My colleague, Fernando Martin, has an interesting chart that plots the real per capita GDP of five industrialized countries since 1991:

(click to enlarge)

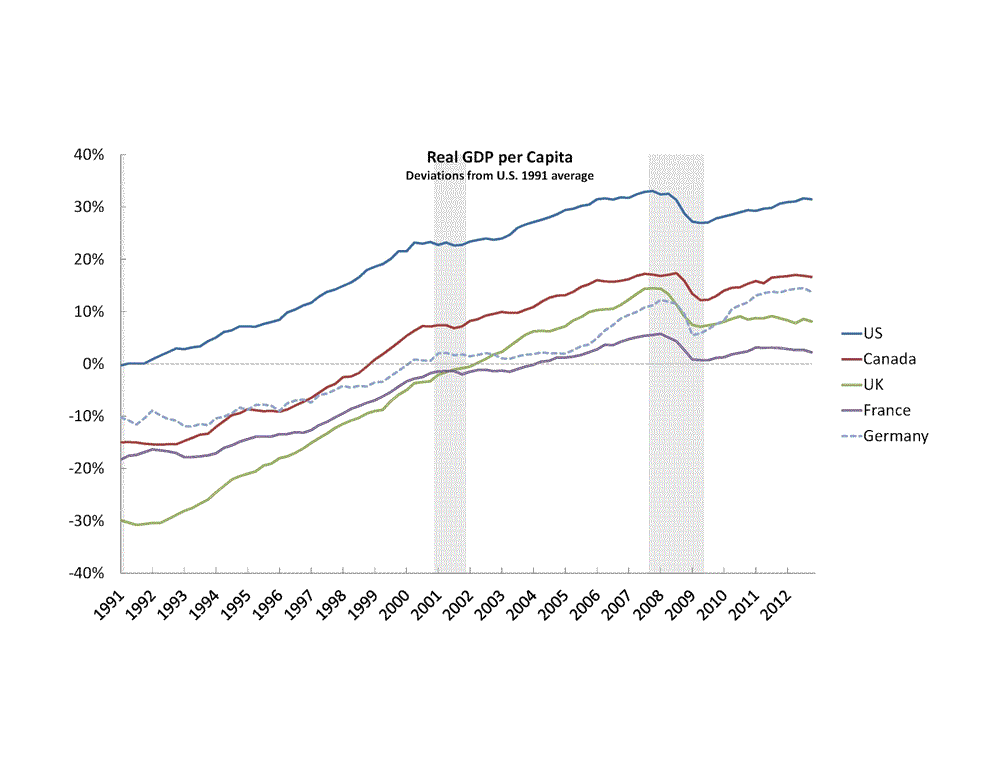

The data above are expressed as percentage deviations from the U.S. level in 1991, with the initial position calculated using PPP converted GDP per capita from the Penn World Tables. Thus, in 1991, the U.K. is estimated to have had a real per capita income that was 30% lower than the U.S. Germany’s real per capita income was only 10% lower than the U.S. in 1991, and so on.

Each of these countries experienced a similar decline in output during the most recent recession. But only Germany has the recession been “temporary.” That is, only in Germany has real per capita income returned to its pre-recession trend. The other four countries exhibit persistent “output gaps”–their real per capita income remains below their respective pre-recession trends. Ah, Germany. All hail that Teutonic economic juggernaut.

But just hold on a second. While it is true that Germany appears to have weathered the economic storm better than others, it seems to have done so at considerable cost.

From 1991-2007, German real per capita income grew at a paltry 1.3% per annum. Compare this to the U.S. (2.1%), Canada (2.2%), France (1.6%), and the U.K. (2.9%). These are huge differences in long-run growth rates. In particular, while German income was only 10% below that of the U.S. in 1991, it is presently about 18% below U.S. income. That’s called falling behind (albeit, at a steady pace).

And yes, the U.K. presently looks ugly. But it looks considerably less ugly when we take into account the growth record. In 1991, real per capita income in the U.K. was 20% below that of Germany. Just prior to the recession, the U.K. had just about closed that gap. Of course, things have not looked good for the U.K. snce then.

Fernando and I are also led to speculate on the role played by monetary policy for shaping the economic recoveries of these nations. France and Germany, as members of the EMU, operated under the same monetary policy–and yet, their recovery dynamics look very different. Also, since inflation was pretty low over this sample period, real and nominal GDP look practically the same. So for the NGDP targeters out there: it appears that German NGDP is back on target, but not French NGDP. Care to comment?

Moreover, out of this set of countries, only the U.K. has experienced a significant rise in inflation (and hence, NGDP). It’s not exactly clear from this data how this “looser” monetary policy has contributed to a more rapid recovery dynamic (although, as usual, we have to be careful because many other things are happening, especially on the fiscal front).

- Bulenox: Get 45% to 91% OFF ... Use Discount Code: UNO

- Risk Our Money Not Yours | Get 50% to 90% OFF ... Use Discount Code: MMBVBKSM

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

What you have totally overlooked is the ~2 Trillion USD Germany spent on its unification.

Without this “national project” Germany would have easily eclipsed US and UK growth.

Max