New York Federal Reserve President William Dudley had a sit down with the Wall Street Journal in which he provides some key insights into Fed thinking. First, regarding the tepid pace of data, it’s the weather:

Mr. Dudley said that he still expects, “the economy should do better” relative to last year, growing at around 3% this year.

He said, however, it appears very likely that harsh weather slowed economic growth in the first quarter to under a 2% annual rate.

See also this Wall Street Journal report on weak February retail sales. As expected, the Fed will dismiss soft numbers as an artifact of the cold. (although I think the acceleration at the end of 2013 was less than meets the eye to begin with). That means the pace of tapering is not going to change at the next meeting. But guess what? Tapering is not really data dependent in any event. It is more appropriately described as “outlier dependent”:

“If the economy decided it was going to grow at 5% or the economy decided it wasn’t going to grow at all, those would be the kind of changes in the outlook that I think would warrant changing the pace of taper,” Mr. Dudley said Thursday.

How this is really any different from a fixed time-line is beyond me. If the range of acceptable outcomes to justify tapering is anywhere between 0 and 5% growth, the FOMC statement can be reduced by simply admitting that asset purchases are on a preset course. As I have said many times, the Fed wants out of the asset purchase business. It’s all about interest rates now:

Mr. Dudley affirmed that nothing’s changed when it comes to the short-term interest rate outlook. He said “we have a long time to go before we have to think about raising short-term interest rates.”

Sometime in 2015. The weaker the data, the deeper into 2015 is the first rate hike, all else equal.

Finally, look for changes in the next FOMC statement to reflect what has been true for some time:

The 6.5% marker “is already a little bit obsolete in the sense we are really close to it,” Mr. Dudley said. The level is “not really providing a lot of value in terms of our communications.”

The meeting later this month would be a “a reasonable time to revamp (the) statement to take out that 6.5% threshold,” he said. The Fed has amended its guidance to say rates could stay near zero well past that point as long as inflation remains in check.

The 6.5% marker is not a “little” obsolete. It is a “lot” obsolete. It became obsolete the minute the Fed made clear it was irrelevant as they had no intention of raising rates at that point. The are not going to replace it with another numerical guide. It will be replaced with qualitative, and ultimately discretionary, guidance.

Meanwhile, Dallas Federal Reserve President Richard Fisher made clear his view that asset bubbles are brewing left and right:

…there are increasing signs quantitative easing has overstayed its welcome: Market distortions and acting on bad incentives are becoming more pervasive.

Stock market metrics such as price to projected forward earnings, price-to-sales ratios and market capitalization as a percentage of GDP are at eye-popping levels not seen since the dot-com boom of the late 1990s. In the words of James Mackintosh, writer of the Financial Timescolumn “The Short View,” a not insignificant number of stocks in the S&P 500 have valuations “that rely on belief in a financial fairy.” Margin debt is pushing up against all-time records. And, in the bond market, narrow spreads between corporate and Treasury debt reflect lower risk premia on top of already abnormally low nominal yields. We must monitor these indicators very carefully so as to ensure that the ghost of “irrational exuberance” does not haunt us again.

Interestingly, former Federal Reserve Chairman Alan Greenspan writes today that such bubbles are just part of the territory:

Successful financial policy, in my experience, ironically spawns the emergence of bubbles. There was never anything resembling financial euphoria, or the bubbles it creates, in the old Soviet Union, nor is there in today’s North Korea. At the Federal Reserve during my tenure, we often joked that our greatest fear was that policy might be too successful. Achieving an underlying stable rate of growth and low inflation appears to have been a necessary and sufficient condition for the emergence of a bubble. We would conclude with mock seriousness that optimum monetary policy for bubble prevention was to create destabilizing inflation.

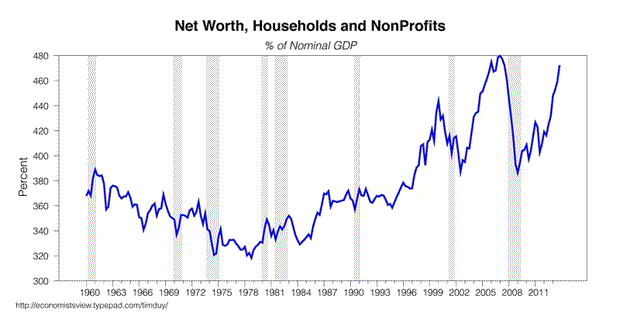

There is much of interest in the Greenspan piece (including his claims that the 1994 tightening was an attempt to derail the bubble of the 1990s) and little time to take it up now. As if on cue, the Federal Reserve release the latest flow of funds data. Check out net worth:

Approaching the high seen in the last asset price bubble. Doesn’t mean it can’t go higher.

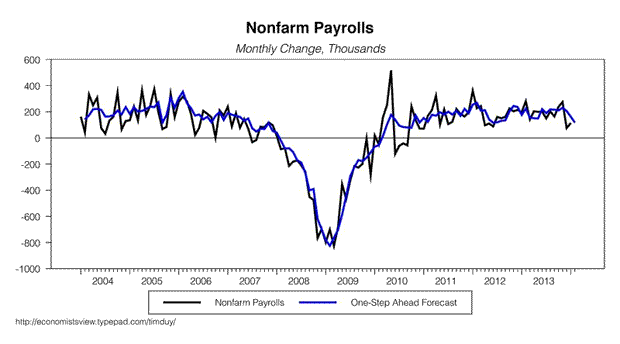

Tomorrow is employment report day. The general expectation is that weather played a starring role in depressing job growth while the ACA had a supporting role. Consensus is for 150k gain in payrolls with forecasts ranging from 80k to 203k. My recent track record has been a little (lot) shaky on this number of late, but maybe third time is a charm. Usual caveats apply about the insanity of forecasting a heavily revised rounding error of the massive monthly churn in the labor market. I will take the under this month and am looking for a gain of 118k:

More interesting will be the unemployment rate (what is the impact of the end of extended benefits?) and wage growth (are we seeing any yet?).

Bottom Line: Barring the outlier outcomes of either recession or explosive growth, tapering is on autopilot. Rate guidance is now qualitative and actual policy is discretionary. Incoming data is interesting for what it says about the timing of the first rate hike. So far, though, it is not telling us much given the Fed’s belief that weak data is largely weather related. The degree to which asset bubbles are a concern varies greatly accross Fed officials but the general consensus is that such concerns are of second or third order magnitude compared to missing on both sides of the dual mandate.

- Bulenox: Get 45% to 91% OFF ... Use Discount Code: UNO

- Risk Our Money Not Yours | Get 50% to 90% OFF ... Use Discount Code: MMBVBKSM

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply