Morgan Stanley, the uber bull in Apple (NASDAQ:AAPL) is out with some very positive comments on the name after completing their US consumer survey.

– The firm issues a positive Research Tactical Idea (RTI) on AAPL.

Their 3 key takeaways are:

* iPhone demand is tracking ahead of expectations in C4Q11. The survey points to 11-12 million US iPhone shipments in the December quarter, which translates to 31-36 million global shipments. This compares to Morgan Stanley estimate of 30 million and consensus estimate of 28 million.

* Surprisingly, US consumers expect to buy more iPhones in C1Q12 than in C4Q11. Even after applying a 10% discount to C1Q12 purchase intentions, the survey predicts 13 million US iPhone sales or 41 million global iPhone sales in the March quarter. For perspective, the firm currently models 28 million iPhone shipments in C1Q12, down 7% Q/Q. Given iPhone demand will benefit from more country and carrier rollouts next quarter, likely including China, the data bodes well for meaningful iPhone unit upside in early 2012. Applying the average iPhone seasonality over the past two years to C1Q12 shipments based on firm’s survey implies 190 million iPhones in CY2012, roughly in-line with the 200 million production capacity Apple is asking suppliers to prepare.

* Perhaps most surprising, US tablet demand remains extremely strong despite recent data points regarding iPad production cuts and Corning’s negative pre-announcement pertaining to Gorilla glass. Only 8% of US consumers own a tablet today but 27% plan to buy one, according to the survey. This represents 63 million future purchases vs. 26.5 million tablets shipped over the past six quarters in the US. While Apple will give up a modest 4 points of share to Amazon’s Kindle Fire, the overall market growth puts upward pressure on their estimates. 13% of US consumers, or about 30 million people, plan to buy the iPad, which compares to about 16.8 million sold in the US to date and our global iPad forecast of 52 million in CY12 (roughly 20 million of which are US). Applying the recent US iPad mix of 37% to the US demand figure implies 81 million global iPad units next year, in-line with the 80 million production capacity Apple is asking suppliers to prepare.

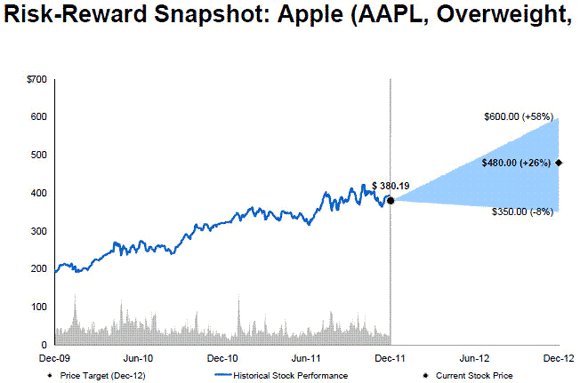

Firm maintains Overweight rating and $480 PT on AAPL. Firm’s Bull case stands at $600.

Notablecalls: This should clear some of that uncertainty created by Corning’s (GLW) warning.

Would not be surprised to see AAPL move up on this in the n-t.

- Bulenox: Get 45% to 91% OFF ... Use Discount Code: UNO

- Risk Our Money Not Yours | Get 50% to 90% OFF ... Use Discount Code: MMBVBKSM

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply