“Will they or won’t they?”

In ordinary circumstances, when such a question is asked on the day of an FOMC policy announcement, it refers to whether or not the Fed will adjust policy rates. Of course, the past three years have been anything but ordinary, and desperate times have called for desperate measures.

So when we ask “will they or won’t they” of the Fed today, what we’re really asking is whether or not they’ll change the “extended period” language, which is popularly believed (though not officially sanctioned) to render a promise of no rate hikes for a period of six months thereafter. Desperate stuff indeed.

For choice, Macro Man would suggest that they give it another few weeks and then tweak the language at the next meeting. After all, having gone through extraordinary pains to assure the market that all its fumbling with the plumbing carried no monetary policy implications, the Fed would, in a sense, be contradicting itself by taking the first opportunity to alter language that (rightly or wrongly) is so intimately connected with the trajectory of monetary policy.

Still, that hasn’t stopped markets from wondering (and scrambling.) Equity bears saw defeat snatched from the jaws of victory yesterday as it took the magic of Monday to erase what looked like a “Fed risk premium” down day.

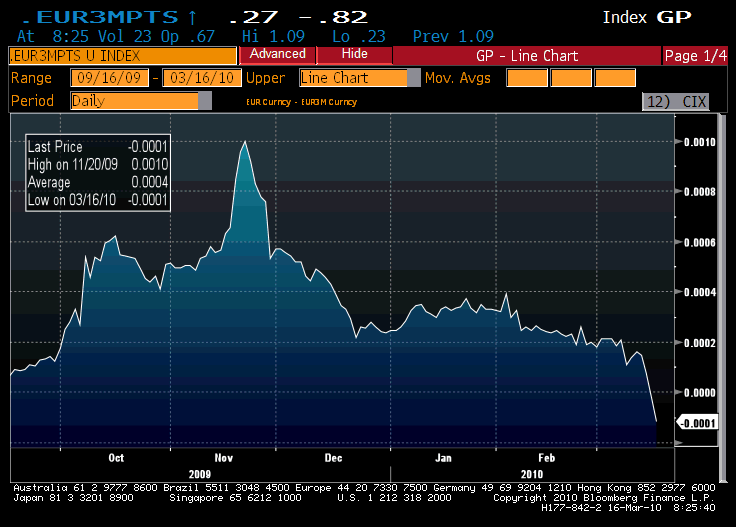

More interestingly, the FX forward market has seen a scramble of dollar borrowing, sending the 3m EUR/USD points into negative territory. This, for the non-expert, means that 3m USD interest rates are trading above those in the Eurozone. If you look at your screen and see that 3m LIBOR is 0.25% and 3m EURIBOR is 0.64% and wonder how this can be, well….it pretty much tells you what a mockery LIBOR has become.

(click to enlarge)

In any event, while the demand for dollars may well be sourced in non-US banks potentially being cut off from cheap funding from the GSEs, it is nevertheless telling. Squeezes in $ rates/dislocation in the FX forward market have tended to accompany downdrafts in equities…so if you’re thinking of a cheeky SPX purchase: caveat emptor.

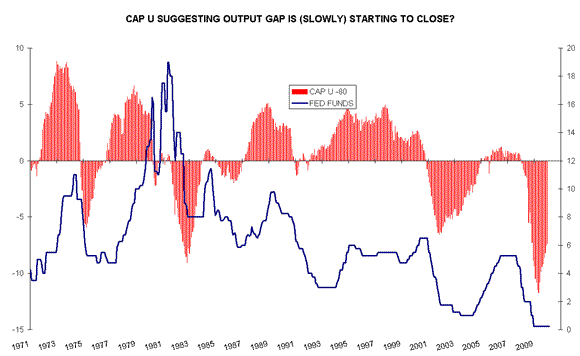

The question then arises of whether the Fed should be contemplating policy tightening. Your view on this almost certainly depends on your view on US housing (outlook: poor), consumer savings, employment, pent-up capex demand, and other things. The Fed themselves have unsurprisingly highlighted “resource utilization” as a prime determinant of the the trajectory of monetary policy.

To be sure, there remains ample slack in the economy…but by most m6easures that slack is being reduced somewhat. The unemployment rate, even U-6, is well off its highs; industrial capacity utilization, meanwhile, has also begun to tick up steadily.

The appropriate question on the output gap is strikingly similar to that on interest rates: is it the level that matters….or the change? Academic opinion on monetary policy is mixed; the true answer is probably that they both matter, to some extent. So the question then becomes: how much narrowing of the output gap is required before the Fed feels compelled to adjust policy?

The correct answer is almost certainly “quite a bit more.” But if the next question is “how much narrowing of the output gap will be required for the Fed to start wishing to give itself some flexibility in its decision-making?”, then the answer might be markedly different.

A separate issue, of course, is whether the Fed keeps the funds rate as the primary instrument of monetary policy, or whether they move to targeting interest on excess reserves (IOER.) Macro Man’s understanding is that the latter is set by the Board of Governors, not the Open Market Committee; if that is the case, then targeting IOER will a) shunt the regional presidents further off to the side in terms of significance, and b) raise the question of when the hell the Fed plans to fill out the Board of Governors!

As an aside, students of history will recall that in the early days of the Fed, there was a clear split in the policy making responsibilities of the regional presidents and the central Board of Governors…and didn’t that work out well!

In any event, good luck for this evening, and may BB and co. give you what you wish for.

- Bulenox: Get 45% to 91% OFF ... Use Discount Code: UNO

- Risk Our Money Not Yours | Get 50% to 90% OFF ... Use Discount Code: MMBVBKSM

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply