EWI has been getting smarter on investing in China, and prepared a fairly insightful report on Chinese and Japanese markets that weaves together cultural as well as economic trends. The result is a roadmap for their future. As an affiliate, I get broadsided with various EWI reports, and generally let them fly by. This one, however, I highly recommend. You can download it here.

The starting point is the huge credit bubble inside China. This has led to an ebullient social mood, as shown by the hemline indicator among other items in the report (see picture). (Short skirts = bubble mood. Short skirts in Army = govt-led bubble.) The report compares China today to Japan in the ’80s, and lays out a roadmap for China that begins with the evaporation of a lot of credit-fueled illusory wealth.

The starting point is the huge credit bubble inside China. This has led to an ebullient social mood, as shown by the hemline indicator among other items in the report (see picture). (Short skirts = bubble mood. Short skirts in Army = govt-led bubble.) The report compares China today to Japan in the ’80s, and lays out a roadmap for China that begins with the evaporation of a lot of credit-fueled illusory wealth.

Beyond the report, other indicators support their roadmap. In order to fuel the growth and keep their currency pegged at a low rate to the Dollar, the Chinese workers have been forced to save at low rates (earning less than the inflation rate), or put their earnings into real estate which has trapped massive amounts of capital. Trapped? The resell market in China is near zero, on the order of 1% annually or less. Buyers would rather jump into a newly constructed flat than look for an old one. Ken Rogoff thinks the property collapse in China is already starting. Capital is being badly malinvested, and the fault lines across the lucky and unlucky are beginning to fray. What happens to social mood when the bubble bursts?

An interesting on-the-ground observation from a Michigander’s visit to China is worth pondering. He comes from Ground Zero (Detroit) of the huge collapse in US housing (values and vacancies), and he sees the same signs if not worse in Chengdu, especially the many vacant buildings:

Chengdu seemed worse [than Detroit]. I couldn’t tell what or why I found myself gawking at massive developments at 3 pm in the middle of the week without signs of construction, occupancy, or any activity. These were not mere strip malls but giant commercial, industrial, residential cities within a city. Skyscrapers, street front shops, apartments, malls, many I observed were vacant.

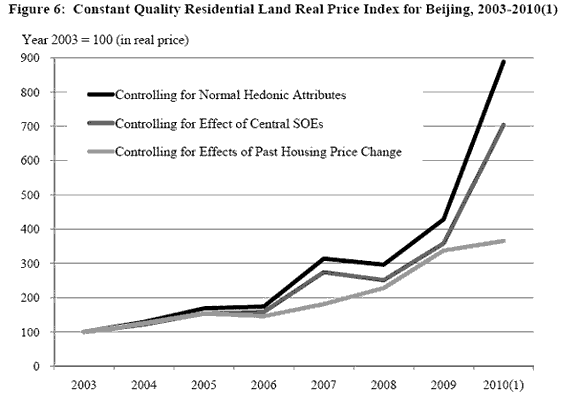

A recent study by NBER concludes that the recent rise in home prices in Beijing are driven by land values, and they have increased in real terms by an astounding 800% since 2003, an increase they characterize as “unprecedented”. This could be bigger than the Japan bubble of 1989.

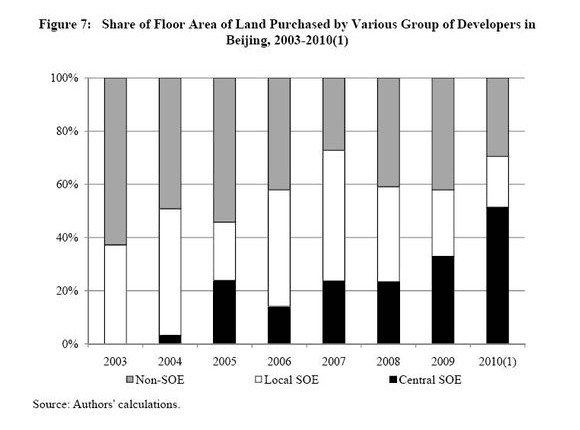

An increasingly-large portion of purchases has been by a decreasing number of buyers, specifically a handful of of huge companies backed by the central government (so-called SOEs), who overpay believing they are too big to fail. Apparently what is driving them is to hedge against the rising inflation in China – but the socioeconomic perspective of the EWI analysis says that explanation really reflects one of many rationalizations for simply acting to an ebullient social mood. As the breadth of purchasers narrows, the end is nigh, and in the end only the government will be left to keep the party going.

Econbrowser looks into this study and has a telling chart which shows the housing bubble in land prices, and discusses the differences and similarities to the recent US housing bubble:

Mish goes further and finds evidence of Ponzi Shark Loan operations that are driving this bubble: local officials, required to meet central government growth figures, give permits for real estate development in return for bribes. The loans for down payments to buy these new flats come from locals who have no good place to invest their earnings and pool it for high-interest loans to property buyers, keeping the bubble going. It may be the SOEs are bailing out the collapsed loan sharks, but more likely they have emerged to now be over half of all housing purchases to also keep the party going (see last chart, from the NBER story above) because real buyers are unable to keep up with the horrifically expensive prices, now 22 times average incomes. This is similar to our Fannie/Freddie eventually owning 90% of the final stages of our housing bubble.

- Bulenox: Get 45% to 91% OFF ... Use Discount Code: UNO

- Risk Our Money Not Yours | Get 50% to 90% OFF ... Use Discount Code: MMBVBKSM

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply