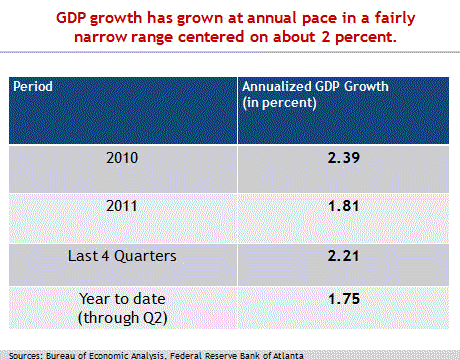

In his last two posts (here and here), economist Tim Duy has done some yeoman work displaying and discussing the economic context of monetary policy decisions past and prospective. Though Wednesday’s self-titled post “Data Dump” focuses on the incoming data as a set-up to the next meeting of the Federal Open Market Committee (FOMC), what strikes me is the consistency of the broad macroeconomic outcomes over the course of the recovery. Gross domestic product (GDP) growth has pretty clearly clocked in at about 2 percent…

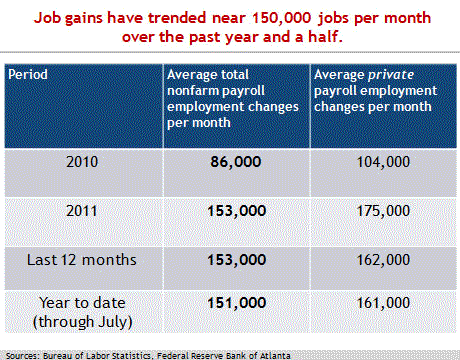

…and, looking through the quarterly ups and downs, payroll employment growth has clearly trended near 150,000 jobs per month after a slower start in 2010:

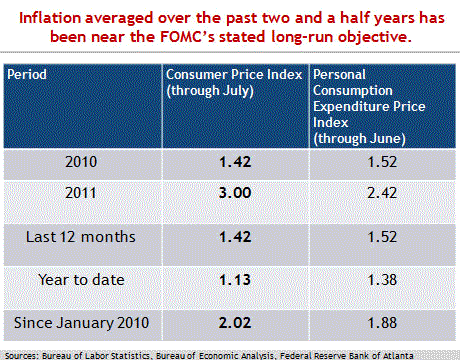

The inflation picture shows more variation…

…but in my view, that sort of variation is why it makes sense to think in terms of medium-term performance. “Medium-term” is more a measure of art than science, and I would concede the point that the recovery as a whole would be on the shorter end of that time frame. Suffice it to say that the pace of price-level growth over the past two and a half years wouldn’t contradict the presumption that inflation is pretty close to the FOMC’s stated longer-run objective.

Duy looks at this performance and sees pretty clear evidence of failure:

The economy continues to settle into a path that is not consistent with either part of the Fed’s dual mandate. Moreover, there are very real downside risks to even a tepid outlook…

This is frustrating. What in the world is the point of making a big claim to affirm the nature of the dual mandate and then subsequently ignore any forecasts that indicate you have no faith the elements of the dual mandate will be met anytime soon?

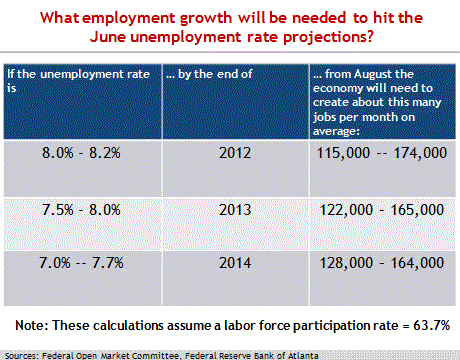

That complaint is not really about the inflation part of the mandate, but the employment/growth part of it. But if you are willing to accept that employment growth remains on a pace of 150,000 jobs per month—and I see no clear evidence to the contrary—it is not at all obvious that the pace of the recovery is inconsistent with the FOMC’s view of achieving its dual mandate. Here, for example, are the central tendency ranges of the unemployment rate projections from the FOMC’s June Summary of Economic Projections (SEP) and the employment growth that would be required to meet those objectives (with some important assumptions, such as the labor force participation rate remaining at the current level).

Here is the important statement of conditionality, as described in the SEP document:

The charts show actual values and projections for three economic variables [GDP growth, the unemployment rate, and PCE inflation] based on FOMC participants’ individual assessments of appropriate monetary policy.

Under appropriate policy—which pretty clearly means mandate-consistent outcomes—the majority of FOMC participants don’t seem to think that the unemployment rate will improve that quickly. And, to my point, it is not clear that the trend in payroll employment is inconsistent with that pace of improvement.

Of course, individual contributors to the SEP may have different assumptions about things like the labor force participation rate. More importantly, the SEP is silent on what, in each contributor’s view, constitutes “appropriate policy.”

And I am certainly begging the important issues. Would the economy have achieved even the somewhat unspectacular pace of 2 percent GDP growth, 150,000 jobs per month, and average inflation near the long-run objective absent large-scale asset purchases (“QE2”), forward guidance (statements indicating that policy rates are expected to be exceptionally low through at least late 2014), and maturity extension programs (“Operation Twist”)? Does “appropriate policy” imply that more must be done to achieve even the modest progress in the unemployment rate implied in my calculations above? And could we have (looking backward) or can we (looking forward) do even better with an even more aggressive approach, as many Fed critics argue?

Good questions, those.

- Bulenox: Get 45% to 91% OFF ... Use Discount Code: UNO

- Risk Our Money Not Yours | Get 50% to 90% OFF ... Use Discount Code: MMBVBKSM

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply