The May employment report should help ease concerns about the health of the economy, but will have little impact on the outcome of next week’s FOMC meeting. Fed officials had largely already written off the June meeting, and I think it is too little too late to expect them to reverse course now. Instead, the report puts the focus squarely on September.

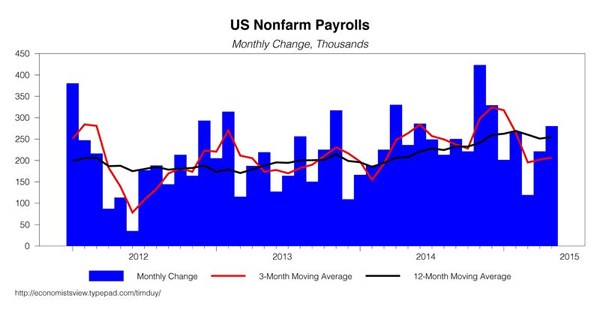

Nonfarm payrolls gained 280k for the month, with upward revisions adding 32k to the previous two months. The March slowdown now looks like what it was – the typical kind of variability we see in this report:

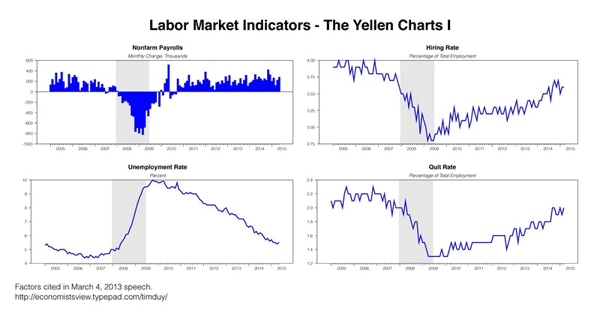

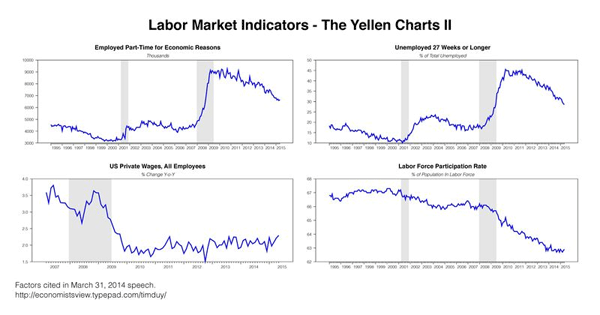

The unemployment rate edged up on the back of an increase in the labor force participation rate, a positive development in light of the downward demographic push on the labor force. In the context of indicators previously identified by Fed Chair Janet Yellen, the overall picture looks like:

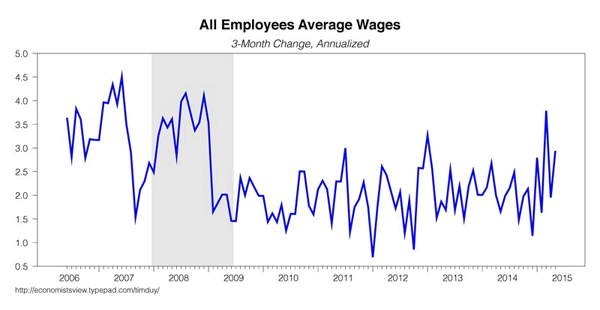

Sustained improvement in labor markets as slack slowly dries up. And I would say the signs that wage growth is gaining traction are increasing; the three-month trend is heading up:

I am not ready to sound the “all clear,” but I am optimistic that we are getting there. That said, not getting there fast enough to dramatically change the path of monetary policy just yet. Data since the beginning of the year, especially the GDP data, spooked Fed officials pretty badly – they just weren’t sure what was persistent and what was temporary. The employment data suggests the latter is largely at play. Moreover, I don’t think they fully appreciate the implications of a lower growth trajectory on the quarterly GDP readings. These zero and sub-zero events are more likely to happen than in the past. The upshot is that a June rate hike was essentially off the table before this report, and is after this report as well.

Bottom Line: The resilience of the job market – clearly foreshadowed by the initial claims data – suggests that the weakness in recent GDP numbers is less than meets the eye. That weakness, however, already deterred Fed officials from a June rate hike, leaving next week’s meeting something of a nonevent. Fed Chair Janet Yellen will likely use the press conference to outline the case for a 2015 rate hike, but emphasize the data dependent nature of that decision and, more importantly, a focus on the path of rate hikes after the first hike. That is what the Fed would like us to be watching, and the data still suggests a fairly modest pace of tightening. Attention now shifts to the September meeting as the first in which we might anticipate sufficient data to support a rate hike. Given how badly the Fed was spooked by the first quarter, it seems unlikely that sufficient data will pile up by the July meeting. So that pretty opens up all of our summer schedules.

- Bulenox: Get 45% to 91% OFF ... Use Discount Code: UNO

- Risk Our Money Not Yours | Get 50% to 90% OFF ... Use Discount Code: MMBVBKSM

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply