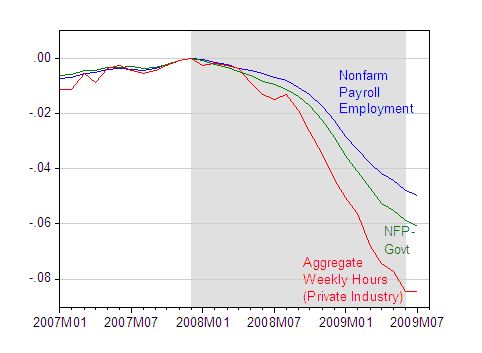

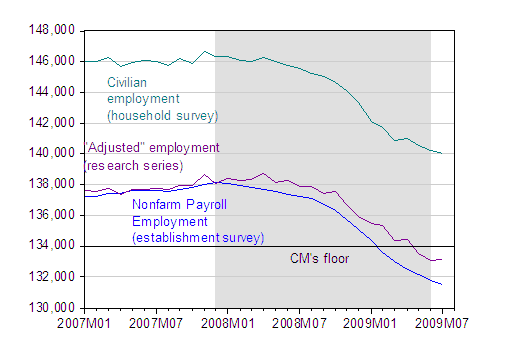

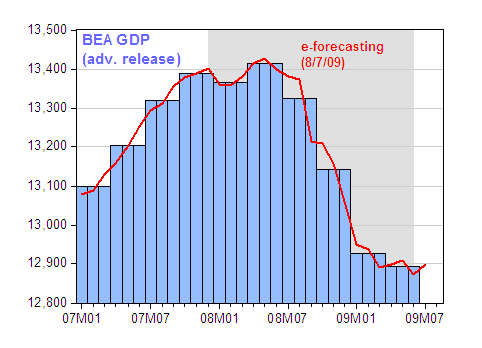

Some observations on the employment situation and other economic indicators: (1) Not only is nonfarm payroll employment slowing its rate of descent, so is private employment; (2) but perhaps more dramatically the decline of aggregate hours halted last month; (3) the rate of decrease has diminished even faster for civilian employment measured by the household survey, and indeed; (4) the household (research) series adjusted to conform to the payroll series is now improving; and (5) a first “estimate” of July GDP supports the case for stabilization of output.

Figure 1: Log nonfarm payroll employment (blue), log private sector nonfarm payroll employment (green) and log aggregate weekly hours for the private sector (red), seasonally adjusted, all normalized to 0 at 2007M12. Gray shading denotes NBER defined recession, assuming end of recession at 2009M06. Source: BLS July release via St. Louis Fed FREDII, NBER author’s calculations.

Figure 2: Nonfarm payroll employment (blue), in thousands, civilian employment (teal), civilian employment adjusted to conform to nonfarm payroll concept (violet). CM’s Floor denotes C. Mulligan’s 10/26/08 forecast floor on NFP. Gray shading denotes NBER defined recession, assuming end of recession at 2009M06. Source: BLS July release via St. Louis Fed FRED II, BLS, NBER, and C. Mulligan.

Figure 3: GDP (blue bars) and GDP monthly estimate from e-forecasting (red line), in billions Ch.2005$. Gray shading denotes NBER defined recession, assuming end of recession at 2009M06. Source: BEA GDP advance 2009Q2 release, e-forecasting release 8/7/09, NBER.

In all cases, the usual caveats apply: the NFP series will undergo revisions (as will the hours series), the household survey based civilian employment series has high variability, and the July GDP estimate will undergo substantial revision as more data comes in. And, of course, one observation does not a trend make.

Employment, Hours, and Estimated Output

- Bulenox: Get 45% to 91% OFF ... Use Discount Code: UNO

- Risk Our Money Not Yours | Get 50% to 90% OFF ... Use Discount Code: MMBVBKSM

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply