Bernstein’s Pierre Ferragu is upgrading Blackberry (NASDAQ:BBRY) to Outperform from Market Perform with a $22/share price target.

– They believe Blackberry should trade in the $20-25 range once a decent launch for Blackberry 10 and a stabilised trajectory for FY2014 are priced in.

Bernstein upgrades Blackberry to outperform today as they believe BB10 is set for a strong launch. Even if the long term prospects for the platform are very uncertain, the firm believes all is in place for Blackberry 10 to enjoy a great debut. They see four reasons to model a launch well above current expectations.

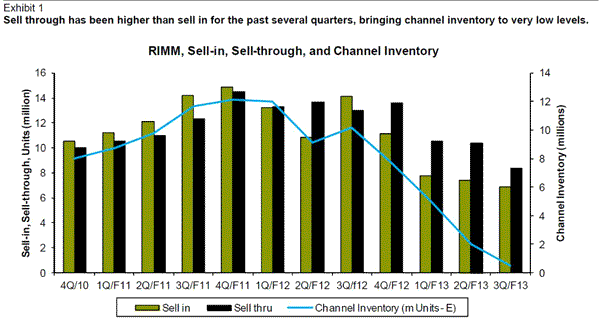

1 – Blackberry has drained channel inventories over the last 12 months and is in a very strong position to start shipping its new devices. Channel inventories came down by over 10m units over the last 12 months, which means most distributors and operators will take on significant initial orders (Exhibit 1)

2 – Blackberry 10 will propel up device gross margins. Bernstein believes the company currently sells high end devices at negative gross margins. As these devices are replaced by positive margin Blackberry 10 ones, Blackberry’s P&L should swing back into the black in 1QF14. They are at this stage convinced initial Blackberry 10 shipments will carry gross margins in the region of 30%.

3 – The Blackberry 10 launch is supported by most operators. In their recent discussions with operators the firm noted a very broad support, with operators willing to give the platform a good push.

4 – Initial Corporate demand will be strong. Bernstein recognises rapid share losses for blackberry in corporate, as “Bring Your Own Device” becomes the norm, but the brand still benefits from a significant user base equipped with ageing smartphones. They have anecdotal evidence that a number of corporate clients have been waiting for Blackberry 10 to refresh their installed base, which will support shipments meaningfully in the first months of the launch. If only 10% of Blackberry’s 30m corporate users refresh their phone within the first 6 months of the launch, this would represent ~3m units alone.

The strength of this launch is overlooked by investors, creating strong opportunity to buy Blackberry.

– Bernstein conservatively expects shipment of 1m units for January and February, in the current quarter, and thereafter 1m units per month in March to May, generating 3m units of BB10 sales in the first fiscal quarter of 2014. As a reference, the current sell through run rate of Blackberry is close to 3m units a month.

– They assume ~$550 ASP and 30% gross margins for BB10 devices, which is in line with communicated selling prices and their channel checks. This would drive gross profits 24% above current expectations for 4QF13, 32% above expectations for 1QF14.

There is no bear case related to the evolution of Service revenues.

– For the last two years, Blackberry’s service revenues have remained stable, in the region of $1bn a quarter, driven by a stabilising user base and resilient ARPU.

– It is well understood that the migration to Blackberry 10 will create some pressure on Service revenues, most likely for some consumer segments. Bernstein models an average service revenue per BB10 user 50% below the current average. On that basis they see two potential scenarios, and the stock working well for both!

– Either Blackberry 10 is a slow launch, driving limited upside. In that case, older contracts will continue to form the vast majority of Blackberry’s user base. Blackberry will continue to benefit from the service revenue cushion. In that scenario, Blackberry’s business model is much more resilient than consensus expectations imply.

– Or Blackberry 10 is a success, and in that case, there is a risk that service revenues come under meaningful pressure. The irony is that if Blackberry 10 is a success, some pressure on Service revenues would be the least of Bernstein’s concerns and more than compensated by a recovery in the device business.

Notablecalls: Ferragu has been a major bear in Blackberry since ’10 with a couple of stints on the Market Perform side along the way. Now he is making a rather significant call saying the stock should trade ~100% higher. This will not go unnoticed.

His views regarding the Services side potentially ending in a win-win situation are also quite interesting and should work to calm investor fears.

With the stock down 5 pts from the $18+ highs I suspect a strong case for a long trade can be made here. Potential 10%+ move in the cards.

- Bulenox: Get 45% to 91% OFF ... Use Discount Code: UNO

- Risk Our Money Not Yours | Get 50% to 90% OFF ... Use Discount Code: MMBVBKSM

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply