Joe Gagnon says no:

For more than two years, the Fed has dragged its feet and resisted the obvious need for more aggressive action…

…A large majority of the committee projects [pdf] that inflation will be below target over the next two and a half years. If they assign any weight to their employment objective, they should be willing to accept inflation at least modestly above target in order to get a better outcome on employment.

Considering that more aggressive action has not been taken, monetary policymakers appear to disagree. The willingness to accept the current state of affairs suggests that fear of the 1970’s remains alive and well on Constitution Ave. The risks of inflation simply outweigh the expected benefits of additional easing, at least from the point of view of Federal Reserve Chairman Ben Bernanke. Earlier this spring, Brad DeLong made an insightful observation about the real parallels with the 1970s:

In my view, there is an odd symmetry between the Federal Reserve of today and the Federal Reserve of the 1970s. The Federal Reserve of today does not take effective steps to reduce unemployment because it thinks any risk of sustained inflation above 2%/year is unacceptable. The Federal Reserve of the 1970s did not take effective steps to control inflation because it thought sustained unemployment above 7% was unacceptable. Since then, the Federal Reserve of the 1970s–Arthur Burns and G. William Miller–have been censured, condemned, scorned, and damned for their failure to understand the situation they were in and their proper objective function.

The Fed is really making the same mistake as they did in the 1970s. Not so says David Altig, who does not see so much of a conflict between the Fed’s objective and the actual outcomes:

That complaint is not really about the inflation part of the mandate, but the employment/growth part of it. But if you are willing to accept that employment growth remains on a pace of 150,000 jobs per month—and I see no clear evidence to the contrary—it is not at all obvious that the pace of the recovery is inconsistent with the FOMC’s view of achieving its dual mandate…

…And I am certainly begging the important issues. Would the economy have achieved even the somewhat unspectacular pace of 2 percent GDP growth, 150,000 jobs per month, and average inflation near the long-run objective absent large-scale asset purchases (“QE2”), forward guidance (statements indicating that policy rates are expected to be exceptionally low through at least late 2014), and maturity extension programs (“Operation Twist”)? Does “appropriate policy” imply that more must be done to achieve even the modest progress in the unemployment rate implied in my calculations above?

Mark Thoma replies:

It sounds as though the Fed has given up — we’ve done all that we can, there’s nothing more we can do, so we won’t even try — and we’re not about to risk even the tiniest bit of inflation to find out if we are wrong…

Mark’s idea that the Fed has “given up” is not sufficiently appreciated. Altig’s calculations make the important assumption that the labor force participation rate holds at 63.7%. This effectively assumes that none of the decline in the labor force participation is cyclical. Instead, it is all structural:

(click to enlarge)

Should the Fed take the labor force participation rate as exogenous or endogenous? If they take it as exogenous, then policymakers have effectively “given up” on the recovery. Any cyclical decline in the labor force participation rate becomes structural over time as skill loss increasingly excludes those displaced by the recession from reentering the labor force.

This is similar to the debate over the current level of potential GDP. Once policymakers started to believe (on the basis of an HP filter, of all things) that the economy is operating at potential, rather than well-below potential, then they would start behaving as if the economy was in fact at potential, setting policy and managing the economy along the suboptimal level. This sends signals to economic agents about the expected growth in output (or nominal GDP), who adjust their behavior accordingly. The cyclical declines becomes structural. In other words, a shift in potential GDP becomes a self-fulfilling prophecy.

Should the Fed take all “structural variables” as exogenous? For all the derision heaped upon former Federal Reserve Chairman Alan Greenspan, consider the long-gone 1990s. Greenspan believed that accelerating productivity growth meant the economy could run at a higher growth rate than previously believed. Suppose Greenspan had not reached this conclusion. Would unemployment have fallen as low as it did? More importantly, we told a story back then, and it went like this: Low unemployment was forcing firms to reach deeper and deeper into the labor pool to the point where they had to start actively training new employees. They no longer had the luxury of cherry-picking only the obviously skilled employees; they had to bring unskilled labor up to speed. This process is human capital deepening, which should have a positive impact on potential GDP growth. A benefit that would have been lost if Greenspan pulled the plug on economy sooner (the same holds true of the physical capital deepening of the time).

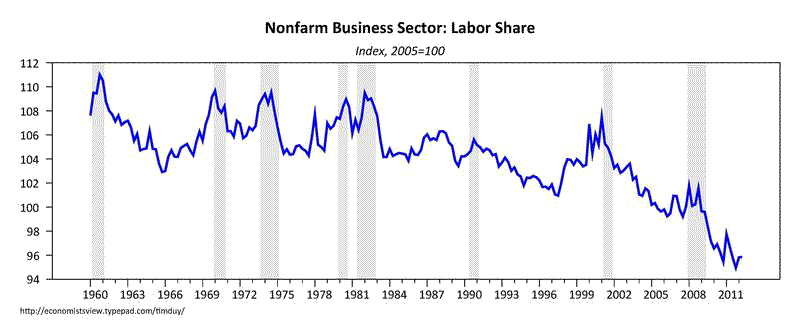

And did that process of capital deepening make any difference? Running the economy red hot had the benefit of shifting the share of output in favor of labor during the 1990s:

(click to enlarge)

Of course, inflation did accelerate to something closer to 2.5% over that period. Was that such a high price to pay to lift up those at the lower end of the socioeconomic ladder? Maybe, just maybe, the Fed’s newly minted 2% target is simply too low. Maybe, just maybe, if we run the economy a little on the red side of hot the supply response will be stronger than the Fed believes – that the long-run path of the economy will prove to be just a little more endogenous than the Fed is willing to accept. Maybe, just maybe, the Fed’s obsession with disinflation (and don’t let the Fed fool you – they used the most recent recession to achieve another round of opportunistic disinflation) is contributing to stagnant to falling standards of living for much of the country.

Note that I am not suggesting the Fed should take all structural variables as endogenous, just that we don’t necessarily have a complete understanding of what is endogenous. In essence, if the Fed bases policy on 63.7% labor force participation as an exogenous variable, ignoring any endogenous response, the economy will proceed on a path that is very well suboptimal. But downward nominal wage rigidities and fear of inflation above 2% will prevent the Fed from exploring any other possibilities.

Bottom Line: Monetary policy might have a bigger impact on shaping the underlying growth rate of the economy than policymakers believe. Some of what they think is exogenous may be at least in part endogenous. Ultimately, within a certain margin, we will get the economy the Fed wants us to get. And right now we are getting the economy that is defined by central bankers living in mortal fear of any inflation rate greater than 2%. With the exception of a few policymakers, the cost of 2.5% inflation far exceeds the possibility of learning to what degree the underlying structure of the economy is exogenous or endogenous.

I increasingly believe that the Fed made a massive policy error in defining their mandate as 2% inflation. I think they believed it would give them more freedom to use new tools by solidifying inflation expectations. Instead, the target has placed policymakers in a straitjacket. It is Bernanke’s cross of gold.

- Bulenox: Get 45% to 91% OFF ... Use Discount Code: UNO

- Risk Our Money Not Yours | Get 50% to 90% OFF ... Use Discount Code: MMBVBKSM

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply