Regarding the never-ending debate on the the currency wars, Greg Ip adds an important point:

..these conventional and unconventional actions work the same way: by lowering the real (inflation-adjusted) interest rate, they stimulate domestic demand and consumption…This pushes the exchange rate down in two ways. First, a lower interest rate reduces a currency’s relative expected return…Second, higher inflation reduces a currency’s real value and thus ought to lead to depreciation. But higher inflation also erodes the competitive benefit of the lower exchange rate, offsetting any positive impact on trade.

If this were the end of the story, the currency warriors would have a point. But it isn’t. The whole point of lowering real interest rates is to stimulate consumption and investment which ordinarily leads to higher, not lower, imports. If this is done in conjunction with looser fiscal policy (as is now the case in Japan), the boost to imports is even stronger. Thus, QE’s impact on its trading partners may be positive or negative..The point is that this is not a zero sum game; QE raises a country’s GDP by more than any improvement in the trade balance.

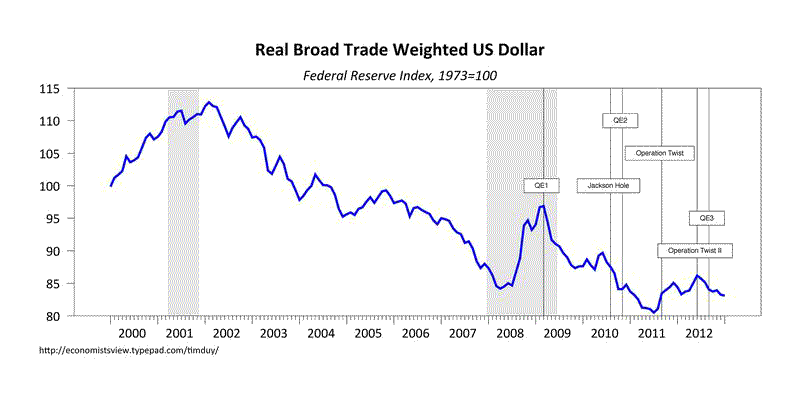

The Federal Reserve is generally considered the first offender in the currency wars, yet it is often forgotten that the vast majority of the Dollar’s real depreciation occurred prior to the recession:

(click to enlarge)

To be sure the Dollar took a hit after the first round of quantitative easing, but that was a positive policy outcome for all as the calming of financial markets eased the rush to the safety of the US currency. On average, since the beginning of 2008 there has been little change in the real value of the Dollar, despite the massive expansion of the Fed’s balance sheet.

Also note that by stabilizing the US (and global economies), the Fed contributed to a stabilization of the US current account balance:

(click to enlarge)

All of the improvement in the current account balance occurred prior to the Fed’s expansion of the balance sheet, largely due to collapsing global trade. And the subsequent period was one of generally declining real government spending; a more stimulative policy would likely have supported more imports such that trade remained an even greater drag on the economy.

In short, the Federal Reserve did not pursue a “beggar-thy-neighbor” policy. The Federal Reserve actually stabilized the Dollar’s value, calmed global financial markets, made a positive contribution to international trade, and stabilized the US current account balance. Sounds like a net win across the board.

Separately, I see that Japanese policymakers continue to make the same mistake of needlessly antagonizing their trading partners. From Bloomberg:

The yen fell after Kazumasa Iwata, a potential candidate to become the next central bank head, signaled the currency has scope to depreciate further and data showed Japan’s gross domestic unexpectedly shrank…Iwata, a former deputy governor at the BOJ, said in a statement the price goal can’t be reached without a correction in the yen’s strength. The yen at 90 to 100 per dollar marks a return to equilibrium, he said.

While there are voices in Japan arguing that the Yen’s depreciation is simply a side-effect of domestic policies, it is tough for other nations to buy that story when prominent current, former and potentially future policymakers repeatedly put numbers on the appropriate value of the Yen. They would be better off with some noncommittal statement about currency values being driven by economic fundamentals, with only one spokesperson for the currency. Trying to convince Japanese policymakers to not talk about the value of the Yen, however, is generally about as productive as trying to convince the sky not to be blue.

Leave a Reply