In June, Personal Income (PI) was unchanged from May, a slowdown from the 0.3% increase posted in May and the 0.4% increase recorded in both April and March. Disposable personal income, or after-tax income, followed pretty much the same path: unchanged in June after rising 0.3%, and increases of 0.5% in April and 0.4% in March.

Personal Consumption Expenditures (PCE) were also unchanged on the month, but that is not as big a slowdown as on the income side since PCE has been growing at a snail’s pace for several months now, up just 0.1% in May and down 0.1% in April, but up 0.5% in March. The weak growth on both the income side and the spending side in June suggests that the next revision to second-quarter GDP will be downward.

The sources of income were also on the weak side. Private wages and salaries fell by $5.2 billion in June after increasing by $19.2 billion in May. More than all of that decline was on the goods-producing side, where wages fell by $8.9 billion, rather than the May increase of $10.4 billion. Service-sector wages continued to increase, but at a slower rate, rising $3.7 billion rather than $8.8 billion.

The Census had an impact on the government wages portion of personal income. The layoff of temporary Census workers subtracted $3.4 billion in June, while hiring them added $5.7 billion in May.

Income from capital, i.e. interest received and dividends continued to increase, but only rose by $1.9 billion rather than by $4.1 billion. Rental income rose the same $1.8 billion it did in May. The only category showing greater growth in June than in May was in government support payments (transfer receipts), which rose by $7.2 billion rather than the $6.0 billion in May.

Savings Rate

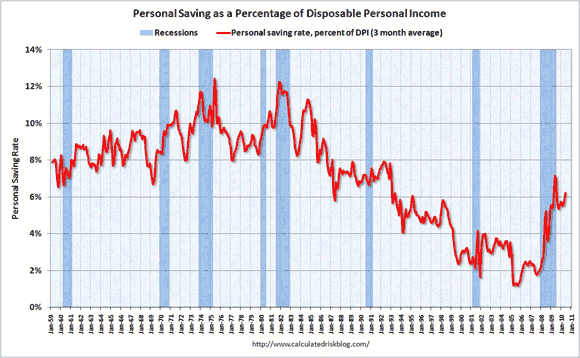

The Savings Rate edged up to 6.4% from 6.3% in May, but the big news buried in this report was the revisions to prior years. For all of 2007, 2008 and 2009, PI was revised up and PCE was revised down. That resulted in some rather dramatic changes to the savings rates.

For all of 2007, the personal savings rate is now calculated to be 2.1% rather than the 1.7% we thought it was. The rate for 2008 was revised up to 4.1% from 2.7% and for 2009 to 5.9% from 4.2%.

As the graph below (from http://www.calculatedriskblog.com/) shows, the savings rate was on a secular decline from the early 1980’s to 2006 or so. It has since staged a massive rebound. A falling savings rate provides a tailwind for the economy, but a low savings rate is ultimately very dangerous and unsustainable for the economy.

If people are simply holding on to their wallets and not spending, then the economy suffers. If they are spending more and saving less than they did, then the economy will see more activity. Ultimately, though, savings are needed to finance the investments needed for future growth. If we cannot generate the savings domestically to finance our growth, it means they have to be imported.

That means a higher trade deficit, and that the country becomes indebted to the rest of the world. During this period of secular decline in the savings rate, the U.S. went from being the world’s largest creditor to being the world’s largest debtor.

The Curse of the Housing ATM

A large part of the decline in the savings rate can be tied to rising asset prices, particularly for houses. People figured that if the value of the house they were living in was growing quickly, they could save less and consume more today, and then be able to spend the gains in the value of the house when it came time to retire or put the kids though college. Large numbers of people started to use their houses as if there were an ATM in the kitchen, using Home equity lines of credit, and cash out refinancing to support current consumption, such as go on vacation or buy a new car.

The popping of the housing bubble changed all that. Housing wealth, which is the only real wealth that millions in the working and middle classes had, has evaporated. For 14.75 million homeowners in the first quarter, not only do they have no housing wealth anymore, but they owe more than the house is worth (see “Housing: Still Flooded“).

As a result they have to put away more of their current income and repair their shattered personal balance sheets. The balance sheet repair operation has begun, but it is a long way from finished. As a result, the savings rate will probably continue to rise (not necessarily in a straight line, but trending up over time).

If the rise in the savings rate occurs because income is rising faster than spending, it will be less painful than what we saw during the recession, when it was spending that simply fell off a cliff, and income declined more slowly. Still, it means that economic growth will be lower than it otherwise would have been, had the savings rate stayed stable. Holding more money in the bank might be nice for the likes of J.P. Morgan (JPM), but it is bad news for retailers like Macy’s (M).

It will be the more discretionary parts of the economy that will grow more slowly. Less money spent on vacations means that fewer people will take cruises on Carnival Cruise Lines (CCL). People will tend to hold on to their cars longer, meaning fewer new cars sold by Ford (F).

The economy can handle this if it happens gradually, but it still means lower growth than what would have occurred. In essence, at least some of the economic growth between 1982 and 2006 was a mirage — a case of living large on the credit card. Now comes the part where we have to pay off the bill.

This will be a long-term headwind for the economy, just as the falling savings rate provided a tailwind that lasted for a quarter of a century. The headwind will probably not last that long, but don’t expect it to be over in just a few months, or even a few years, for that matter.

CARNIVAL CORP (CCL): Free Stock Analysis Report

JPMORGAN CHASE (JPM): Free Stock Analysis Report

FORD MOTOR CO (F): Free Stock Analysis Report

MACYS INC (M): Free Stock Analysis Report

- Bulenox: Get 45% to 91% OFF ... Use Discount Code: UNO

- Risk Our Money Not Yours | Get 50% to 90% OFF ... Use Discount Code: MMBVBKSM

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply