Richard Fisher, head of the Dallas Fed, flagged the risk of monetizing government debt and bashed the government for out of control spending. He felt the Fed was now “an accomplice to Congress’ fiscal malfeasance” and came out against further Quantitative Easing (QE). He further said he would back Fed tightening at the earliest signs of inflation.

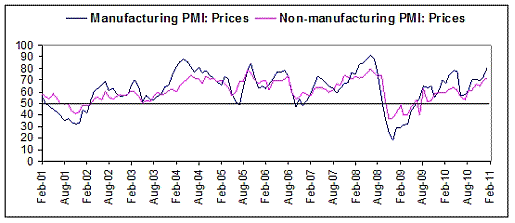

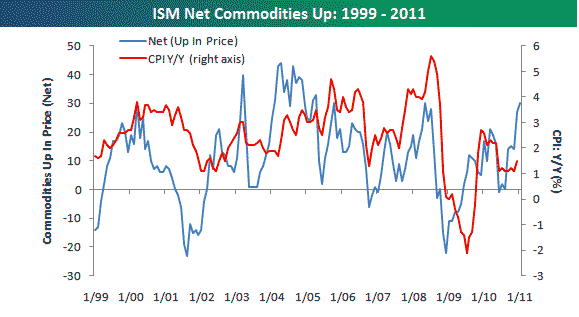

He may be facing that prospect as early as March. The January ISM Reports showed economic activity growing at rates not seen since August 2008, which is good news, but the “prices paid” index grew even faster:

Bespoke notes how the ISM prices paid is outpacing the official inflation rate, and the last time commodiites prices rose this much, CPI rose 5%, over 3x higher than currently reported:

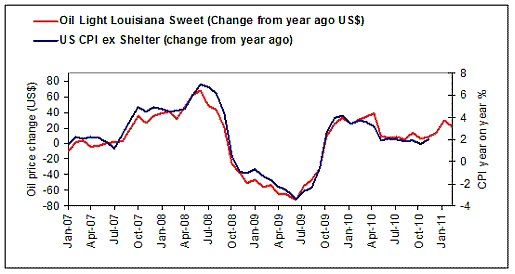

Pierre du Plessis looked at the inflation data and concludes that the CPI excluding housing tracks closely to the oil price with a month’s lag. if oil holds up in the $90+ range through Feb, the CPI ex-housing should hit 3.5% in March:

These factoids put the Fed’s policy in a vise. If QE2 has succeeded by improving economic activity, there is no need to continue it. If it has driven prices up faster than growth, it would now need to try to put the inflation genie back in the bottle by ending QE and as Fisher noted, tightening instead of loosening.

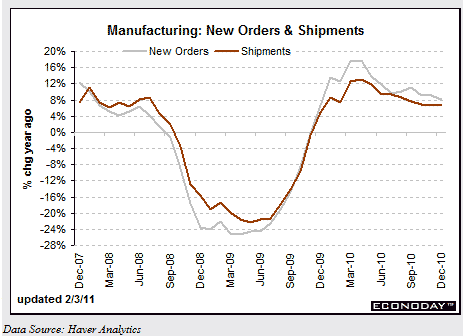

A third factor is the drop in inventories and the rise in imports shown in December. There have been some stories of stockpiling of materials by US companies, as a reaction to rising prices; but overall inventories have dropped. This may indicate a demand problem, that since pricing cannot be passed through, rather than be caught in a margin squeeze, producers are pulling back in stock. In fact, both new orders and inventories have been trending down for most of 2010:

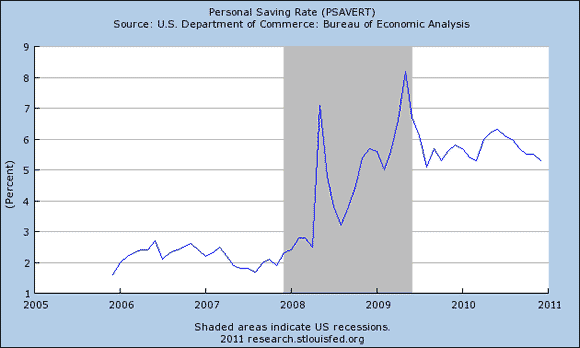

The Fed talks about how the “wealth effect” can spur recovery, and seems to believe the rising stock market (since the QE2 announcement last August) is responsible for increased spending. Presumably that has contributed to spending, along with consumers pulling money out of savings, as shown in this chart from Econophile, who concludes that the wealth effect and reduction in savings are both ephemeral consequences of QE, not signs of a sustainable recovery:

So now the Fed is caught in a three-way vice:

- they need QE to continue an apparent recovery

- the recovery politically undermines the need for QE

- especially because they risk inflation getting out of control

Leave a Reply