The NAR announced that pending home sales rose for the fifth consecutive month.

The Pending Home Sales Index,1 a forward-looking indicator based on contracts signed in June, rose 3.6 percent to 94.6 from an upwardly revised reading of 91.3 in May, and is 6.7 percent above June 2008 when it was 88.7. The last time there were five consecutive monthly gains was in July 2003.

Lawrence Yun, NAR chief economist, said a combination of positive market factors is fueling the gains. “Historically low mortgage interest rates, affordable home prices and large selection are encouraging buyers who’ve been on the sidelines. Activity has been consistently much stronger for lower priced homes,” he said. “Because it may take as long as two months to close on a home after signing a contract, first-time buyers must act fairly soon to take advantage of the $8,000 tax credit because they must close on the sale by November 30.”

On its face, this is a positive report. Housing’s slow recovery seems to be continuing. It’s pretty much a bottom of the market recovery with investors and first time home buyers snapping up homes at severely distressed prices. If you move up the market, you find stagnation and continuing price deterioration.

Does it have legs, though? The tax credit has probably spurred some buying on the margin or it may be carrying a big part ot the market, there’s just no way to tell until it expires. How much is being driven by investors and how much longer will they play? Demand from them can’t be infinite and I suspect that at some point they have to be concerned about how much money to dump into the residential market. And, is the supply actually coming down? Talk continues of significant inventory represented by foreclosed properties not yet listed or defaulted loans that are yet to even enter the foreclosure process.

This chart from the WSJ Real Time Economics blog is an eye opener:

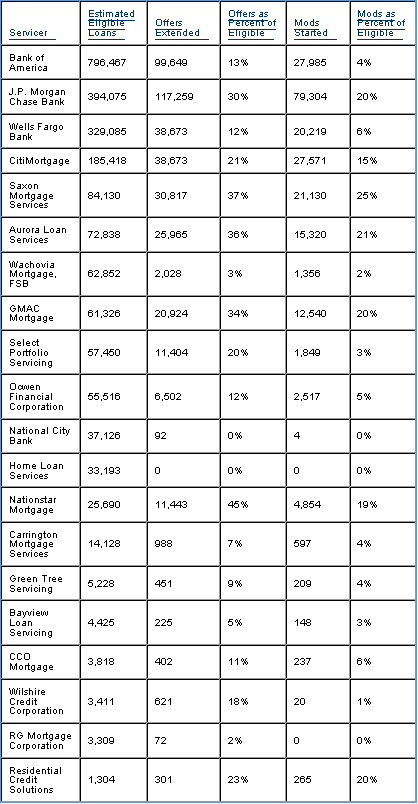

The following sortable chart lists the firms with the most eligible loans that are delinquent for 60 days or more.

Keep in mind that these are not foreclosures. These are loans in trouble or owned by individuals that are at risk. Just take a look at the top four lenders. They have about 1.7 million loans that are 60 or more days past due, they have managed to work through about 300,000 of them and have extended modifications for about 150,000. We know that the failure rate for modifications is about 50%, so put that in the mix and it looks as if we’re just chasing our tail here.

The point isn’t that we aren’t making some progress, we are. There are a finite number of homes that will end up in the lenders hands and we are probably approaching that level but the meme that we have touched the bottom and are now in a recovery period might be overdone.

Sooner or later supply and demand are going to come into line. I’m not sure that we’re there yet.

- Bulenox: Get 45% to 91% OFF ... Use Discount Code: UNO

- Risk Our Money Not Yours | Get 50% to 90% OFF ... Use Discount Code: MMBVBKSM

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply