There are some economists who are concerned about future inflation because of the loose, expansionary monetary policy in 2008, e.g. see Brian Wesbury and Bob Stein here, here and here. I don’t think inflation will be a problem, and here’s why:

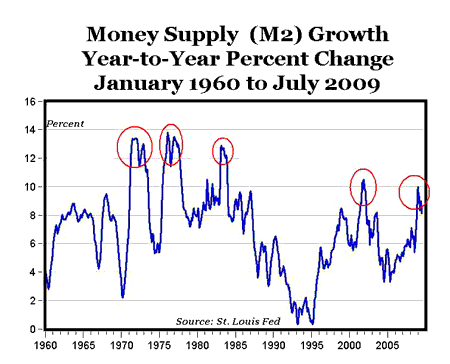

The chart above shows the annual growth rate in the M2 money supply (percent change from the same month in the previous year, data here) monthly from January 1960 to July 2009. Notice that:

1. There was sustained double-digit money growth in two periods in the 1970s, and that is what generated the high double-digit inflation in that decade. There was double-digit M2 growth for 29 consecutive months from March 1971 to July 1973 (and nine straight months above 13%), and then again for 30 consecutive months from July 1975 to December 1977, with a high of almost 14% growth in early 1972 (see chart above).

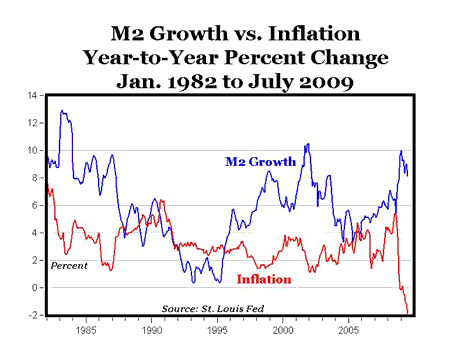

2. There was double-digit M2 growth in 1983, but only for 12 months from January to December of 1983, and this monetary expansion wasn’t enough to cause inflation (see chart below). Inflation never rose above 5% for many years after the double-digit money growth of 1983.

3. There was double-digit money growth in September, November and December of 2001, but inflation in subsequent years never got above 5% (see chart below).

4. The peak monetary expansion of M2 in 2008 was below the peaks in 1971-1972, 1976-1977, 1983 and 2001 (see chart above), and during the recent monetary expansion there has been only one month of double-digit money growth, and that was the peak of 10% in January 2009.

Bottom Line: Without sustained double-digit M2 growth, we won’t have anything close to double-digit inflation. And the historical evidence during the two most recent experiences of double-digit money growth in 1983 and 2001 demonstrates that short periods of double-digit money growth aren’t enough to bring about inflationary pressures. And since recent M2 growth during the “loose” monetary policy of 2008 is actually lower than in 1983 and 2001, there probably can’t be any inflationary pressures that will lead to problems with future inflation. In other words, a single month of double-digit M2 growth in January 2009 isn’t expansionary enough to create inflation.

- Bulenox: Get 45% to 91% OFF ... Use Discount Code: UNO

- Risk Our Money Not Yours | Get 50% to 90% OFF ... Use Discount Code: MMBVBKSM

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply