Karl Smith at Modeled Behavior notes Bloomberg’s story on rising rents, summarizing it with:

In any case the point is that rents are rising, and rents are hefty portion of inflation.

It seems to me that the story has two parts. The first is, as Smith notes, that upward pressure on rents will put upward pressure on inflation. No problem there. The second part of the story is the message that the Fed is missing the importance of rising rents, and thus we are on the verge of runaway inflation:

Federal Reserve Chairman Ben S. Bernanke and his colleagues say they will hold interest rates at record lows for an “extended period,” based on an assessment that slack in the economy from 9 percent unemployment will help subdue core inflation and any threat of accelerating prices likely will be “transitory.” Not everyone agrees with that judgment.

“They should have looked at rents,” said Maury Harris, chief U.S. economist in New York at UBS Securities LLC, whose team at UBS was the most accurate inflation forecaster over 2009 and 2010, according to Bloomberg calculations. “They’re putting too much weight on the ‘slack is all that matters’ theory. It matters but, for heaven’s sake, it’s not all that matters.”

Housing has become “a contributor to inflation, and it continues to rise,” agreed Bruce McCain, chief investment strategist at the private-banking unit of KeyCorp in Cleveland, with $22 billion in assets under management. That’s partly why he’s advising clients to look at “specifically, a heavier mix of equities, and maybe the use of TIPS to mitigate the effects inflation could have over 10 years or longer.”…

…“When you look at the longer-term portion of a bond portfolio, consider pretty carefully the ravaging effects that inflation could have,” McCain said in an interview. He estimates that rents have accounted for about 1 percentage point of the last decade’s 2.4 percentage point rise in prices and soon may revert to or overshoot this trend.

“The worse it gets for apartment rentals, the more you’re going to see that number adding to the overall inflation rate,” he said.

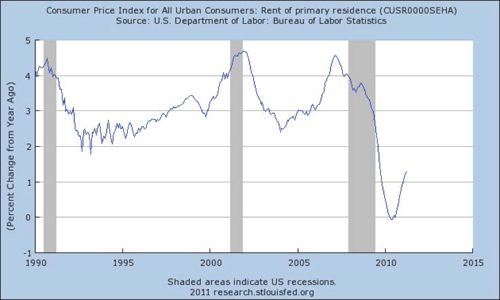

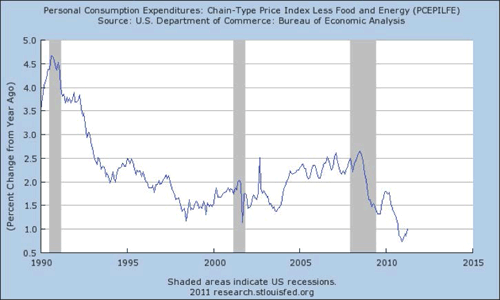

I have trouble seeing the impending disaster when I look at the recent history:

My first thought is that I think we were generally happier with the overall economic environment when rents were growing in the range of 3 to 4%. I recall the late 1990’s as being pretty good. People seem to be less happy with the conditions that drop rent growth to zero. My second thought is that accelerating rents does not itself lead to runaway inflation:

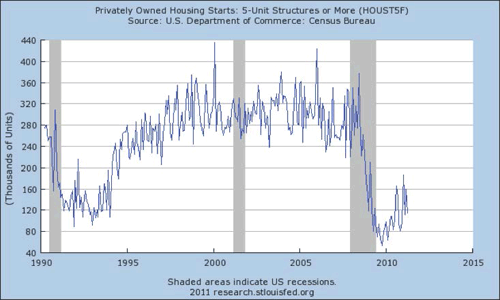

My third thought was that rising rents might induce a supply side response that seems desperately needed at this juncture. If rents are stagnant, why should developers build apartments? Why should banks finance apartment construction? This is a sector with significant unused capacity:

Looks like there should be no problem expanding the construction of multifamily housing. I think there are a whole bunch of people and firms that are looking to jump back into that market. One thing I know for sure we can still build in America – housing. This suggests that supply growth will be at hand to temper the impact of demand growth on prices. And I thought the whole point of pushing the economy back to trend was to put people back to work.

Bottom Line: Yes, inflation will (hopefully) rise – that is part of reestablishing a long-run equilibrium. Indeed, a reasonable case can be made for allowing inflation growth to accelerate sufficiently to return to pre-recession price trends. But it will be tough to reestablish that long-run equilibrium if policymakers panic at each price increase and step on the brakes long before a clear path to potential output is established.

- Bulenox: Get 45% to 91% OFF ... Use Discount Code: UNO

- Risk Our Money Not Yours | Get 50% to 90% OFF ... Use Discount Code: MMBVBKSM

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply