As is widely known, the Federal Reserve is working on improving its communication strategy to provide better guidance about monetary policy and thus hopefully induce better outcomes. From today’s Wall Street Journal:

The Fed has taken ad hoc steps in this direction. During the financial crisis, it said rates would stay low for an “extended period.” In August, it said they would stay low “at least through mid-2013.” Quarterly projections would formalize this guidance and make it more specific. If the Fed signals that rates will stay lower even longer than investors expect, it could push long-term interest rates down now, spurring investment, spending and growth.

“The scope remains to provide additional accommodation through enhanced guidance on the path of the federal funds rate,” Fed vice chairwoman Janet Yellen said in a speech last week. She is chairing the Fed subcommittee designing the communications overhaul.

The “mid-2013” formulation is especially problematic. At some point it will need to be updated. With unemployment high and not falling quickly, it is possible the Fed won’t raise interest rates until much later. Of course, if inflation surprisingly picks up, it might need to move rates up sooner.

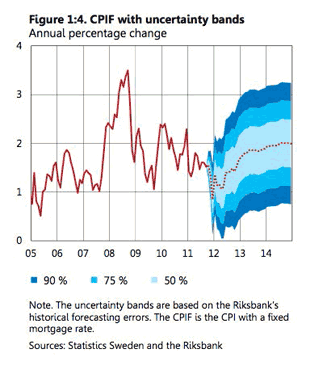

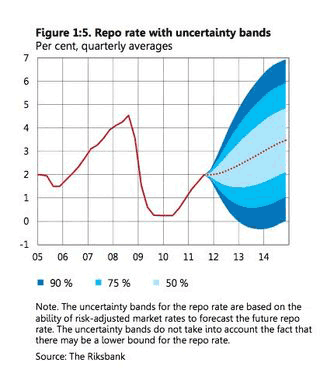

What form might “enhanced” guidance take? It seems unlikely that the Fed would limit itself to point estimates on the future course of interest rates. Reality is much more probabilistic, and I would expect additional Fed guidance to reflect forecast uncertainty via confidence intervals. One such example would be the Monetary Report of the Swedens’ central bank. Forecasts for inflation:

yield interest rate guidance:

Essentially, this formalizes what we already expect – if inflation exceeds forecasts, then it is likely interest rates will rise at a greater rate than currently expected. It also provides information on the magnitude of any deviation from the interest rate forecast given differing inflation forecasts. Of course, we would expect the Fed to include a similar forecast for unemployment. And, given the current range of policy tools, it would be nice to have guidance on the balance sheet as well, although I sense it to be unlikely.

Expect some push back from some Federal Reserve policymakers:

Some Fed officials still aren’t convinced this is the right approach. Giving interest rate guidance “might be an interesting exercise,” Richard Fisher, president of the Dallas Fed, said in an interview last week. “Its utility I wonder about.”

Some officials, like Mr. Fisher, doubt it will accomplish much. One risk is the Fed’s signals about the expected path of rates might even confuse the public, rather than clarify the central bank’s intentions.

I tend to think this is misguided – that a probabilistic assessment of the Feds’ forecast will make it easier to interpret the implications of incoming data for the evolution of Fed policy, thus making the public less reliant on the often discordant views of Fed officials. Importantly, in the current environment I think additional guidance would make clear that the more hawkish policymakers are outliers, thus minimizing the likelihood of raising premature expectations of policy tightening as we experienced earlier this year. Which would explain Fisher’s resistance to chance – he would prefer not to be further marginalized in the policymaking process.

Note: Sorry to be short on posts recently. I have been running around the last few days trying to tied up loose ends at the end of the term.

- Bulenox: Get 45% to 91% OFF ... Use Discount Code: UNO

- Risk Our Money Not Yours | Get 50% to 90% OFF ... Use Discount Code: MMBVBKSM

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply