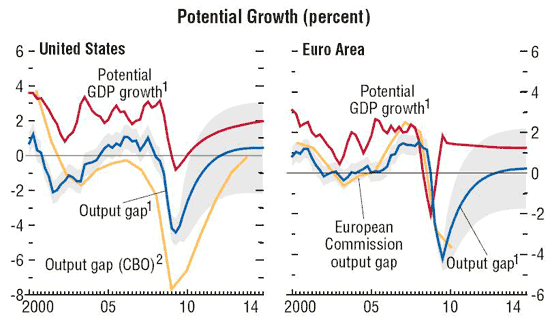

After reading Nouriel Roubini’s latest article in the FT I now feel less certain on what the Fed should be doing going forward. One one hand I see figures like the one below from the IMF’s World Economic Outlook (p. 32) that point to excess global capacity and the ongoing threat of global deflation (the bad kind) and come to same conclusion Scott Sumner does:

If the Fed adopted a much more expansionary monetary policy, and if the PBOC kept its policy stance the same, then world monetary policy would become more expansionary, and world aggregate demand would increase. That would help everyone.

In short, the Fed should use its monetary superpower status to ensure there is ample global liquidity and in so doing stabilize global nominal spending.

On the other hand, Nouriel Roubini’s claims the current Fed policies in conjunction with a large dollar carry trade is creating a new set of asset bubbles:

Risky asset prices have risen too much, too soon and too fast compared with macroeconomic fundamentals… So what is behind this massive rally? Certainly it has been helped by a wave of liquidity from near-zero interest rates and quantitative easing. But a more important factor fueling this asset bubble is the weakness of the US dollar, driven by the mother of all carry trades. The US dollar has become the major funding currency of carry trades as the Fed has kept interest rates on hold and is expected to do so for a long time.Investors who are shorting the US dollar to buy on a highly leveraged basis higher-yielding assets and other global assets are not just borrowing at zero interest rates in dollar terms; they are borrowing at very negative interest rates – as low as negative 10 or 20 per cent annualised – as the fall in the US dollar leads to massive capital gains on short dollar positions.

Let us sum up: traders are borrowing at negative 20 per cent rates to invest on a highly leveraged basis on a mass of risky global assets that are rising in price due to excess liquidity and a massive carry trade. Every investor who plays this risky game looks like a genius – even if they are just riding a huge bubble financed by a large negative cost of borrowing – as the total returns have been in the 50-70 per cent range since March.

People’s sense of the value at risk (VAR) of their aggregate portfolios ought, instead, to have been increasing due to a rising correlation of the risks between different asset classes, all of which are driven by this common monetary policy and the carry trade. In effect, it has become one big common trade – you short the dollar to buy any global risky assets.

Yet, at the same time, the perceived riskiness of individual asset classes is declining as volatility is diminished due to the Fed’s policy of buying everything in sight – witness its proposed $1,800bn (£1,000bn, €1,200bn) purchase of Treasuries, mortgage- backed securities (bonds guaranteed by a government-sponsored enterprise such as Fannie Mae) and agency debt. By effectively reducing the volatility of individual asset classes, making them behave the same way, there is now little diversification across markets – the VAR again looks low.

So the combined effect of the Fed policy of a zero Fed funds rate, quantitative easing and massive purchase of long-term debt instruments is seemingly making the world safe – for now – for the mother of all carry trades and mother of all highly leveraged global asset bubbles.

Roubini is not optimistic about what this means for the future:

[O]ne day this bubble will burst, leading to the biggest co-ordinated asset bust ever: if factors lead the dollar to reverse and suddenly appreciate – as was seen in previous reversals, such as the yen-funded carry trade – the leveraged carry trade will have to be suddenly closed as investors cover their dollar shorts. A stampede will occur as closing long leveraged risky asset positions across all asset classes funded by dollar shorts triggers a co-ordinated collapse of all those risky assets – equities, commodities, emerging market asset classes and credit instruments.

So what is the bigger threat: global deflation or “the mother of all carry trades”-driven asset bubbles? Tim Lee via Buttonwood also sees potential problems to the unwinding of this dollar carry trade. I hope there is another way out for the Fed.

- Bulenox: Get 45% to 91% OFF ... Use Discount Code: UNO

- Risk Our Money Not Yours | Get 50% to 90% OFF ... Use Discount Code: MMBVBKSM

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Good article, But Let me, play devils advocate. Let get right off saying I would be a deflationist, but with no Paul Vockler. For this bubble to collapse the FED, will have to raise the key funds rate, which would effectively raise borrowing costs for Gov’t and a host of companies, and citizens. This, would spark such a reversal but here’s what you did not mention in your Mother of all Deflation argument, Is in that scenario, would the FED sit idly, & keep raising the rate as US Stocks, equities, commodities fall, maybe even make New Lows. Given the 1930 deflation happened due to the natural limit of money supply, given a gold standard. I believe Inflation will win out. A. if the economy is still too fragile, FEDS words by 2010, third quater, and raise rates, and the labor market still shedding jobs, the economy will wither & real deflation will be back. THEN the FED WILL slash interest rates & inject liquidity again and effectively stop tightening efforts.

B. Or what were seing in todays markets, continues, doesn’t stop due to lack of political support & accommodative FED, the more low interest stimulas doles out, the higher the markets go, and that much harder to raise rates. The Amercan consumer is not back. So if we get a rising dollar, all that money Amercan companies are making from favorable exchange rates will dry up as it becomes expensive globally to buy US. I do not see the FED, tightening as that will bring real deflation, They picked their Poison, death by Inflation as the FED will not tighten on institutions that received bail out funds, if they try, it wont work & they’ll slash rates within the 1st 6 months of a rate hike. The more deflation that occurs, the more the FED will Inflate. No deflation, No change of course. For a history of the FED rate hike look at 2001-07, 5%; failed. 1970’s-82 Paul Vockler, 20% rates; succes. The carry trade is a pretty major blunder by the FED, gives me no hope that they will get it right.

If a dollar crash were to occur, it might happen because foreign investors decide that the U.S. has fallen into a so- called tax trap. A tax trap occurs when a nation finds itself unable to increase revenue by lifting tax rates. Such a circumstance, if paired with mounting deficits, can lead to wholesale flight from a nation’s assets

Why might the U.S. be in a tax trap? The problem is that the U.S. income tax, a primary source of federal revenue, is very progressive, and has high rates. When rates are already high, it becomes harder and harder to raise money by lifting them more. This is, of course, the observation that made economist Arthur Laffer famous, and for the U.S. it is a real concern.

The government deficit already looks like it will approach 9-12 (estimate) trillion over the next decade

When foreign investors see that higher taxes deliver little new revenue while spending soars, they will head for the exits. The dollar will be effectively dead if we cant prove we know how to balance budgets.