Developed economies are implementing massive fiscal stimulus packages. Should emerging economies? This column warns them that fiscal multipliers are not certain, financing budget deficits will not be easy, the risk of default looms, and central bank independence may be eroded.

What began as the subprime crisis in the US during the summer of 2007 and morphed into a global financial crisis in the other advanced economies of the “North” has led to unprecedented fiscal stimulus efforts worldwide. The “North” – including the US, Ireland, the UK, Spain, Switzerland, and Japan – needed stimulus because banking crises are usually accompanied by severe and protracted recessions and rising unemployment. The “South” sought to stimulate domestic demand by fiscal means in the face of collapsing exports, as available financing from global capital markets dried up in a “sudden stop” as predicted by Guillermo Calvo.

Despite the enthusiasm for such stimulus in some policy circles, authorities in emerging market economies should be cautious. Countries with a history of fiscal excesses that compromise central bank independence do not have the luxury of smoothing the business cycle.

Emerging markets on the eve of the sub-prime shock

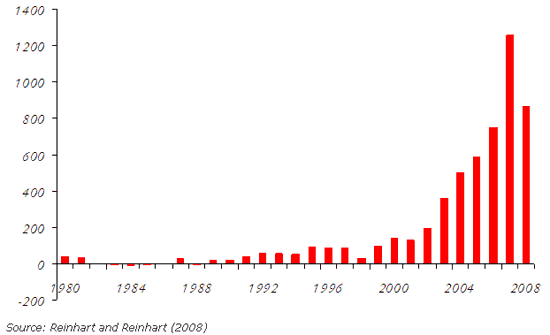

Fortunately for many emerging markets, this synchronous export and financing shock from the North came after they had built vast war chests of international reserves during the “bonanza” years (Figure 1). Emerging market reserve managers learned the lesson of the Asian Crisis – when times get tough, the advanced economies look inward, so emerging markets’ first line of defence must be their own resources. In the fat years, commodity prices were booming, growth in the North was buoyant, international interest rates were low and stable, and international capital was plentiful. In such an environment, fiscal positions in many emerging markets improved markedly. Public debt levels were stabilised or even reduced, and many countries substituted public external debt with domestic debt and lengthened the maturities of their outstanding debt.

Figure 1. Accumulation of international reserves by emerging market and developing economies, 1980-2008, billions of US dollars

If the adverse shock to the North had been a short-lived reduction in financing, as many observers believed at the time, the fiscal consolidation and reserve build up would have put emerging markets in a good position to cope with the shock. A combination of currency depreciation (now possible owing to more flexible exchange rate arrangements) and some international reserve sales would seem to fit the bill. In addition, a short-lived fiscal response that entailed increasing government expenditures for a limited period of time did not seem to carry substantive risks to debt sustainability.

Such optimism that fiscal policy could be used to de-couple the South from the North is misplaced in three important dimensions.

- Fiscal finances and external accounts were not as healthy as they appeared in 2007, as explained by the aptly titled All That Glitters May Not Be Gold: Assessing Latin America’s Recent Macroeconomic Performance from the Inter-American Bank Development Bank (2008).

The commodity-price boom had papered over many cracks in fiscal accounts. Those governments’ ability to ramp up spending will be impaired by the shaky base they are building upon.

- Funding fiscal deficits with domestic debt is neither new nor riskless.

As Reinhart and Rogoff (2008) show, governments often default on such domestic debts, either explicitly or through unexpectedly high inflation. Furthermore, private debts (both domestic and external) had also been rising markedly. As crisis after crisis has consistently shown, private debts turn out to be contingent government liabilities.

- It is now two years since the onset of the crisis, and the effects continue to linger (even if recovery is at hand).

Plainly, this episode hardly classifies as a fleeting shock, as far as market participants, households, or policymakers are concerned. “Temporary” stimulus might persist so as to put pressure on funding costs over time.

Response to the crisis: Fiscal stimulus, North and South

Led by the US, both advanced and emerging economies have passed fiscal stimulus packages in various guises and magnitudes. By January 2009, the Global Economic Monitor, published by the Institute for International Finance, detailed the packages either adopted or planned in about twenty advanced and emerging market economies, including China, Korea, Mexico, and Saudi Arabia. Less than two months later, the list of countries had expanded to include Russia and Turkey, among others (Prasad and Sorkin 2009). The IMF, both famous and infamous for advocating fiscal austerity packages in response to financial crises around the globe since its inception in 1945, began to advocate a “possible strategy whereby fiscal policy can foster the resumption of normal economic growth while maintaining public sector solvency” (Cottarelli 2009).

To be sure, avoiding the acute fiscal policy pro-cyclicality that has plagued most emerging markets for decades is, indeed, progress. As Kaminsky, Reinhart, and Vegh (2003) document, during 1965-2003 the most prevalent pattern in emerging markets during recessions (in contrast to their OECD counterparts) was sharp reductions in real discretionary fiscal spending. It is difficult to imagine that this would not help account for the greater volatility evident in emerging market output.

Fashions and fundamentals

Fashions are hard to resist, and it is now fashionable in much of the North to rely on a fiscal engine of growth. Boosting spending in emerging economies, however, at a time in which revenues are contracting or, in many cases, collapsing for an uncertain period of time is a more complicated matter.¹ Policymakers in emerging market economies would do well to keep three risks in mind.

1. Fiscal multipliers: North and South

Although there is little consensus in academic and policy circles on their magnitudes, the discussion of fiscal multipliers in most OECD countries is at least informed by existing analytical and empirical studies. For emerging markets, however, a comparable literature does not exist. Thus, any statement about fiscal multipliers for emerging markets (and developing countries) as a class has to be interpreted with care.

In this regard, there has been especially timely recent work by Ilzetzki, Mendoza, and Vegh (2009), who calculate such multipliers for advanced high-income economies, emerging markets (middle income), and developing countries (low income) using quarterly data. Their analysis suggests that:

- the fiscal multiplier on impact is larger for developing and emerging market countries than for the advanced high-income countries;

- the opposite is true for the peak multiplier;

- and the cumulative multipliers are far smaller for emerging markets than for advanced economies, as the positive impact of fiscal spending on GDP dies out fairly quickly.

2. Emerging markets and global crowding out

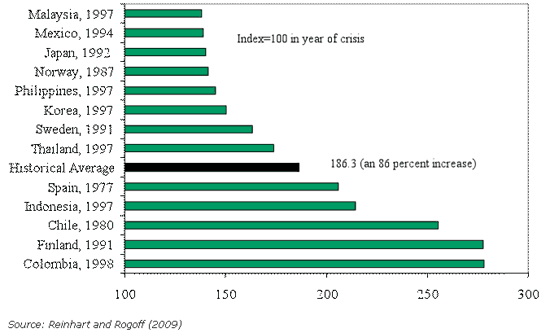

Figure 2 highlights that public debt typically explodes in the years following a systemic financial crisis. On average, public debt nearly doubles three years after the crisis. Recessions lead to major revenue losses and fiscal spending expands, as the bailout of the banking sector proves costly and stimulus packages find favour. With severe banking crises, deep recessions, or a combination of the two in the world’s largest economies simultaneously, international financing for emerging markets is likely to be far scarcer than during the bonanza years before 2007. Financing budget deficits will not be easy or cheap.

Figure 2. Cumulative increase in real public debt in the three years following the banking crisis

Notes: Each banking crisis episode is identified by country and the beginning year of the crisis. Only major (systemic) banking crisis episodes are included, subject to data limitations. The historical average reported does not include ongoing crisis episodes, which are omitted altogether, as these crises begin in 2007 or later, and debt stock comparison here is with three years after the beginning of the banking crisis.

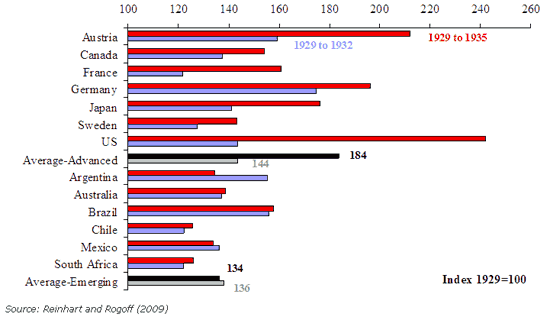

It is noteworthy that the last time the world experienced a crisis of this proportion (the Great Depression), governments in the advanced economies were able to continue borrowing (Figure 3), as recovery remained elusive for nearly a decade. Debt rises by 44% in the first three years and by another 40% during the next three years. By contrast, the public debt of emerging markets remained frozen after the third year. This was not the result of rebounding revenues balancing the budget – in a number of cases it was the result of sovereign defaults.

Figure 3. Cumulative increase in real public debt three and six years following the onset of the Great Depression in 1929: Selected countries

Notes: The beginning year of the banking crises range from 1929 to 1931. Australia and Canada did not have a systemic banking crisis but are included for comparison purposes, as both also suffered severe and protracted economic contractions. The year 1929 marks the peak in world output and, hence, is used as the marker for the beginning of the depression episode.

3. Above all – remember debt intolerance!

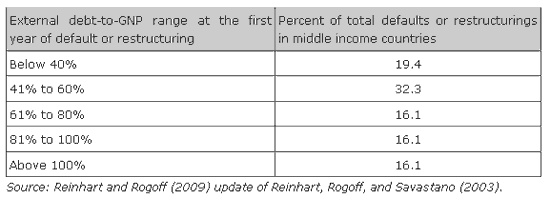

Historically, emerging market defaults have taken place at levels of debt that would appear to be safe and even conservative by advanced economy standards. The defaults of Mexico in 1982 and Argentina in 2001 were not exceptions. Table 1 shows that external debt exceeded 100% of GNP in only 16% of the default or restructuring episodes, that more than one-half of all defaults occurred at levels below 60% – which would have satisfied the Maastricht criteria – and that defaults took place against debt levels that were below 40% of GNP in nearly 20% of the cases. In effect, the external debt-to-GNP thresholds reported in Table 1 are biased upwards because the debt-to-GNP ratios corresponding to the year of the credit event are driven up by the real exchange rate depreciation that typically accompanies the event. Real exchange rate depreciation typically accompanies a default, of course, as locals and foreign investors flee the currency. The fiscal “space” to implement ambitious stimulus plans in emerging markets is far more limited than that of advanced economies – not that policymakers in the latter may underestimating these constraints as well.

Table 1. External debt at the time of default: Frequency distribution, 1970-2008

Final reflections

Taken together, these risks have broader implications than for fiscal policy alone – these are risks to macroeconomic policy at large, especially in emerging market countries where central bank independence is of recent vintage. Many of these countries have an unfortunate track record in which fiscal officials having trouble funding large deficits turn to the central bank for help. As a consequence, financing deficits with money creation has played a major role in shaping the path of monetary policy, the exchange rate, and inflation. Getting off that treadmill and gaining credibility has been a long and difficult process. Losing that credibility to a fashion for fiscal stimulus can happen fairly quickly. A more cautious alternative is to make sure that fiscal policy does not tend to the excesses that ultimately could threaten the pursuit of price stability. It is enough of a victory that fiscal policy is no longer pro-cyclical.

References

•Cottarelli, Carlo (2009). “Paying the Piper” Finance and Development, (Washington, DC: International Monetary Fund, March).

•Ilzetzki, Ethan, Enrique Mendoza, and Carlos Vegh (2009). “How big (small) are fiscal multipliers?” Mimeograph. University of Maryland College Park

•Institute for International Finance (2009). Global Economic Monitor (Washington, DC: Institute for International Finance, January).

•Inter-American Development Bank (2008). All That Glitters May Not Be Gold: Assessing Latin America’s Recent Macroeconomic Performance (Washington, DC: Inter-American Development Bank, March).

•Kaminsky, Graciela L., Carmen M. Reinhart and Carlos A.Végh (2004). “When It Rains, It Pours: Procyclical Capital Flows and Policies” in Mark Gertler and Kenneth S. Rogoff, eds. NBER Macroeconomics Annual 2004. Cambridge, Mass: MIT Press, 11-53

•Prasad, Eswar, and Isaac Sorkin (2009). “Assessing the G-20 Economic Stimulus Plans: A Deeper Look” Mimeograph. (Washington, DC: Brookings Institution, March).

•Reinhart, Carmen M. and Vincent R. Reinhart. (2008). “Capital Inflows and Reserve Accumulation: The Recent Evidence”, NBER Working Paper 13842, March.

•Reinhart, Carmen M., and Kenneth S. Rogoff (2008). “The Forgotten History of Domestic Debt”, NBER Working Paper 13946, April.

•Reinhart, Carmen M., and Kenneth S. Rogoff (2009). This Time It’s Different: Eight Centuries of Financial Folly Forthcoming (Princeton: Princeton University Press).

1 This is not intended to underestimate the difficulty and (usually) controversy of undertaking any kind of change in fiscal policy in the advanced economies.

![]()

- Bulenox: Get 45% to 91% OFF ... Use Discount Code: UNO

- Risk Our Money Not Yours | Get 50% to 90% OFF ... Use Discount Code: MMBVBKSM

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply