far the price of gold in dollars can rise, and therefore no ultimate ceiling on gasoline prices.”

MP: Measured in terms of a stable commodity in relatively fixed supply like gold, the price of oil now is below its historical average, as the chart illustrates, and suggests that the falling value of the U.S. dollar is contributing to record high gas and oil prices, when measured in dollars. Measured in gold, oil and gas are now historically “cheap,” not expensive.

Leave a Reply