Harold Meyerson, Washington Post opinion writer, channels a Bloomberg report (via The Big Picture), and thinks he finds a smoking gun:

“Why is this recovery different from all other recoveries?

“… what really sets the current recovery apart from all its predecessors is this: Almost three years after economic growth resumed, the real value of Americans’ paychecks is stubbornly still shrinking. According to Friday’s Bloomberg Economics Brief, ‘the pace of income gains is well below that of the past two jobless recoveries and real average hourly earnings continue to decline.’

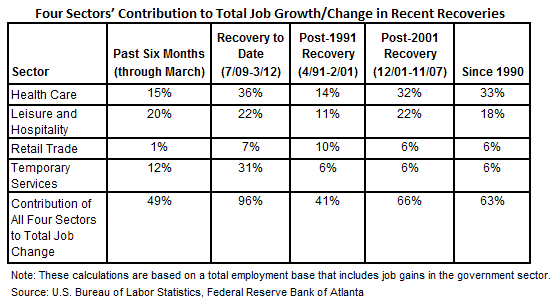

“The Bloomberg report cites one reason for this anomaly: Most of the jobs being created are in low-wage sectors. According to Bloomberg, fully 70 percent of all job gains in the past six months were concentrated in restaurants and hotels, health care and home health care, retail trade, and temporary employment agencies. These four sectors employ just 29 percent of the country’s workforce but account for the vast majority of the jobs being created.”

Meyerson accurately repeats the Bloomberg story, but that story itself is somewhat misleading. To begin with, the 70 percent figure appears to include the entire category of professional and business services, of which temporary help services are only a part. The types of jobs that fall under the professional and business service label are broadly described by the U.S. Bureau of Labor Statistics and include employment in scientific and technical services, management jobs as well as administrative and support type jobs. In particular, the professional scientific and technical services sector is described as follows…

“The Professional, Scientific, and Technical Services sector comprises establishments that specialize in performing professional, scientific, and technical activities for others. These activities require a high degree of expertise and training. The establishments in this sector specialize according to expertise and provide these services to clients in a variety of industries and, in some cases, to households. Activities performed include: legal advice and representation; accounting, bookkeeping, and payroll services; architectural, engineering, and specialized design services; computer services; consulting services; research services; advertising services; photographic services; translation and interpretation services; veterinary services; and other professional, scientific, and technical services.”

… and here is the description of management of companies and enterprises sector:

“The Management of Companies and Enterprises sector comprises (1) establishments that hold the securities of (or other equity interests in) companies and enterprises for the purpose of owning a controlling interest or influencing management decisions or (2) establishments (except government establishments) that administer, oversee, and manage establishments of the company or enterprise and that normally undertake the strategic or organizational planning and decision making role of the company or enterprise. Establishments that administer, oversee, and manage may hold the securities of the company or enterprise.”

These parts of the economy are hardly made up of the prototypical low-wage jobs and, according to my calculations, you don’t get to Bloomberg’s 70 percent number without including them.

If you focus strictly on “restaurants and hotels” (or, more precisely, the leisure and hospitality sector), health care, retail, and temporary employment services, your conclusion would be that these sectors accounted for about 50 percent of total job growth/change over the past six months, a share that may still strike you as pretty significant. But is it really? A little historical context might help:

It is true that this expansion, which began in July 2009, has been unusually concentrated in the four sectors identified by Bloomberg and highlighted in the Meyerson piece. However, a closer look reveals that the only one of the four that looks unusual is employment in temporary help services, the share of which in this recovery has been five times the post-1990 level as a whole. (We reach the same conclusion even if we compare where we are today in this recovery—roughly three years out—with that same period following the recoveries from the 1991 and 2001 recessions.)

On the other hand, it is also true that the share of temp services in total jobs gains has been much lower over the past six months than it was earlier in this recovery. I don’t know if that share will eventually fall to the (remarkably stable) level that characterized the (almost) two decades before the past recession. But even if that share remains near 12 percent, as opposed the more historical 6 percent level, I think the story remains the broad-based nature of the relatively tepid growth (in incomes and jobs) that has characterized this recovery.

- Bulenox: Get 45% to 91% OFF ... Use Discount Code: UNO

- Risk Our Money Not Yours | Get 50% to 90% OFF ... Use Discount Code: MMBVBKSM

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply