I sold off my Molycorp (MCP) last week. The stock is up about 400% in less than a year. MCP has a market cap of just $5.4b. It has no earnings at all. Not much in the way of sales either. About $25mm in the most recent quarter.

I have little doubt that MCP will succeed as a mining company and it will be producing rare earths in the coming years. So maybe the stock price is justified. But this is a bet on the come. At a price of 50Xs trailing sales it makes it one of the most expensive stocks out there.

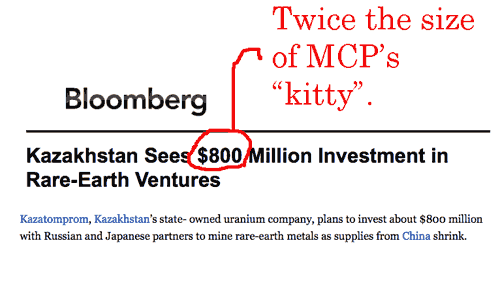

We know that RE aren’t rare. It’s extracting them that’s the problem. It’s a dirty business. We also know a thing or two about greed and money. That’s also a dirty business. When it is possible to raise $400mm and create a market value of $5b (MCP) on nothing more than a vague promise about future results one can expect that there will be many copycats.

I saw this article this morning. It made me feel a bit better about running for cover on MCP. Please don’t read this and conclude that MCP is a short. The stock could be up $10 in any given week. Calling the top is a fool’s game. Especially when the price is already at foolish levels. But taking profits can be ‘sweet’ too.

- Bulenox: Get 45% to 91% OFF ... Use Discount Code: UNO

- Risk Our Money Not Yours | Get 50% to 90% OFF ... Use Discount Code: MMBVBKSM

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

None of the metals listed in the linked article are “rare-earths”…