It wasn’t a pretty week for gold prices. The eurozone’s epic endeavor to conquer its sovereign debt issues forced some institutional investors to liquidate profitable gold positions to meet a rising need for liquidity.

In addition, falling confidence in the euro and other global currencies pushed investors tumbling toward the relative safety of the U.S. dollar. As we outlined for you last week, the key phrase is “relative safety” because we know that it could only take a slight breeze to blow the dollar’s house down.

Back on August 22, I wrote that gold was due for a correction and that it would be a non-event to see a 10 percent drop in gold. I wrote, “This would actually be a healthy development for markets by shaking out the short-term speculators.”

This morning’s gold price of $1,590 is about 15 percent from the high, which is a little greater than predicted, but a non-event just the same. I believe the long-term story remains on solid ground.

In a report this week, Credit Suisse reiterated the bull market for gold is not over, saying, “We do not believe the key fundamental drivers of the [gold] bull market have dissipated. While there are risks, in our opinion gold is getting close to attractive levels for new longs to be initiated.”

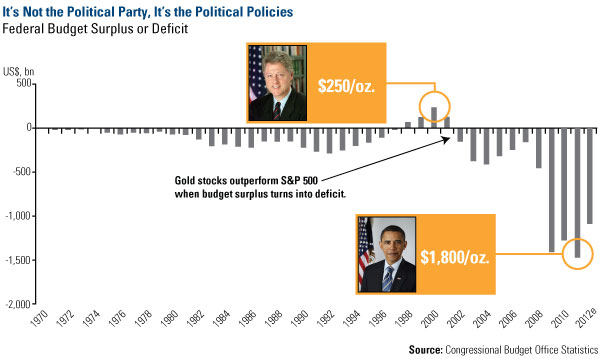

Gold Stocks vs. the Federal Budget

This chart, which we’ve highlighted several times, shows the size of the surplus or deficit in the federal budget. When the federal government is spending more than it takes in, gold and gold stocks tend to outperform the broader market. It’s important to point out that it’s the political policies, not political parties, that drive this phenomenon. During the 1990s, when President Clinton was in office, there was a budget surplus and investors could earn more on Treasury bills (about 3 percent) than the inflationary rate (about 2 percent). This gave investors little incentive to embrace commodities such as gold, and prices hovered around $250 an ounce.

Since 2001, increased regulation in all aspects of life, negative real interest rates, welfare and entitlement expansion funded with increased deficit spending have created an imbalance in America’s economic system. It’s this disequilibrium between fiscal and monetary policies that drives gold to outperform in a country’s currency. The Federal Reserve capped interest rates near zero back in 2008 and the federal budget deficit ballooned to $1.4 trillion. In fact, both the deficit as a percentage of GDP (negative 11 percent) and federal government debt as a percentage of GDP (nearly 65 percent) are at the highest levels since 1950. This has helped fuel gold’s rise through $1,000 and $1,500 an ounce.

Striking Portfolio Balance with Gold Stocks

Gold stocks have historically ranked among some of the most volatile asset classes. Over any given one-year period, it is a non-event for gold stocks to move plus or minus 38 percent. This DNA of volatility is about three times that of gold bullion, which carries an annual volatility around 13 percent.

Despite this volatility, our research shows that investors can use gold stocks to enhance returns without adding risk to the portfolio.

In 1989, Wharton School finance professor Jeffrey Jaffe completed an academic study that illustrated the effects of portfolio diversification into gold stocks. Jaffe’s original study covered the period from September 1971, just after President Nixon ended convertibility between gold and the dollar, to June 1987.

During Jaffe’s study period, the average monthly return for the S&P 500 was 0.89 percent. Gold stocks, as measured by the Toronto Stock Exchange Gold and Precious Minerals Total Return Index, converted to U.S. dollars, performed considerably better, returning an average monthly return of 1.42 percent.

On the risk side, gold stocks had greater volatility (measured by standard deviation) than the S&P 500. But Jaffe found that, because of their low correlation to U.S. stocks, adding a small percentage of gold-related assets to a diversified portfolio slightly reduced overall risk.

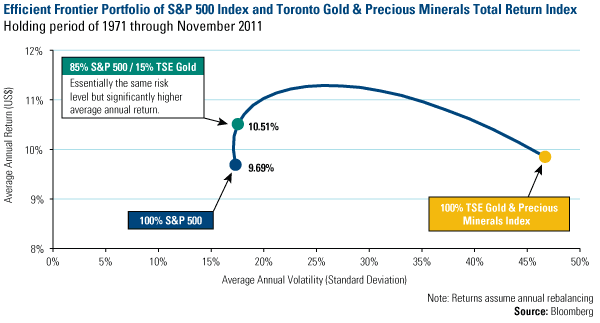

Here is an updated version of Jaffe’s results.

To find an optimal portfolio allocation between gold stocks and the S&P 500, the efficient frontier plots different portfolios, ranging from a 100 percent allocation to U.S. stocks (the S&P 500) and no allocation to gold stocks, and gradually increases the share of gold stocks while decreasing the allocation to U.S. equities.

Assuming an investor rebalanced annually, our research found that a portfolio holding an 85 percent allocation to the S&P 500 and a 15 percent allocation to gold equities* had essentially the same volatility as the S&P 500 (horizontal axis) but delivered a higher return (vertical axis). In other words, the addition of a small allocation to gold stocks increased portfolio returns with no increase in the portfolio’s volatility.

Between September 1971 and November 2011, the S&P 500 averaged a 9.69 percent annual return. A 15 percent allocation to gold equities and an 85 percent allocation to U.S. stocks, with annual rebalancing to maintain the allocations, would have yielded, on average, an additional 0.82 percent per year.

How much is 0.82 percent per year?

Let’s use a hypothetical $100 investment as an illustration. A $100 investment in gold stocks in 1971 would have grown to nearly $5,100 at the end of November 2011, while the same amount in the S&P 500 Index would be worth about $4,800.

But look what happens when you combine the two. Assuming the same average annual returns since 1971 and annual rebalancing over 40 years, a hypothetical $100 investment in a portfolio with 15 percent gold stocks would be worth about $6,600. That is 37 percent greater than the $4,800 for the portfolio solely invested in the S&P 500, while adding virtually zero risk.

U.S. Global Investors consistently suggests allocating up to 10 percent gold in a portfolio, so we also looked at returns for investors at that level. In dollar terms, a hypothetical $100 investment in the 90-10 portfolio would grow to $6,022 over the ensuing 40 years (assuming annual rebalancing), compared to $4,820 for the portfolio solely invested in the S&P 500.

And when you look at the efficient frontier in the chart, a portfolio with a 10 percent weighting of gold stocks and a 90 percent allocation to the S&P 500 has also historically increased return with no additional volatility.

More than two decades and many ups and downs have passed since Jaffe published his study, but our follow-up research shows that the relationship among gold, outsized returns and volatility has remained consistent through the past four decades.

If you haven’t already completed your annual portfolio rebalancing, this may be an opportune time recalibrate your portfolio with gold stocks.

- Bulenox: Get 45% to 91% OFF ... Use Discount Code: UNO

- Risk Our Money Not Yours | Get 50% to 90% OFF ... Use Discount Code: MMBVBKSM

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply