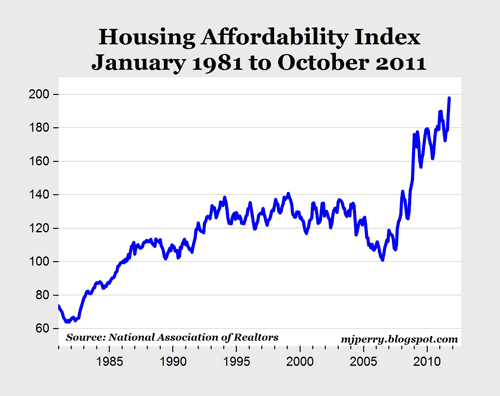

The chart above shows the National Association of Realtors’ monthly housing affordability index back to January of 1981 (data here). The historical trend over the last 30 years is pretty striking for several reasons:

1. In the 1981-1982 period when the 30-year mortgage rate was peaking at record highs of 16-18%, the housing affordability index was about 65, meaning that the typical American family was only earning 65% of the income necessary to qualify for a 30-year mortgage to purchase a median-price home (with 20% down payment).

2. As interest rates fell through the 1980s, housing became more affordable and the index rose above 100 by the mid-1980s, and has remained above 100 since then.

3. From the early 1990s through about 2005, the affordability index was pretty stable in the 120-140 range, until the housing bubble came along and inflated home prices, which lowered the affordability index down to 101 by July 2006.

4. Over the last five years or so, the housing affordability index has nearly doubled to 197.8 in October of this year, reaching the highest level in the history of the index, and maybe the highest level ever? Amazingly, the typical American family in October had almost twice the amount of income necessary to purchase the median-priced home.

What, if any, are the implications of housing affordability being at the highest level in history? It’s true that not everybody will benefit from this historic affordability, but many Americans will, especially first-time home buyers. Here are some thoughts:

1. We keep hearing about stagnating income, rapacious income inequality, the disappearance or difficulties of the struggling middle-class, and how younger generations today will be worse off economically than their parents, how a household today needs to have both parents working full-time to survive financially, etc.

2. For CPI calculations, the BLS weights shelter as about one-third of consumer expenditures (32%), which is the category with the highest weight, and much higher than food (15%), clothing (3.6%), transportation (17%), medical care (6.6%), recreation (6.3%), and education (6.4%), etc.

3. Given the facts that: a) housing/shelter is the greatest single expense for American households by far, and b) housing affordability is at an all-time historical high, doesn’t that have to transfer into a huge increase in the standard of living for many Americans, especially younger, first-time, middle-class home buyers?

For example, doesn’t the fact that the typical household now has almost twice the income necessary to qualify to buy a median-priced home contradict the common narrative that it takes two adults working full-time today to support a household, whereas in the past it only took one full-time earner? Making the two-earner case would have been much easier 30 years ago when housing affordability was below 100.

Further, when a household’s main monthly expense is now the most affordable in history, doesn’t that translate into a huge increase in household purchasing power, even if wages are stagnant? Of course, one could argue that current homeowners don’t necessarily benefit from record-high affordability, but there are still millions of young Americans who have been benefiting and will continue to benefit if affordability remains high.

Bottom Line: Doesn’t historically high housing affordability at least partially offset some of the narrative of stagnating income, the shrinking middle-class, and how younger generations today will be worse off economically than their parents, and how struggling household today needs to have both parents working full-time to survive financially, etc.?

There may not have been any generation in history that has faced such incredibly affordable home ownership, especially when a young couple is buying a first home to get started in life, invest in a home, and raise a family. At least in terms of housing affordability, young, middle-class Americans have never had it this good.

- Bulenox: Get 45% to 91% OFF ... Use Discount Code: UNO

- Risk Our Money Not Yours | Get 50% to 90% OFF ... Use Discount Code: MMBVBKSM

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply