Since the financial crisis started we have heard many commentators telling the Euro countries: “I told you so, this was a very bad idea”. The argument is that the Euro area is not an optimal currency area – a jargon used by economists to argue that the costs of having a single currency are larger than its benefits. While until 2008 things have looked fine, the crisis is the real test for the Euro area and it has failed. And it has failed because of what any standard macroeconomics textbook tells you: that once you give up your exchange rate you lose a stabilization tool and when a crisis that is asymmetric in nature comes along you suffer a prolonged crisis as the only way out is to let prices and wages fall (internal devaluation), a painful and inefficient process.

In a recent post, Paul Krugman reminds us once again of these arguments by comparing Ireland during the current crisis to Thailand or Indonesia during the Asian crisis. His argument is that the Asian economies recovered quite fast from their crisis while Ireland has not (and Greece has not even started any recovery). As Kevin O’Rourke puts it, Ireland looks like Thailand without the Baht.

The arguments seem solid and the evidence strong but I am somehow skeptical that we can that quickly conclude that the Euro was a failed experiment and that life without the Euro would have been better (and maybe I am reading too much into those posts and they are not really going that far in their statements).

What one wants to do is build a counterfactual: where would Greece or Spain or Ireland be if they had never joined the Euro? What would their currency have done for them before and after the 2008 crisis? Unfortunately we cannot build such counterfactual so the best we can do is to look for similar examples (such as Thailand during the Asian crisis). But let me argue that if one extends the set of examples and anecdotes some of the data does not speak that clearly against the Euro.

Before I start let me make two points:

1. I have no disagreement with the argument that rigidities in prices and wages make an internal devaluation a painful way to get out of a recession. A depreciation is a much faster way to reset relative prices. This is what I teach to my students.

2. I agree that the Euro area comprises a set of countries that are performing way below their potential. A combination of failed reforms, lack of economic leadership, a not very proactive central bank is producing a growth rate that is below potential (both before and during the crisis).

The point that I am trying to make is that among the list of problems that the Euro countries have, the Euro itself might not be the biggest one. While a devaluation could have helped established a faster recovery, its effects would have been uncertain and possibly small. I reach that conclusion by looking at data the same way Krugman and O’Rourke do. It just happens to be that I look at different data. Are my comparisons much better than theirs? Not sure (this is just a blog post, not a research paper). But I find them more relevant even if I have to admit that we have a great deal of uncertainty here, that our knowledge about the potential performance of countries with flexible versus fixed exchange rates is limited. And by knowledge I mean empirical not theoretical. We understand very well how exchange rates work but my reading of the literature is that we are not very good at quantifying these effects.

Below is a list of random and unconnected empirical facts that suggest that the Euro itself might not have caused as much damage as the comparison between Thailand and Indonesia to Ireland and Greece might suggest.

1. Comparing across countries with different GDP per capita is tricky. It is hard to imagine Ireland to grow at rates similar to Thailand and Indonesia at any point in time after 2008 given that Irish GDP per capita is as high as that of Germany or the US (in 2012 and according to the IMF GDP per capita in Ireland is higher than in Germany; In contrast, in 1996 the GDP per capita of Indonesia was less than 10% of the US level). Finding a better comparison is difficult. Very few advanced economies adopt fixed exchange rates or go through large devaluations. But we can still find some anecdotal evidence.

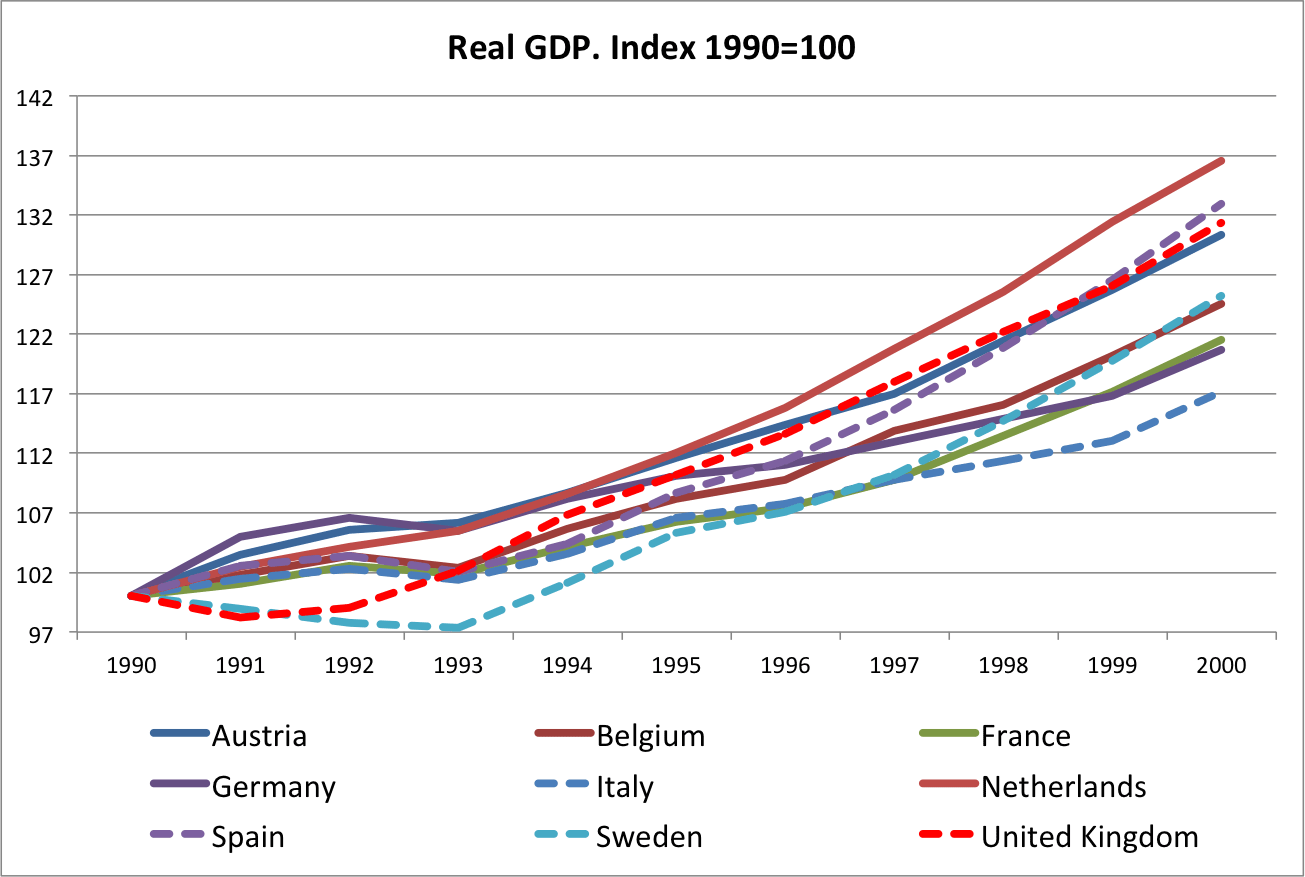

2. The European countries were in a crisis also during the years 1991-1993. A crisis that brought their system of fixed exchange rates down. Some countries abandoned the fixed exchange rate and devalued while others stayed. This is the closest we have to an experiment of countries leaving the Euro area (yes, the experiment is not perfect, the crisis was much smaller, but it can help us understand the role of exchange rates). Below is a chart with the path of GDP that different countries followed.

(click to enlarge)

There are 9 countries in the chart. Some of them let their currencies be devalued (and a subset of those completely left the system). These are represented by dotted lines. The others stayed within the system and their value of their currencies remained fixed to each other (they are represented by the solid line). The chart reveals that there is no clear pattern between the two groups. Growth differences do not seem to correlate well with the behavior of exchange rates. It might be that only those who devalue “had to devalue”, possibly, but what is remarkable is how similar the growth patterns are for all countries.

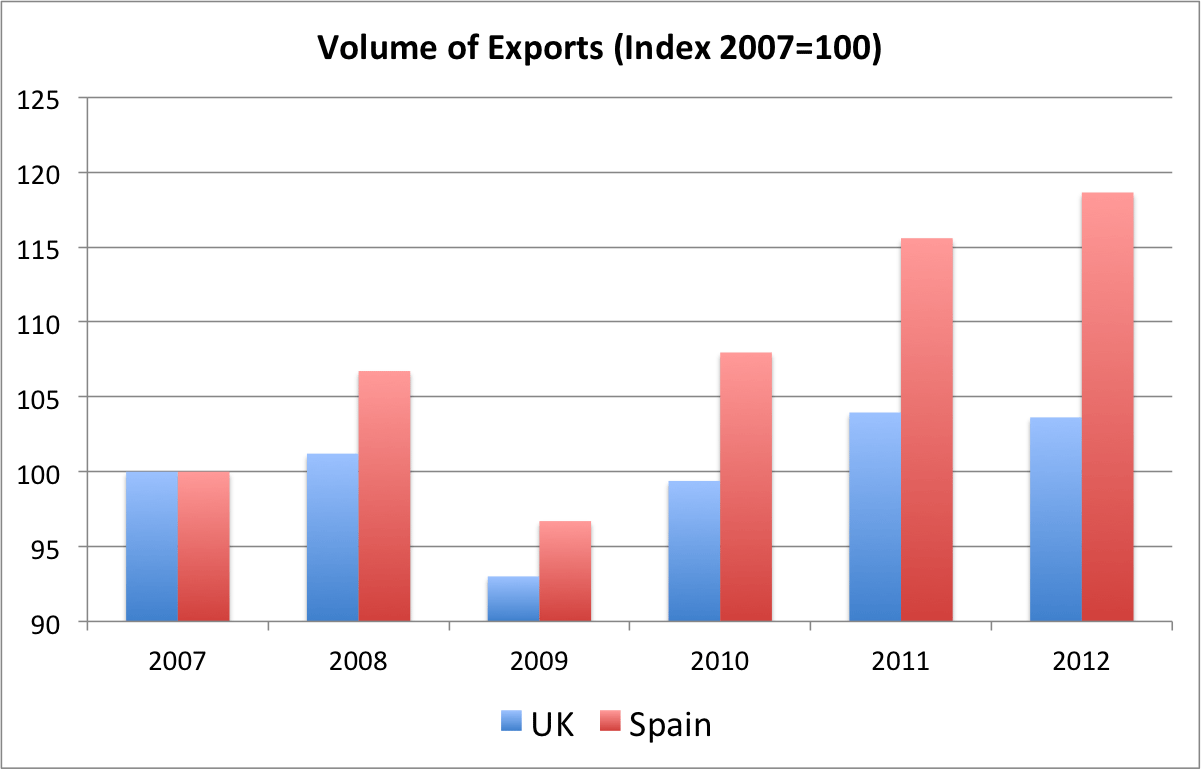

3. Here is a second piece of evidence from the most recent crisis. Both Spain and the UK have suffered the consequences of the 2008 financial crisis. Both are large economies that before the crisis saw real estate prices booming. But once the crisis started one them let its currency depreciate (the UK) by about 30% relative to the Euro while the other (Spain) was stuck with a currency that it did not own. The theory says that the UK should have benefited from a strong boost in exports as a result of the depreciation of its currency. Below is a comparison of exports (real) after the crisis erupted at the end of 2007.

(click to enlarge)

Contrary to our priors, Spanish exports have grown faster than UK exports. So it seems that the depreciation did not help that much the UK (or the lack of control of your currency did not hurt Spain that much either).

4. So maybe exports in Spain did not behave that badly but isn’t unemployment extremely high, at levels that are as high as during the Great Depression in the US? Yes, they are, but unemployment rates in Spain were also extremely high when Spain had a currency (the peseta).

|

Annual

Employment Growth

|

||

| Growth | Rate | |

| 1980-1998 | 0.81 | 18.87 |

| 1999-2012 | 1.45 | 14.00 |

None of the above facts provide a perfect test of what life without the Euro would have been for some of the Euro countries but they, at a minimum, question the conclusion that the recent financial crisis has clearly proven that the creation of a single currency in Europe was a really bad idea. For some of these countries life is hard and volatile (with or without the Euro).

- Bulenox: Get 45% to 91% OFF ... Use Discount Code: UNO

- Risk Our Money Not Yours | Get 50% to 90% OFF ... Use Discount Code: MMBVBKSM

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply