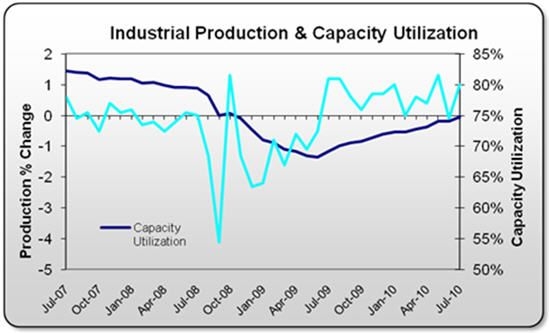

In this Summer of Disillusionment, where the plethora of bad news is driving a bond bubble, we had some rare good news: an increase in industrial production of 1% that beat expectations of 0.6%. Production is up almost 8% above year-ago levels, and if this pace continues, we should be back to a full recovery by next summer. This is the first positive surprise after a series of disappointing reports on retail sales, housing and building permits. Is this a harbinger of a change of trend back towards an economic recovery?

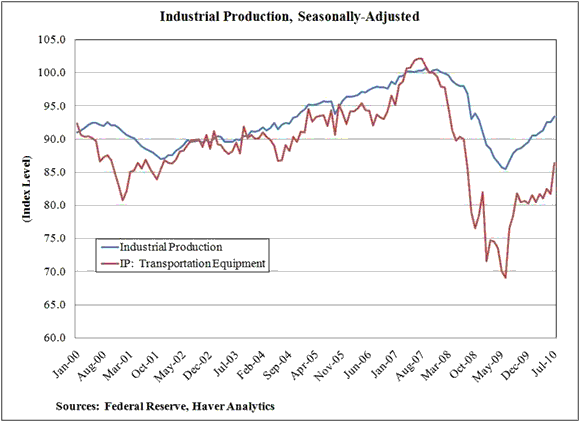

The report stands out against other negative news. This raises the concern that it is based on a statistical anomaly. A major component of the increase is the auto sector, and if that is carved out of the report a strange spike emerges in the data:

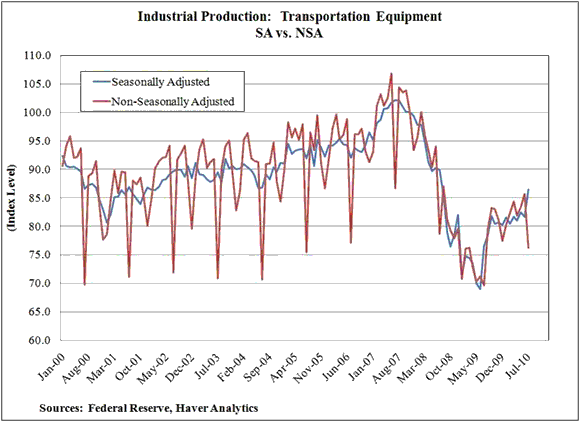

The spike comes from seasonal adjustments that may be skewed because normally July is a down month – so a lesser decline in July causes a positive blip up after adjustment. You can see in this comparison of non-seasonal numbers (red) vs adjusted numbers (blue) how a steep drop in actual production was turned into a steep increase in adjusted production:

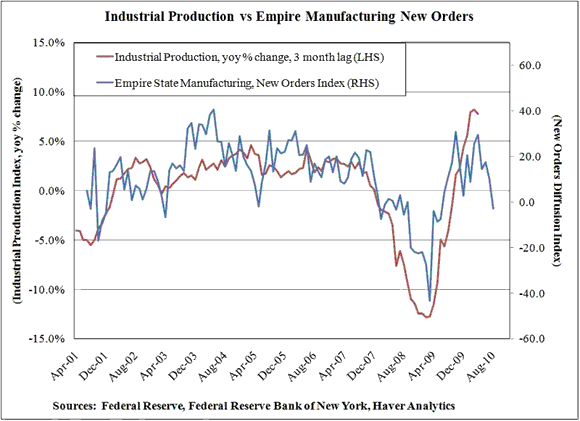

The statistical blip is not showing up in other reports. The Empire State Manufacturing Index came out weaker than expected. The index is still positive at 7, and rose a bit from its July level at 5, but has fallen from a 32 level in April and a 20 level in June. When compared with the new orders component of the Empire State index, industrial production looks like it is rolling over towards a decline, not accelerating into a rise:

driven mainly by gov't handouts, handouts are over (or are they?).